Secured Cash Through Two Capital Increases... Avoiding Complete Capital Impairment by Year-End

Mid- to Long-Distance Flight Strategy Is Positive

Major Shareholder Lacks Funding Capacity... Risk of Financial Difficulties May Resurface

[Asia Economy Reporter Jang Hyowon] Like other airlines, T'way Air has been going through difficult times since the COVID-19 pandemic. To prevent capital erosion caused by massive losses, it has conducted two rounds of fundraising.

For now, the urgent crisis seems to have been averted, but if the airline industry does not recover as expected, there is an analysis that T'way Air could face liquidity issues again. In particular, there are opinions that T'way Air may be hampered because its major shareholder's funding capability is weaker compared to competitors.

Breathing Room Secured with 80 Billion Won Capital Increase

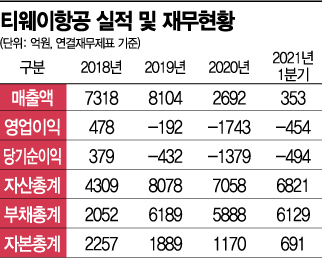

As of the end of Q1, T'way Air's consolidated sales stood at 35.3 billion won, down 76.3% from 149.2 billion won in the same period last year. Operating loss and net loss were 45.4 billion won and 49.4 billion won respectively, with losses increasing by 103.6% and 41.9%.

Founded in 2003, T'way Air is an LCC that has grown based at Daegu Airport, operating 27 aircraft with 9 domestic and 66 international routes. As of the end of last year, its domestic market share was 15.6%, and international market share was about 4.7%.

The main business segments are broadly divided into passenger and cargo, with most of T'way Air's revenue coming from passengers. As of the end of Q1 this year, the passenger segment accounted for 94.5% of sales. Originally, until last year, it was around 97-98%, but due to the sharp decline in passenger revenue caused by COVID-19 and a slight increase in cargo revenue, the proportion changed.

Although cargo revenue increased, it did not significantly impact performance. Unlike full-service carriers (FSCs) that deployed cargo planes on high-yield North American and European routes to boost sales, LCCs focused on Southeast Asian routes could not operate long-haul routes due to the lack of large aircraft.

T'way Air's slump began in earnest with the COVID-19 crisis last year. The airline recorded a net loss of 137.9 billion won last year alone. Consequently, its financial condition deteriorated rapidly. The debt ratio, which was 327.7% at the end of 2019, soared to 789.1% by Q3 last year.

Fortunately, in November last year, T'way Air raised 66.8 billion won through a rights offering, bringing the debt ratio down to 500% by the end of the year. Additionally, in April, it conducted a third-party allotment capital increase targeting Double U Value Up LLC, established by the private equity fund JKL Partners, raising 80 billion won in the form of convertible preferred shares.

By securing cash, the airline is expected to have breathing room until the end of this year. As of the end of Q1, T'way Air's total equity was 69.1 billion won. Adding 80 billion won brings it to 149.1 billion won. Even if it records losses around last year's level of 137.9 billion won this year, it can avoid complete capital erosion.

Jeong Yeonseung, a researcher at NH Investment & Securities, analyzed, "The 80 billion won capital increase secured liquidity to endure until the end of the year, significantly alleviating concerns about capital erosion due to losses this year. Also, the plan to sequentially introduce three medium-sized A330 aircraft by the end of this year to operate medium- and long-haul routes such as Sydney, Croatia, and Malaysia is positive in terms of actively expanding the route portfolio from a mid- to long-term perspective."

Weak Major Shareholder... Credit Rating Downgraded

However, the market views that if the COVID-19 situation continues beyond this year and the airline industry does not recover, T'way Air may face greater financial difficulties compared to other airlines. This is because its major shareholder has limited capacity to provide support compared to competitors.

T'way Air's major shareholder is T'way Holdings, a KOSPI-listed company. T'way Holdings recorded consolidated sales of 276.9 billion won last year, but its standalone sales excluding T'way Air's revenue were only about 7.7 billion won, which is minimal. T'way Holdings operates PHC file manufacturing as its own business. Moreover, it has recorded operating losses on a standalone basis for four consecutive years since 2017, indicating almost no cash-generating ability on its own.

Its cash holdings are also not ample. When T'way Air conducted a rights offering in November last year, it barely raised funds by issuing 30 billion won worth of bonds with warrants (BW) through a public offering.

At that time, Yerimdang, the largest shareholder of T'way Holdings and the apex of its governance structure, did not participate in the BW public offering despite the risk of dilution of its stake from 60.8% to 42.41% through stock conversion. Yerimdang is a company mainly engaged in publishing, and like T'way Holdings, its standalone sales excluding T'way Air, which is consolidated, were about 16.7 billion won, not large.

Given these circumstances, the credit rating of T'way Holdings' BW has already been downgraded twice since issuance. Korea Credit Rating (KCR) downgraded T'way Holdings' BW rating from B+ to B on the 28th of last month and placed it on a 'negative watchlist.' At the time of initial issuance in November last year, the rating was BB-, downgraded to B+ in February, and now further downgraded.

Park Soyoung, senior analyst at Korea Credit Rating, said, "Although the urgent liquidity concerns were alleviated by the 80 billion won capital increase, considering the scale of net operating cash outflows, if additional capital increases or fundraising are not made, liquidity risks could re-emerge in the short term. Given the variability in the timing of operating performance recovery and the A330 introduction plan, the trend of increasing financial burden is expected to continue."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}