US May Consumer Prices Hit 13-Year High

Volatility Expected Amid FOMC Tapering Talks

Market Sees 'Inflation Peak'...Focus on Growth Stocks

"Value Stocks to Maintain Market Lead" Forecast

[Asia Economy Reporters Ji Yeon-jin and Lee Seon-ae] Ahead of the two-day U.S. Federal Open Market Committee (FOMC) meeting starting on the 15th of this month (local time), caution is growing in the domestic stock market. This is because last month’s U.S. consumer price inflation surged to its highest level in 13 years, raising expectations that the meeting might discuss tapering (the reduction of quantitative easing). Experts anticipate a bullish market after the FOMC, which will confirm the Federal Reserve’s (Fed) stance on high inflation and tapering, but opinions diverge regarding the rebound of growth stocks, which have been sluggish since the beginning of the year.

According to the financial investment industry on the 14th, tapering discussions are expected at the FOMC meeting on the 15th. This is because the April FOMC minutes confirmed mentions of asset purchase reductions, and the meeting comes right after the May consumer price index release, making tapering discussions inevitable. The U.S. May consumer price index rose 5.0% year-on-year, a significant increase from April’s 4.2%, and well above the forecast of 4.7%.

The market expects that the FOMC will likely avoid specific mentions of tapering this time and instead adjust the pace to minimize its impact on the stock market. The high inflation rate in the first half of this year is partly due to the base effect from last year’s low inflation during the first half caused by COVID-19, and the current U.S. unemployment rate (5.8%) has not yet fallen to pre-COVID-19 levels (3.5%).

Moon Nam-jung, a researcher at Daishin Securities, said, "This week’s stock market will experience increased volatility and heightened caution," adding, "However, it is highly likely that after the June FOMC, which will show the Fed’s stance to minimize negative impacts on the real economy and stock market, concerns about high inflation and tapering will subside." Daishin Securities recommends actively increasing exposure to growth stocks, particularly in IT, healthcare, and renewable energy sectors. Since U.S. inflation peaked last month, inflation concerns that dominated the global stock market in the first half of this year are expected to ease, and growth stocks, which had been under pressure from rising interest rates, are likely to rebound.

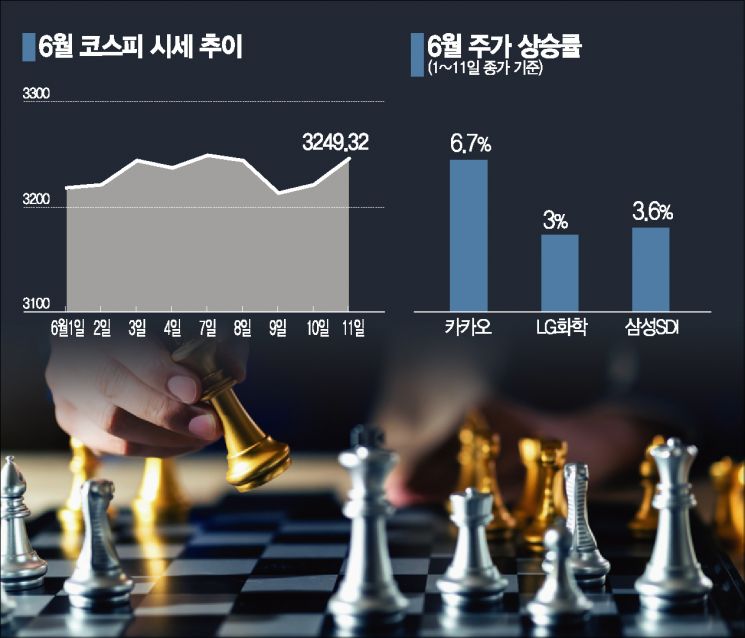

In fact, foreign investors and institutions have recently been actively buying growth stocks. From the beginning of this month until the 11th, foreign investors and institutions purchased 191.9 billion KRW and 179.2 billion KRW worth of Kia shares, respectively. Hyundai Motor also saw net purchases of 104.4 billion KRW and 59.7 billion KRW, respectively. They also bought secondary battery stocks. The third most purchased stock by foreign investors and institutions was Samsung SDI, with net purchases of 19.1 billion KRW and 73.4 billion KRW, respectively. SKC, which operates a secondary battery copper foil business, was fourth, with purchases of 43.1 billion KRW and 23.6 billion KRW, respectively. EcoPro BM, which produces cathode materials for electric vehicle batteries, was also bought with net purchases of 31 billion KRW and 20.1 billion KRW, respectively. They also focused on large bio stocks. Foreign investors and institutions bought Celltrion Healthcare worth 31.3 billion KRW and 31.4 billion KRW, respectively, and Samsung Biologics with net purchases of 28.2 billion KRW and 16.3 billion KRW, respectively. Additionally, funds flowed into HYBE (foreign investors 38.8 billion KRW, institutions 23.8 billion KRW) and Kakao Games (foreign investors 27.5 billion KRW, institutions 17 billion KRW).

However, there is also analysis that this growth stock rally should be viewed from a cyclical perspective. It is premature to hastily conclude the end of value stock rotation, as the deflationary phase has not yet arrived. Seo Jeong-hoon, a researcher at Samsung Securities, said, "Considering that there is still significant room for economic recovery and that policy support will continue for a considerable period, the dominance of value stocks is likely to persist." He added, "The timing for growth stocks to take the lead again is likely when the economic recovery momentum subsides and inflation rates return to average levels, which is reasonably expected to be around the end of this year or early next year at the earliest."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}