Big Tech's Full-Scale Entry into Finance: Tilted Playing Field vs. Consumer Benefits Clash

Conflict Peaks Over Debt Refinancing Platforms

Expert Urgent Diagnosis: "Government Must Act as an Impartial Referee"

[Asia Economy Reporters Kiho Sung and Jinho Kim] As the digital finance era fully unfolds, traditional financial institutions and big tech companies (large information and communication enterprises) are clashing over various issues. This is because each side has sharply conflicting interests regarding the new systems introduced in response to these changes. While the financial sector claims that big tech companies receive excessive privileges, big tech argues that excessive regulation from the financial sector infringes on consumer convenience.

Despite mediation efforts by financial authorities, the confrontation between the two sides continues. Experts point out that the government should actively respond with the principle of ‘same business, same regulation’ while allowing market autonomy.

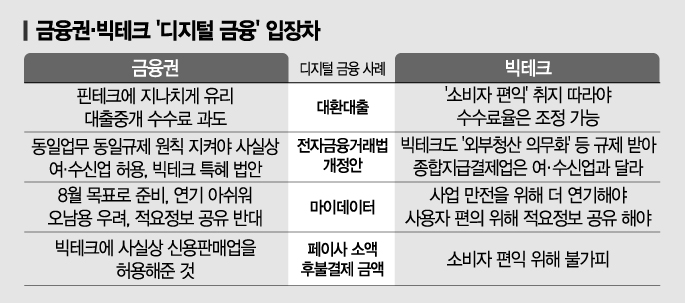

◆ Tilted playing field vs. consumer benefits ‘tension’ = According to the financial sector on the 19th, the conflict between existing financial companies and big tech is deepening ahead of the scheduled launch of the non-face-to-face refinancing loan (loan switching) platform in October. The refinancing loan service promoted by the government allows consumers to compare interest rates of all financial institutions’ loan products via smartphone applications or websites and easily switch to loans with lower interest rates. Both financial companies and big tech agree with this purpose.

However, financial companies strongly oppose it, arguing that it will only increase big tech’s dominance. They claim that consumers will inevitably have to use services from big tech or fintech companies that have built powerful platforms. On the other hand, big tech cites consumer benefits and raises concerns about high intermediary fees.

The two sides have also sharply clashed over the implementation of MyData, which has been promoted since last year. They have debated the scope of data usage from the preparation stage and recently have been in conflict over the timing of the project’s implementation. The Financial Services Commission recently held an expert advisory meeting and decided to include bank transaction details within the scope of MyData. Transaction details refer to information recorded about bank account deposits and withdrawals, including the accounts, names, and memos of senders and recipients. Banks have opposed disclosing this information, citing concerns over misuse of personal data. Furthermore, when financial authorities indicated that the mandatory application programming interface (API) implementation for MyData might be delayed from August, accommodating big tech’s requests, opposition from the financial sector intensified.

The conflict surrounding the amendment of the Electronic Financial Transactions Act is also ongoing. The financial sector argues that big tech companies effectively conduct deposit and loan businesses but are not subject to the same regulations as banks. Big tech counters that since they cannot freely operate consumer deposits, cooperative payment businesses are clearly different from deposit and loan businesses.

The tug-of-war with big tech is not limited to banks. Previously, the card industry clashed with financial authorities over the standard for ‘PaySa small postpaid payment amounts.’ Initially, the limit was expected to be around 500,000 KRW, but reflecting the card industry’s position, it was reduced to 300,000 KRW. However, this effectively allowed credit sales, and the card industry views the encroachment of big tech companies into the credit sales market as a matter of time.

◆ Experts: "Government should be a third party, not a player" = Experts explain that it is a natural progression for the two sides to clash as the digital finance era advances. However, they emphasize that the government’s active role is crucial before confusion worsens. In particular, experts agree on the necessity of applying the same regulations to the same industries.

Professor Minhwan Lee of Inha University’s Global Finance Department said, “With the emergence of big tech, the boundaries of the financial industry have become ambiguous, so instead of overall regulation of the financial sector, regulations should be introduced by business type.” He added, “Creating regulations by business type prevents conflicts among stakeholders.” He noted that although the pace of change in the financial industry is very fast recently, the framework for regulation and supervision needs to be transformed.

Rather than the government directly intervening in financial policy, it was also emphasized that the government should act as a ‘referee’ who applies regulations without discrimination while leaving market autonomy intact. Professor Jiyong Seo of Sangmyung University’s Business Administration Department said, “The government should be a third party that reviews regulations. It should not participate as a player as it does now.” He pointed out, “For the refinancing loan platform, it would be better to create platforms by industry to promote competition and resolve conflicts.”

There was unanimous agreement on the principle of same regulation for the same business. Professor Sangbong Kim of Hansung University’s Economics Department stated, “Globally, the financial industry has lines that must be strictly observed,” and added, “Same regulations are essential for the same business.” Senior Researcher Hyekyung Jo of the Political Economy Research Institute Da-an also said, “The principle of same function, same regulation must be established,” and noted, “The controversy continues because the principle is not being upheld.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}