Top-tier Private Lending Companies' Total Assets and Net Income Decline

Major Firms Also Sequentially Halt Loans and Withdraw from Business

70% of Those Rejected for Loans Resort to Illegal Private Loans

Due to government regulations and successive reductions in the maximum interest rate, the management indicators of top-tier loan companies have significantly deteriorated. Leading large loan companies are either halting new loans or considering withdrawing from the market. Experts point out that if the regulated loan market collapses, the ultimate victims will be low-credit borrowers driven to illegal private loans.

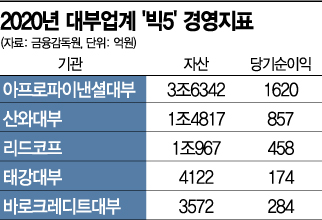

According to the Loan Finance Association and the Financial Supervisory Service on the 7th, the total assets of the top five loan companies last year (Apro Financial Loan, Sanwa Loan, Leadcorp, Taegang Loan, Baro Credit Loan) amounted to 6.9822 trillion won, a decrease of 204 billion won compared to the previous year. Net income also shrank by 32.84% (166 billion won) from 505.6 billion won to 339.5 billion won in one year. Even among the top 10 companies, net income decreased by 21.34% (117.3 billion won) from 549.8 billion won.

The problem is that these companies are leaning towards closing their businesses rather than overcoming management difficulties. They have either stopped issuing new loans and confirmed their withdrawal or rumors of business withdrawal are circulating. In 2019, when the Big 5 companies officially announced their withdrawal, some rankings changed, but the companies newly entering the Big 5 also face uncertainty in continuing their business.

At that time, Welcome Credit Line Loan, which was ranked, planned to withdraw from the loan market by 2024 on the condition of acquiring a savings bank. Last year, Joy Credit Loan stopped issuing new loans. Recently, the credit ratings of major domestic loan companies such as Leadcorp and Baro Credit Loan have also been continuously downgraded.

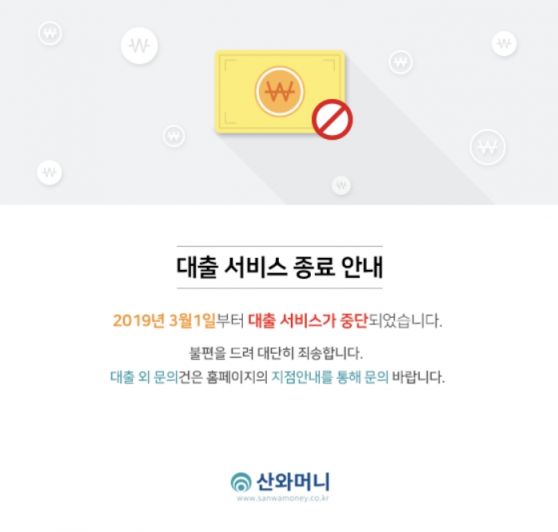

Sanwa Loan, a Japanese loan company that had been the undisputed industry leader for several years, has stopped issuing new loans since March 2019. Currently, it is focusing solely on recovering principal and interest on loans. The timing for resuming loans is also uncertain. The company states this is for soundness management, but there are speculations that the prolonged suspension of loans effectively means withdrawing from the Korean market.

As Sanwa Loan’s asset ranking shrinks, Apro Financial Loan, which took the top industry spot, is in a similar situation. This company launched OK Savings Bank by acquiring Yejoo and Yenarae Savings Banks in 2014. At that time, it promised the financial authorities to withdraw from the loan business by 2024 as a condition of the acquisition.

Leadcorp, ranked third, shows a steady decrease in loan receivables. This year, it slightly increased by 9.33 billion won to 893.3 billion won compared to the previous year, but this is a small figure compared to the aggressive management of nearly 1 trillion won in loan receivables in the past. This is why there are market speculations that the loan business might be downsizing.

Authorities Plan "Premier League"... If Loan Industry Shrinks, Low-Credit Borrowers Will Inevitably Suffer

The loan industry’s current trajectory is analyzed to be due to the scheduled reduction of the legal maximum interest rate in July. The cost of funds for loan companies typically includes a bad debt cost (unrecoverable money) of 10-12%. Since the lowest credit rating borrowers are concentrated, defaults or delinquencies are common. Additionally, brokerage fees are about 4%, and the cost of funds is known to be in the 6% range. The cost alone reaches at least 20-22%, and when labor and related expenses are added, under the 20% maximum interest rate system, negative margins are inevitable.

The Financial Services Commission announced in March that it plans to establish a "Loan Premier League" system that provides institutional incentives if low-credit borrowers’ loan approvals and legal compliance are met. Selected companies will be allowed to procure funds from commercial banks. Currently, loan companies raise funds through capital or savings banks. If they can borrow money from commercial banks at around 3-4% interest rates, as the industry claims, they can cover losses.

However, there is skepticism within the loan industry. Only a few companies can be selected for the Premier League, and even if selected, borrowing from commercial banks is thought to have strict conditions. There is also criticism that banks have little incentive to participate.

If the loan industry shrinks despite various measures, experts warn that the damage will ultimately fall on low-credit borrowers. Currently, the loan approval rate in the loan industry is around 10%, meaning 9 out of 10 applicants are rejected. Vulnerable groups who need urgent funds but find it difficult to get loans are likely to turn to illegal private financing.

According to a recent study by the Korea Inclusive Finance Agency, 69.9% of those rejected by loan companies obtained loans from illegal private lenders at rates exceeding the legal interest rate. It is estimated that 30% of borrowers pay interest exceeding the principal, and 12.3% of vulnerable groups pay interest rates over 240% annually.

The Korea Inclusive Finance Agency emphasized, "The interest costs borne by illegal private finance users are not only economic costs but also social costs," and added, "There is a need to introduce a flexible application method for the maximum interest rate, which has been unilaterally lowered, to better suit economic conditions."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}