2Q Reserve Fund Operation Amount 260 Trillion Won... Up 16.8% YoY

Domestic Yield Around 2%... Significantly Lower Than Overseas

Need for Benchmarking Advanced Countries Including Introduction of Fund-Type Governance

[Asia Economy Reporters Kwangho Lee and Hayoung Ki] As the importance of retirement assets grows due to aging populations, the retirement pension market is rapidly expanding. However, despite quantitative growth, returns have remained sluggish, prompting calls for regulatory improvements by financial authorities and the establishment of advanced country-style business models.

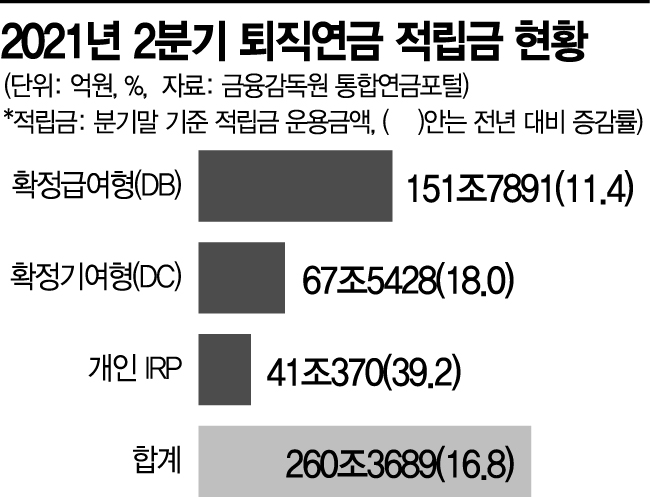

According to the Financial Supervisory Service's Integrated Pension Portal on the 26th, as of the second quarter of this year, the total retirement pension fund managed by 43 financial companies reached 260.3689 trillion KRW, a 16.8% (37.3458 trillion KRW) increase compared to 223.0231 trillion KRW in the second quarter of last year.

In particular, the growth of Individual Retirement Pensions (IRP) was steep. The IRP fund in the second quarter was 41.037 trillion KRW, up 39.2% (11.5531 trillion KRW) from the previous year. Defined Benefit (DB) and Defined Contribution (DC) plans also increased by 11.4% and 18.0%, recording 151.7891 trillion KRW and 67.5428 trillion KRW, respectively.

By sector, the financial investment industry showed remarkable growth. This is attributed to increased funds flowing into financial investments due to the stock market boom continuing since last year. Although the total retirement pension fund size was smaller than that of insurance and banks, it achieved 55.6021 trillion KRW, a 23.3% (10.4975 trillion KRW) increase compared to the previous year.

Banks recorded the largest scale at 135.0749 trillion KRW, increasing by 16.6% (19.2017 trillion KRW) during the same period. Insurance showed a 12.3% increase to 69.6919 trillion KRW. In both banks and financial investments, individual IRP funds increased significantly by 36.1% and 62.9%, respectively, driving net fund growth.

Over the past year, the financial investment sector also posted the highest operating returns. Financial investments recorded DB-type returns of 1.72% to 6.70%, DC-type 4.85% to 17.62%, and individual IRP 3.68% to 21.00%. Banks achieved DB-type returns of 0.43% to 1.69%, DC-type 1.49% to 3.92%, and individual IRP 1.44% to 6.24%. Insurance recorded DB-type 1.57% to 2.89%, DC-type 2.12% to 6.51%, and individual IRP 1.92% to 10.48%.

Securities Firms Can Invest Aggressively... Banks Focus on Deposits and Savings

This difference arises because financial investments pursue aggressive investment strategies, whereas banks mainly manage funds through principal-guaranteed deposits and savings. Banks requested financial authorities to allow real-time trading of Exchange-Traded Funds (ETFs) for DC-type and individual IRP accounts, but the authorities denied this, stating that ETF trading brokerage is beyond the scope of banks' permissible activities.

There are voices predicting an acceleration in the movement of retirement pension funds for these reasons. According to four major securities firms?Mirae Asset, NH Investment & Securities, Korea Investment & Securities, and Samsung Securities?the amount of IRP funds moved from banks and insurance to financial investments reached 312.2 billion KRW in the first quarter alone. Compared to 156.3 billion KRW in 2019, this more than doubled in one year. Additionally, the amount invested in ETFs from DC and IRP accounts at these four securities firms surged to 1.3204 trillion KRW in the first quarter, more than seven times the 183.6 billion KRW recorded in 2019.

Experts: "Regulatory Improvements Needed to Enhance Retirement Pension Returns"

Experts say that rather than competition among sectors, regulatory improvements and benchmarking advanced countries are necessary to improve returns. In advanced countries like the United States and Australia, retirement pension returns reach 7?10%. In contrast, domestic returns hover around 2%. The seven-year (2013?2019) average annual return on retirement pensions was 9.5% in the U.S. and 8.9% in Australia, while Korea remained at 2.3%. At the end of last year, 89% of Korea's retirement pension products guaranteed principal and interest, whereas in advanced countries like the U.S. and Australia, this ratio was between 30% and 60%.

Jae-woo Nam, a research fellow at the Korea Capital Market Institute, said, "To increase retirement pension returns, it is necessary to introduce a fund-type governance structure and improve existing methods." Australia's 'Superannuation,' introduced in 1992, allows workers to invest in funds of their choice and manage them until retirement. Notably, subscribers can select from retail funds, industry funds, corporate funds, public funds, and small funds.

Taeyoon Sung, a professor in the Department of Economics at Yonsei University, advised, "While there may be room to strengthen choices regarding retirement pensions, investing in risky assets to increase returns is not appropriate. Applying pressure could rather cause problems."

Sangbong Kim, a professor in the Department of Economics at Hansung University, said, "Despite last year's stock market boom, retirement pension returns remain low. Financial institutions should pay more attention to managing DB-type returns, and institutionally, it is necessary to allow free movement between retirement pension types so individuals can return to DB-type even after switching to DC-type."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}