[Asia Economy Reporter Ji Yeon-jin] It is forecasted that emerging market stocks will be at a disadvantage compared to developed countries once the U.S. Federal Reserve's (Fed) tapering (reduction of asset purchases or quantitative easing) begins.

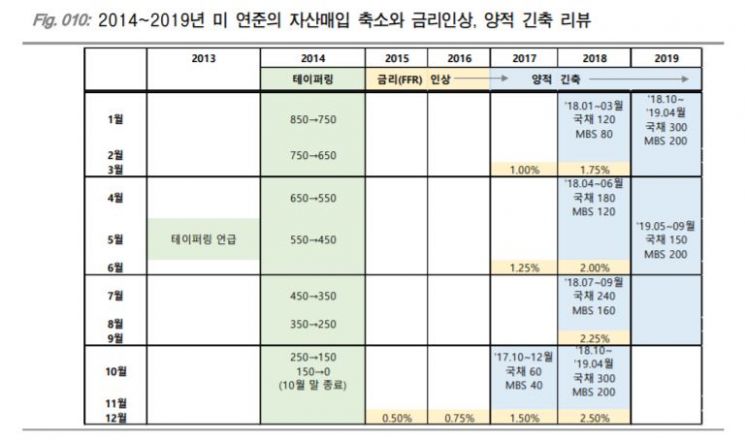

According to the financial investment industry on the 25th, the essential step for the Fed's tapering implementation is a prior notice to mitigate market shocks. If tapering starts early next year, a prior notice is highly likely around July to August. The 2014 tapering proceeded from January to October, with the first mention in May 2013. At that time, it took 13 months from the end of tapering to the first interest rate hike. The interval between the first and second rate hikes was also about one year.

It took 22 months from the first rate hike to the start of quantitative tightening (cessation of reinvestment in maturing government bonds or MBS).

At that time, the economic cycle had fully turned from mid-2011, and economic expansion continued until February 2020, so monetary tightening began in the late phase of a clear economic expansion. This accommodative monetary policy is evaluated to have contributed significantly to extending the economic expansion period. Such accommodative monetary policy was thanks to limited inflation. Currently, if inflation remains limited, the Fed's tightening could proceed slowly over a long period, similar to post-2014.

However, due to COVID-19, the Fed's total assets have doubled over the past year, increasing the need for balance sheet normalization (policy reversal) as the economy recovers. Also, with the U.S. labor market approaching near full employment by the end of 2022 and economic expansion accelerating, if the Fed delays its exit strategy by focusing solely on inflation conditions, it may face the burden of simultaneously implementing tapering, rate hikes, and quantitative tightening within a year.

Recently, factors that increase risks in asset markets due to rising capital costs have increased, and with growing debt levels, central banks worldwide must balance controlling these financial imbalances while continuing to support the economy.

Therefore, it is expected that the Fed will focus its policy on at least suppressing additional monetary easing. There is a high possibility that tapering and moderate balance sheet restraint policies will be implemented from early next year before the first rate hike.

Because of this, unlike the 2014 case where tapering alone did not directly affect money markets (short-term interest rates), long-term interest rates, and stock prices significantly, this time the impact could be substantial. If tapering, rate hikes, and quantitative tightening occur, liquidity will be absorbed into developed countries, which are the providers of liquidity, thus negatively affecting emerging market stocks.

Han-jin Kim, a researcher at KTB Investment & Securities, said, "Assuming a tapering and a series of long monetary tightening schedules in the late phase of economic expansion similar to post-2014, relatively favorable asset classes would be stocks," adding, "During the phase where additional monetary easing is suppressed and monetary policy shifts to tightening, technology stocks (Nasdaq), industrial value stocks (Dow Jones), gold, metals, commodities, and crude oil are likely to show relative performance superiority in that order."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}