[Asia Economy Reporter Lee Seon-ae] As the U.S. 10-year Treasury yield surged sharply, causing the domestic stock market to plunge, investors' attention is focused on the possibility of the Federal Reserve (Fed) shifting to a tightening stance.

According to the Korea Exchange on the 27th, the KOSPI index closed at 3,012.95, down 86.74 points (-2.80%) from the previous trading day. The KOSDAQ index closed at 913.94, down 22.27 points (-2.38%). This is interpreted as a result of the surge in the U.S. 10-year Treasury yield.

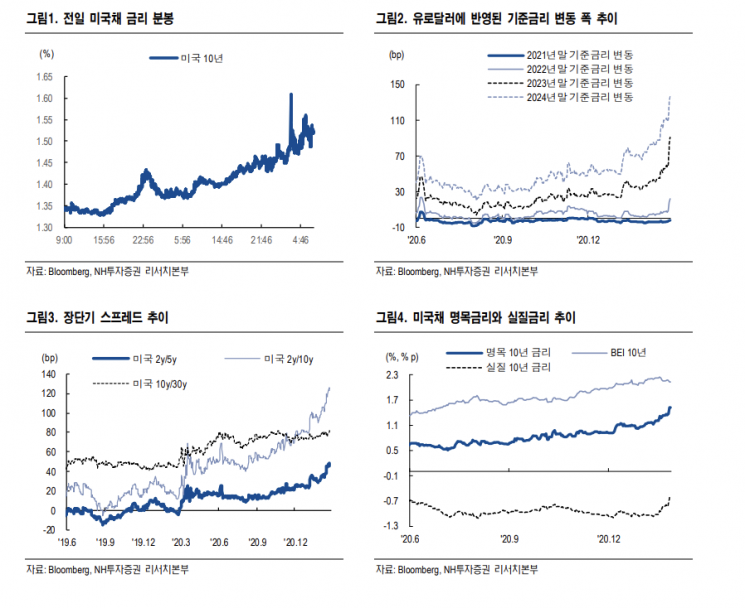

NH Investment & Securities presented an annual outlook last November, suggesting the upper limit of the U.S. 10-year Treasury yield between March and April to be 1.50%. The core rationale was that the U.S. Treasury yield would inevitably rise whether the Fed is trusted (inducing an overshoot in inflation) or not (no shift to tightening), but the Fed would intervene above 1.5% to maintain real interest rates stably.

From this perspective, the upward trend reversal of U.S. Treasury yields since August 2020 can be divided into trust in the Fed (expansion of expected inflation) and distrust in the Fed (possibility of the Fed shifting to tightening). Until January this year, the rise in U.S. Treasury yields was accompanied by an expansion of BEI (bond market's expected inflation), maintaining real interest rates stably. Ultimately, the rise in U.S. Treasury yields until January was mostly due to trust in the Fed.

However, considering that BEI slightly declined despite the sharp rise in U.S. Treasury yields on the 25th, the surge in yields is judged to be mainly due to market concerns about distrust in the Fed, i.e., the possibility of an earlier tightening by the Fed.

In the end, the question "Is further rise in U.S. Treasury yields possible?" can be rephrased as "Will the Fed actually shift to tightening?" NH Investment & Securities judges this to be unlikely. Currently, the Fed is focusing on full employment among its dual mandate (full employment and price stability). Researcher Kang Seung-won of NH Investment & Securities stated, "The biggest reason the market doubts the Fed is Chair Yellen's remark that 'with additional economic stimulus, full employment could be achieved within a year at the earliest.'"

It should be noted that the natural unemployment rate currently presented by the Fed is 4.1%, which was revised downward just before COVID-19 (December 2019 FOMC). At the December 2019 FOMC, the Fed lowered the natural unemployment rate forecast from 4.2% to 4.1%. Notably, at that time, the U.S. unemployment rate was 3.6%, 0.5 percentage points below the natural rate. The problem was that despite employment being below the natural unemployment rate, there was no demand-side inflationary pressure, and the Fed was even conducting unlimited RP purchases. In other words, it is judged that the U.S. natural unemployment rate is likely below 3.5%. Considering this, achieving full employment targeted by the Fed is expected to be difficult even in 2023.

Researcher Kang said, "Although it is acknowledged that doubts about the Fed (somewhat early shift to tightening) are unlikely to be dispelled due to aggressive government spending and the COVID-19 base effect, it is judged that the sharp rise in U.S. Treasury yields due to tightening concerns is unlikely to continue," adding, "Considering the market's herd behavior, there is room for further rise in U.S. Treasury yields, but we have entered a phase where the pace of yield increase is slowing, and the nature of the yield rise is expected to be led again by expected inflation, with real interest rates stabilizing downward."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}