FSS's Remarks on Strengthening Supervision Prove Hollow

Five Major Banks Close 191 Branches in One Year

Over 100 Consolidation Plans Scheduled for Second Half of This Year

[Asia Economy Reporter Jin-ho Kim] Since the COVID-19 pandemic, non-face-to-face transactions have become more commonplace, accelerating the closure of branches by commercial banks. The financial authorities' recommendation that rapid branch closures are undesirable has become almost meaningless. Major banks have announced plans to consolidate and close at least 100 branches in the second half of this year.

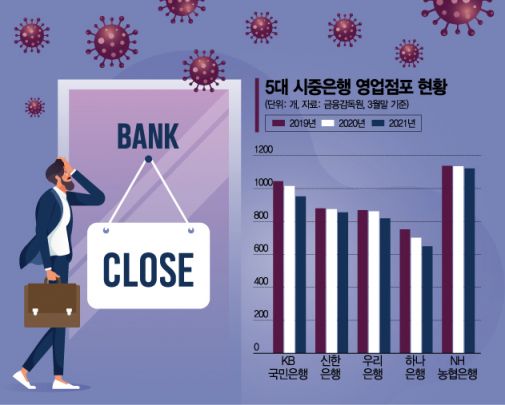

According to the Financial Supervisory Service's Financial Statistics Information System on the 29th, as of the end of March this year, the number of branches of the five major banks (NH Nonghyup, KB Kookmin, Shinhan, Woori, and Hana Bank) stood at 4,398, down by 191 from a year earlier. This decrease is about twice the reduction of 96 branches recorded from March 2019 to March 2020.

Former FSS Governor Yoon Seok-heon stated at an executive meeting last July that "reducing the number of branches in a short period is undesirable" and announced plans to strengthen management and supervision. However, major commercial banks appear to have disregarded this and accelerated branch closures.

In particular, after former Governor Yoon's remarks and the FSS's announcement to prepare guidelines related to branch closures, major banks hurried to close branches. In the second half of last year alone, 139 branches disappeared, which is seven times more than the 21 branches closed during the same period in 2019.

Despite the financial authorities' "verbal warnings," banks pushed ahead with branch closures mainly due to the normalization of non-face-to-face transactions triggered by COVID-19. The intensifying competition in mobile banking and the preference for non-face-to-face transactions due to COVID-19 have made digital innovation and the activation of non-face-to-face transactions essential rather than optional for major commercial banks.

In fact, for some commercial banks, the proportion of non-face-to-face transactions for credit loans and installment savings products approached 70-80% in the first half of this year. An environment has emerged where customers can perform all deposit and loan transactions without visiting a bank branch.

For example, one bank reported that the non-face-to-face proportion of installment savings reached 89.2% in the first half of this year. Nine out of ten newly opened savings accounts were subscribed to non-face-to-face. A banking industry official said, "All transactions at banks have become possible through mobile banking and other non-face-to-face channels," adding, "In this trend, maintaining branches that incur high maintenance costs is both a burden and inefficient."

Branch closures by major commercial banks are expected to accelerate further in the second half of this year. The five major banks have already confirmed plans to consolidate and close around 100 branches.

Shinhan Bank alone has confirmed the consolidation and closure of 62 branches in the second half of the year. Since there is still time until the end of the year, additional branch closures are likely. If so, Shinhan Bank's total number of branches will fall below 800. Woori Bank also plans to consolidate 23 branches in the second half of the year. Hana Bank has announced plans to consolidate seven branches initially, with expectations of more closures in the future. KB Kookmin Bank and Nonghyup Bank are reported to be in similar situations.

Meanwhile, concerns have been raised that the acceleration of branch closures may marginalize elderly people and others in terms of financial services. The financial authorities have also suggested policy directions to activate unmanned branches and counter partnerships, especially in areas with many financially marginalized groups.

However, the banking sector holds a negative view toward so-called joint branches, such as counter partnerships. There is significant resistance to the unclear responsibility in case of financial accidents and to the comparison of bank-specific products in the same space. A financial industry official said, "If problems arise in managing branches operated as joint branches, it may be difficult to resolve them smoothly," adding, "Unmanned branches utilizing smart ATMs are considered a realistic alternative."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}