BIS Estimates 'Credit Gap' at 16.9%P... Highest Ever

Private Debt Growth Relative to GDP Faster Than During Foreign Exchange and Financial Crises

Household and Corporate Debt Increasing Faster Than in US and China

[Asia Economy Reporter Eunbyeol Kim] Following the COVID-19 crisis, corporate and household debt has surged sharply, pushing South Korea's private debt risk level to an all-time high. The pace at which private debt has increased relative to the size of the economy has been faster than during the Asian Financial Crisis and the Global Financial Crisis. While the economic scale shrank due to reduced consumption and production caused by the COVID-19 shock, asset prices such as stocks and real estate soared, resulting in many people borrowing to invest.

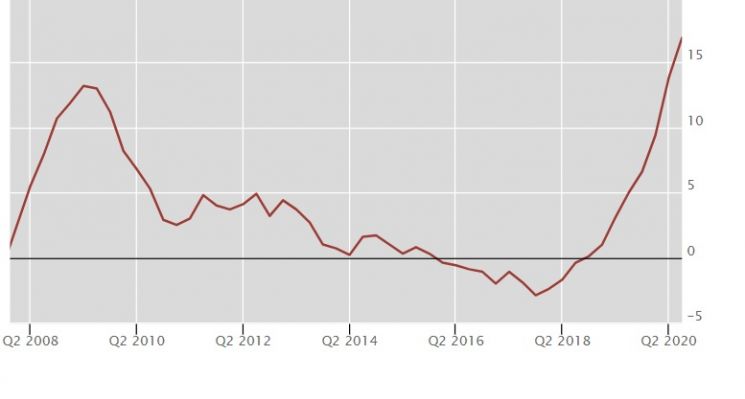

According to the Bank for International Settlements (BIS) as of the end of the third quarter last year, South Korea's Credit-to-GDP gap stood at 16.9 percentage points (P), up 3.1%P from the previous quarter (13.8%P). In the second quarter of last year, it exceeded 10%P for the first time in over a decade since the financial crisis, and this time it surged to the highest level ever recorded.

The Credit-to-GDP gap is a debt risk assessment indicator that shows how much the ratio of private credit (household and corporate debt) to nominal Gross Domestic Product (GDP) deviates from its long-term trend. The faster the ratio of household and corporate debt to GDP increases compared to the past, the larger the gap becomes. Generally, a Credit-to-GDP gap below 2%P is considered normal, between 2%P and 10%P is cautionary, and above 10%P is classified as an alert stage. According to the Bank of Korea, as of the end of the third quarter last year, household debt was approximately 1,682 trillion won, and corporate debt was 1,332 trillion won. Last year, household debt exceeded GDP for the first time, and combined private debt, including corporate debt, far surpassed twice the GDP.

South Korea's private debt growth rate ranks eighth among the 44 countries surveyed by BIS, indicating a rapid increase compared to other nations. It is higher than countries such as China (10.7%P), Brazil (6.6%P), Argentina (6.6%P), Mexico (5.4%P), and the United States (4.9%P). Compared to the fourth quarter of 2019, before the COVID-19 outbreak, South Korea's increase exceeded 10%P, surpassing Brazil (3.7%P), Argentina (4.4%P), and Thailand (9.3%P). Notably, unlike South Korea, countries like China, Mexico, and Argentina have seen their Credit-to-GDP gaps decrease recently, showing signs of recovery.

Although South Korea's debt burden is growing, the views of domestic financial authorities differ somewhat. While acknowledging the rapid increase in debt, they do not consider the 'quality' of the debt to be poor. This assessment is based on indicators such as the household debt delinquency rate (bank household loan delinquency rate at 0.22%) and the capital adequacy ratio (16.02%), which reflects the resilience of financial institutions to defaults, both of which far exceed recommended levels.

South Korea's household loans have a high proportion of mortgage loans, and even in the worst-case scenario, collateral exists. Additionally, due to cultural characteristics, it is rare for Koreans to default on principal and interest payments to the extent of losing their homes, which is another reason financial authorities view the situation positively. The Bank of Korea's own estimate of the Credit-to-GDP gap, reflecting South Korea's specific circumstances, is reportedly better than the BIS assessment. However, caution is advised as interest burdens on companies could surge if loan interest rates rise during the economic normalization process.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}