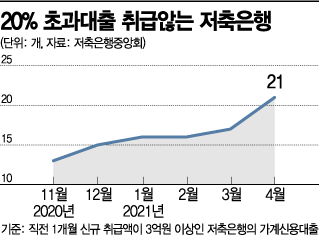

55% of Savings Banks Do Not Exceed 20% Overloan Limit

Small Businesses Face Suspension of Low-Credit Loans

Warnings of Vulnerable Groups Turning to Illegal Private Loans

[Asia Economy Reporter Song Seung-seop] The savings bank industry is rapidly reducing the proportion of high-interest loans exceeding 20% per annum ahead of the legal maximum interest rate reduction scheduled for July. Unlike large savings banks that have adjusted their interest rates, some small-scale firms have stopped lending to low-credit borrowers, raising concerns that a 'loan cliff' may be becoming a reality.

According to the Korea Federation of Savings Banks on the 22nd, among 38 savings banks handling household credit loans, 21 were found not to offer loans exceeding 20%. This is an increase of four from last month, surpassing half (55.26%) of the total. Considering that only 10 banks refrained from high-interest loans when the government and the Democratic Party finalized the maximum interest rate reduction plan last November, the move to reduce high-interest loans appears to be accelerating.

The legal maximum interest rate of 20% was a campaign pledge by President Moon Jae-in and was previously reduced once from 27.9% to 24% in February 2018. Subsequently, in September last year, the government instructed the Financial Services Commission to review the market impact of the interest rate reduction. Following this, amendments to the Loan Business Act and the Interest Limitation Act enforcement decree were made, and the maximum interest rate is set to be lowered to 20% on July 7.

Large savings banks that still maintain loans exceeding 20% are also gradually lowering their proportion. A savings bank official explained, "Large firms are providing loans to as many low-credit borrowers as possible, which is why loans exceeding 20% still remain," adding, "We are adjusting interest rates gradually, and once the maximum interest rate reduction is implemented, we plan to retroactively apply the reduced rates to most loan borrowers."

Small Savings Banks Halt New Loans to Low-Credit Borrowers... Is the 'Loan Cliff' Approaching?

The issue lies with some small and medium-sized savings banks that have begun to stop new loans to low-credit borrowers. A savings bank located in Jeonbuk lent money even to borrowers with a credit rating of 10 in November. However, by April, loans were only extended to borrowers with a rating of 9 (credit score between 445 and 514). Similarly, a savings bank in Incheon previously allowed loans up to an 8th-grade rating, but from this month, borrowers must have a credit score between 601 and 700 to qualify for a loan.

Unlike large savings banks, small-scale firms find it difficult to withstand profit declines due to interest rate cuts. It is interpreted that they are not lowering loan interest rates for low-credit borrowers but are instead ceasing to handle new loans altogether. Another savings bank official analyzed, "Small savings banks are already in a deteriorated management situation," adding, "The decision was likely unavoidable due to the impact of the interest rate reduction."

Industry and academia have long expressed concerns that reducing the interest rate to 20% could drive vulnerable groups toward illegal private loans. The Korea Inclusive Finance Agency recently pointed out in a study that "after being rejected for loans by licensed lenders in 2018, the proportion of borrowers who took loans exceeding the legal maximum interest rate from illegal private lenders actually increased to 69.9%." The Credit Finance Research Institute also warned that after the maximum interest rate reduction, side effects such as increased use of illegal lending in Japan have occurred.

Professor Sung Tae-yoon of Yonsei University's Department of Economics said, "Although it may have started with good intentions, it was a policy expected to have side effects," and criticized, "If the goal was to reduce the interest burden, it should have been addressed through policy support rather than financial intervention."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}