Data Entry Errors and Inadequate Validation

Authorities Issue Successive Improvement Notices

[Asia Economy Reporter Oh Hyung-gil] Insurance companies with poor financial management, such as failing to comply with the Risk-Based Capital (RBC) ratio calculation regulations, are being repeatedly exposed. With the new International Financial Reporting Standards (IFRS17) and the new solvency regime (K-ICS) set to be implemented in six months, completely changing the accounting system, there are concerns that even the current system is not being properly followed on the ground.

According to the insurance industry on the 5th, financial authorities notified MG Insurance last month to strengthen the procedures for calculating and verifying RBC ratio credit and market risk amounts, issuing a management caution.

MG Insurance inaccurately applied related regulations while calculating credit market risk through the RBC standard model and failed to detect data entry errors by the person in charge, resulting in an underestimation of RBC credit and market risk amounts. Additionally, for real estate project financing (PF), the credit risk coefficient should have been applied higher than that of securities with the same credit rating, but this was not followed, lowering the risk amount.

Lotte Insurance was sanctioned last month after it was revealed that in 2019, the Risk Management Team did not implement the comprehensive risk management plan, citing uncertainty about the timing of K-ICS introduction, and failed to report this to the Risk Management Committee.

When establishing the comprehensive risk management plan, it was anticipated that the solvency ratio would deteriorate compared to the current RBC standard model if K-ICS were introduced, and an impact assessment was to be conducted along with measures such as expanding available capital and reducing required capital, but these were not followed.

Moreover, from 2017 to April this year, there were four occasions requiring early warning issuance for interest rate risk, but the Risk Management Team issued early warnings only twice. Although early warnings for insurance risk were issued eight times, the relevant departments did not carry out follow-up measures such as reviewing portfolio changes.

[Image source=Yonhap News]

[Image source=Yonhap News]

Current System Not Even Being Followed

"Insurance Companies, Capital Adequacy Management and Supervision"

In April, a fine of 40 million KRW was imposed for violating the obligation to reserve policyholder liabilities. It was later confirmed that when a new IT system was introduced in 2019, the method for calculating policyholder liabilities was incorrectly applied in the system and not verified, resulting in 5 billion KRW of policyholder liabilities not being accounted for.

AIG Insurance was also criticized in March for inadequate establishment of the Own Risk and Solvency Assessment (ORSA) system and was instructed to develop improvement measures to strengthen mid- to long-term interest rate risk management.

Hyundai Marine & Fire Insurance received a notification from financial authorities to improve the verification work of the Liability Adequacy Test (LAT) following a comprehensive audit conducted last year.

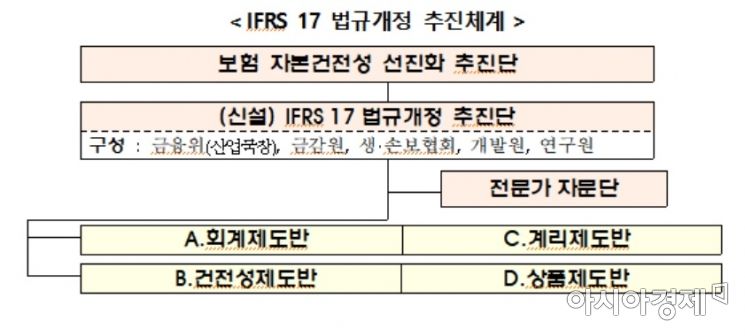

A financial authority official said, "With the implementation of IFRS17, financial management of insurance companies, especially capital adequacy management, will become more important," adding, "We plan to manage and supervise to ensure capital adequacy is maintained." Meanwhile, the Financial Services Commission has announced a draft amendment to the Enforcement Decree and Enforcement Rules of the Insurance Business Act reflecting IFRS17-related content for public comment.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}