Financial Authorities Plan to Maintain Last Year's Growth Rate of Savings Banks' Household Loans

Mid-Interest Loans Growth Rate Limited to 5.4%, Excluding Policy Financial Products

Concerns Over Low-Credit Borrowers Below Grade 7 Being Driven to 'Illegal Private Loans'

47% of New Savings Bank Overdraft Account Customers Are Youths Under 29

"Lending Without Credit Checks" Illegal Loan Ads Rampant on SNS

A loan counter at a bank in downtown Seoul. The photo is not related to any specific expression in the article. Photo by Yonhap News.

A loan counter at a bank in downtown Seoul. The photo is not related to any specific expression in the article. Photo by Yonhap News.

[Asia Economy Reporter Lim Juhyung] #Mr. Lee, a worker in his 20s, has been repeatedly worried recently about securing 'urgent funds.' As the year-end approaches, he finds it difficult to cover living expenses with just his credit card and is considering using savings banks. However, he heard that savings banks will soon tighten their loan screening. Mr. Lee appealed, "My credit rating is low, so using commercial banks is out of the question, and if savings bank loans are blocked too, there is no way to get money," adding, "I can almost understand the mindset of people who resort to illegal loans to roll over their debts."

Financial authorities have issued guidelines to control the growth rate of household loans by savings banks, raising concerns that low-credit households may face a 'financial cliff.' In particular, there is growing worry that young low-credit borrowers who have difficulty accessing institutional finance and rely on savings banks for loans may be driven to illegal private loans. Experts pointed out that if financial authorities directly restrict loans, the burden could fall on consumers.

According to the banking industry on the 2nd, the Financial Supervisory Service recently conveyed the '2021 Household Loan Management Plan for Savings Banks' to companies through the Korea Federation of Savings Banks. The core of this plan is to operate so that the total household loan growth rate this year does not exceed the previous year's growth rate (21.1%).

As a result, savings banks must limit the household loan growth rate, excluding 15.7% for mid-interest rate loans and policy financial products supporting low-income groups (such as Sunshine Loans and Saeitdol), to 5.4% this year.

The reason financial authorities issued such household loan management guidelines appears to be to curb the soaring household debt caused by the economic impact of COVID-19 and the investment frenzy known as 'Yeongkkeul' (pulling together all resources for investment) and 'Debt Investment.' According to the Bank of Korea, as of the first quarter (January to March), the household credit balance?which includes household loans from financial institutions, credit cards, and installment transactions?reached a record high of 1,765 trillion won.

Financial authorities have instructed savings banks to manage operations so that the growth rate of household loans does not rise sharply. The photo is unrelated to specific expressions in the article. Photo by Yonhap News.

Financial authorities have instructed savings banks to manage operations so that the growth rate of household loans does not rise sharply. The photo is unrelated to specific expressions in the article. Photo by Yonhap News.

The problem lies in the fact that if savings banks raise the bar for household loans, low-credit households will be hit hard. In particular, there are concerns that the young generation, who have little experience with unsecured loans and lack assets, making it difficult to use institutional finance, may face a steep 'financial cliff.'

As of the first half of last year, about 47.2% of new customers with overdraft accounts at savings banks were young people aged 29 or younger.

Young people who have just entered society often have insufficient financial transaction records, so there is little basis to assess their personal credit information, resulting in most receiving a 'mid-credit' rating of grades 5 to 6. Without proper management, they could fall to 'low credit' grades 7 or below, which restricts borrowing from primary financial institutions like commercial banks. Therefore, young people who need a lump sum of money have no choice but to rely on savings banks.

In this context, if savings banks tighten household loans, households lacking immediate living expenses may turn to illegal private loans. According to data from the Institute for Basic Economic Studies, about 80,000 to 120,000 financially vulnerable people moved to the illegal private loan market last year due to the economic downturn caused by COVID-19. The amount moved is estimated to be between 1.04 trillion and 2.1 trillion won.

Illegal private loans can cause great pain to low-credit borrowers because they impose higher interest rates than other financial institutions. According to a survey conducted by the Institute for Basic Economic Studies targeting households using private loans, about 70% of respondents said they paid interest rates higher than the legal maximum.

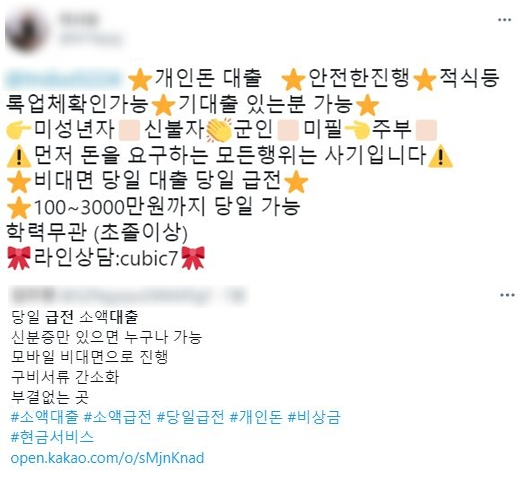

There are also concerns that young people lacking financial knowledge may fall victim to what is essentially 'financial fraud' disguised as loans. On social networking services (SNS) such as Twitter and Facebook, popular among the 20s and 30s generation, illegal loan advertisements have been posted repeatedly, claiming "We lend money without conditions" and "Verification is possible with just KakaoTalk messenger without credit checks." Some ads even claimed, "Same-day loans are possible for minors."

Illegal loan advertisements posted on social networking services (SNS) such as Twitter on the 3rd. / Photo by Internet homepage capture

Illegal loan advertisements posted on social networking services (SNS) such as Twitter on the 3rd. / Photo by Internet homepage capture

Amid this situation, young people in their 20s confessed that they have considered loans when they needed so-called 'urgent funds.'

A (28), who works at a restaurant in Gyeonggi Province, said, "After paying rent, phone bills, and insurance premiums with my salary, there is no money left. I am already worried about next month's living expenses," adding, "I have never had to take out a loan to prepare a lump sum for living expenses, but if I can't even use savings banks in desperate times, it would be bleak."

Company employee B in his 20s said, "I once checked my credit rating and was surprised to find it much lower than I expected," expressing concern, "I thought I might not be able to borrow money from commercial banks when I suddenly need a large sum, and now that loan conditions might become stricter, I am worried."

Experts pointed out that if financial authorities directly handle banks' loan operations, side effects may occur.

Professor Kim Taegi of Dankook University's Department of Economics explained, "If the Financial Supervisory Service imposes total volume regulations on banks' loan operations, the burden and costs tend to be passed on to consumers."

He added, "Regulations that control loans mean that the shortfall in capital must be sourced elsewhere (such as illegal private loans), which incurs additional costs," and suggested, "It is more desirable to allow banks, which directly handle loan operations on the front lines, to manage loans flexibly."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}