[Asia Economy Reporter Ji Yeon-jin] Since the beginning of the year, volatility has increased in financial markets worldwide, including South Korea. Market interest rate hikes triggered by inflation concerns and early normalization of monetary policy have unsettled financial markets. In particular, in the domestic stock market, foreign investors have switched to net selling in both the stock and government bond futures markets, causing stock prices and bond prices to show relatively weaker performance compared to advanced countries. The won-dollar exchange rate has also risen for two consecutive months, reaching the 1,120 won level.

On the 7th, Ha Geon-hyung, an economist at Shinhan Financial Investment, analyzed, "The Korean economy and financial markets have many similarities to the first half of 2004," adding, "At that time, the Korean and global economies were going through several external shocks such as the dot-com bubble in early 2000, the September 11 attacks in 2001, and the spread of the SARS epidemic in 2003, after which a full-scale demand recovery began."

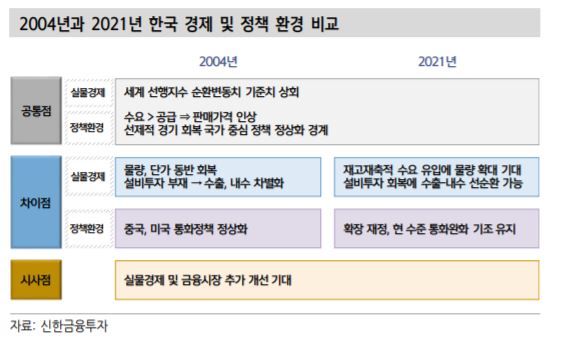

In 2004, the global economy entered an expansion phase. Under a favorable external environment and policy conditions, growth accelerated in major countries. A demand environment exceeding supply was formed due to the inflow of inventory restocking demand, leading to rising sales prices. Major countries sought monetary policy normalization amid the economic upswing.

This year, too, the recovery pace is rapid due to expansionary fiscal and monetary easing policies. Price increases have occurred amid supply chain disruptions. The recent heightened caution regarding policy normalization is also a common factor.

However, there are differences from 2004. Compared to 2004, when inventory restocking demand inflow and volume recovery had already begun, this year has not seen a full-scale inflow of inventory restocking demand. The SARS outbreak was resolved early in the first half of 2003, and proactive inventory restocking demand continued for nearly a year from the second half of that year. In contrast, the current prolonged COVID-19 pandemic has left uncertainties, so inventory restocking demand has not flowed in. South Korea’s manufacturing and wholesale/retail shipment inventory ratios have fallen to late 2018 levels. Except for China, which proactively ended the COVID-19 crisis, most countries including the U.S. and Europe are keeping inventories to a minimum.

The environment accompanied by investment also differs. In 2004, investment expansion did not accompany, resulting in differentiation between exports and domestic demand. Currently, with investment occurring, a virtuous cycle between exports and domestic demand is being formed. Lastly, since the income conditions of vulnerable groups have not improved, expansionary fiscal and monetary easing policies are expected to continue through this year.

Although volatility has increased in the Korean financial market this year, it is premature to discuss peaks in both the economy and policy. Considering inventory restocking demand and investment cycles, the economy is expected to remain strong for at least six more months. The earliest expected timing for policy normalization is from next year. While concerns may be preemptively reflected from the second half of this year, positive factors are expected to dominate from at least the second quarter. Economist Ha stated, "Currently, the Korean economy and financial markets are in a similar position to 2004," but added, "Unlike then, when economic and financial market momentum peaked and declined, there is a high possibility of further improvement now."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}