New Handling Amount COFIX at 0.82%

Outstanding Balance COFIX Falls to 1.02%

[Asia Economy Reporter Kiho Sung] The COFIX (Cost of Funds Index), which serves as the benchmark for variable interest rates on mortgage loans in the banking sector, remained at the same level as the previous month. Accordingly, the variable interest rates on mortgage loans at commercial banks will also maintain their current levels for the time being. However, the balance-based COFIX, which reflects market interest rate changes more slowly, showed a decline.

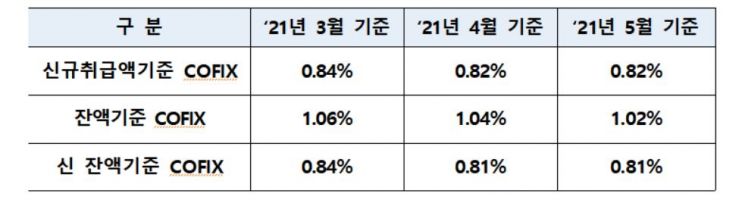

According to the Bankers Association on the 15th, the COFIX based on new transaction amounts for May was 0.82%, the same as in April. Although the COFIX based on new transaction amounts has fluctuated this year, it is generally on a downward trend.

On the other hand, the balance-based COFIX for May was 1.02%, down 0.02 percentage points from April's 1.04%. The "new balance-based COFIX" was 0.81%, also maintaining the same level as in April.

The balance-based COFIX has been continuously falling since recording 2.02% annually in March 2019. The new balance-based COFIX has remained below 1% for seven consecutive months.

With the COFIX based on new transaction amounts holding steady compared to the previous month, the variable interest rates on mortgage loans at KB Kookmin Bank, Woori Bank, and NH Nonghyup Bank will also maintain their current levels.

The mortgage loan interest rates based on new transaction amounts are 2.37% to 3.87% at Kookmin Bank, 2.58% to 3.58% at Woori Bank, and 2.35% to 3.56% at Nonghyup Bank. Based on the new balance, Kookmin Bank's rates range from 2.48% to 3.98%, Woori Bank's from 2.57% to 3.57%, and Nonghyup Bank's from 2.34% to 3.55%.

COFIX is the weighted average interest rate of funds raised by eight domestic banks, reflecting changes in interest rates of deposit products such as actual deposits, savings, and bank bonds handled by banks. When COFIX falls, it means banks can secure funds by paying less interest, and when COFIX rises, the opposite is true.

The COFIX based on new transaction amounts and balances reflects interest rates on deposit products including time deposits, installment savings, mutual installment savings, housing installment savings, negotiable certificates of deposit, repurchase agreements, commercial paper sales, and financial bonds (excluding subordinated bonds and convertible bonds).

An official from the Bankers Association stated, "Those seeking COFIX-linked loans should fully understand the characteristics of COFIX and carefully select loan products."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}