[Asia Economy Reporter Lee Seon-ae] Investment advice has been raised emphasizing the need to pay attention to neglected stocks. The upcoming spring stock market highlights 'interest rate hikes' and 'resumption of short selling' as key keywords, both of which are judged to draw attention to neglected stocks.

Start of the Neglected Stocks Market

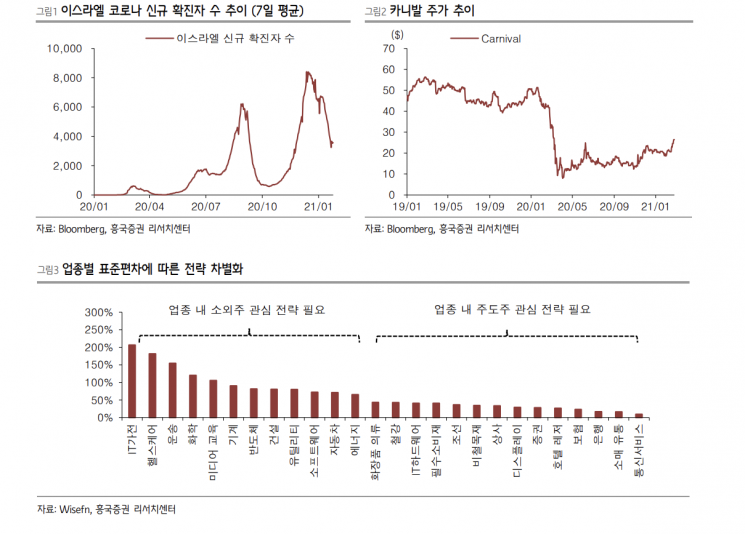

According to Heungkuk Securities on the 28th, neglected stocks have been spotlighted recently for three reasons. First, it is judged that investors are betting on the global market's eventual control of COVID-19. In fact, the number of confirmed COVID-19 cases worldwide has been trending downward since the beginning of the year, and this trend is expected to continue throughout the year. This is because, in addition to the existing vaccine schedule, Johnson & Johnson's vaccine is expected to receive additional approval. Therefore, as vaccination rates continue to strengthen, herd immunity expectations in major advanced countries are likely to increase in the second half of the year. The recent simultaneous easing of lockdowns in major European countries and the marked decline in confirmed cases in California, a large-scale area in the U.S., are particularly positive signals.

Next, the core keywords for the domestic stock market's spring season over the next three months are 'interest rate hikes' and 'resumption of short selling.' Interest rate hikes can symbolize a strong economic recovery. Recent capital outflows in the bond market are judged to be due to the realization of economic recovery following strong indicator improvements rather than supply-demand or thematic factors. Interest rate hikes are likely to act as a buying trigger for undervalued cyclical stocks, while the resumption of short selling is expected to burden overvalued growth stocks, making a 'sell overvalued growth stocks & buy undervalued cyclical stocks' long-short strategy more active. Researcher Byun Jun-ho of Heungkuk Securities advised, "Historically, interest rate hikes have caused value stocks to outperform, and the resumption of short selling has pressured high-valuation bio and KOSDAQ markets in the short term," adding, "Both interest rate hikes and the resumption of short selling lead to increased interest in neglected stocks."

Lastly, the strong performance of U.S. cruise company Carnival's stock has begun. While most U.S. stocks rose with the market, cruise companies' stocks had difficulty rebounding due to the ban on cruise travel. However, Carnival's stock hit bottom in mid-February and began a sharp upward trend. This reflects expectations that global cruise voyages will resume. Given the nature of cruise travel, which requires large groups to travel together, the strong performance of cruise company stocks can be interpreted as a very strong signal of the end of COVID-19. The fact that Carnival's stock has started to strengthen is ultimately judged as a signal for the rise of neglected stocks in Korea.

How to Buy Neglected Stocks

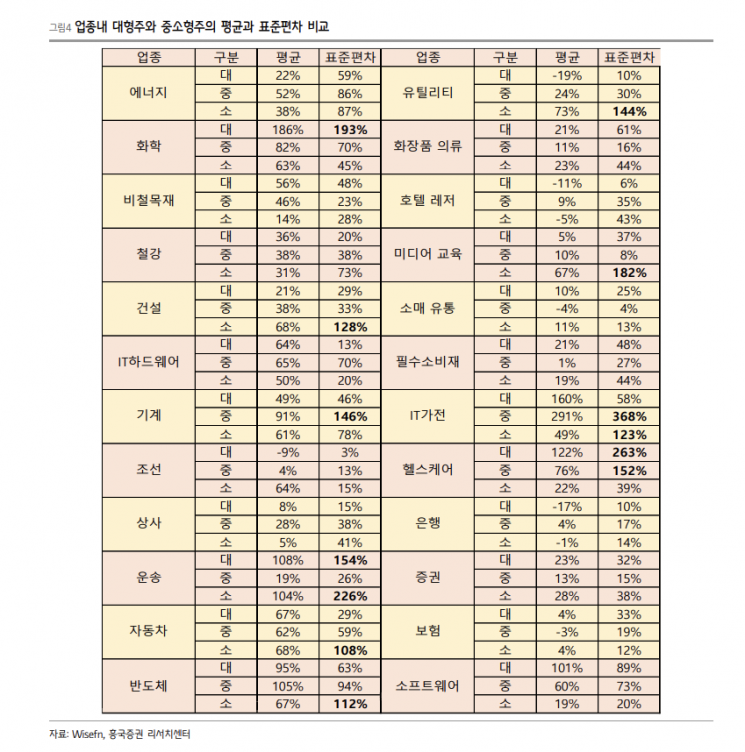

So, how should one approach buying neglected stocks? The method involves using the standard deviation of returns among stocks within an industry. Although stock price movements within an industry are generally similar, there are differences in returns, which can be utilized as the standard deviation of returns. If the standard deviation of returns among stocks in an industry is large, it means there is a significant return gap between stocks, so the possibility of price gap filling by neglected stocks within the industry is high. Conversely, if the standard deviation of returns is small, it means there are no significantly rising stocks or the strength of leading stocks' rise is weak, so chasing high-return leading stocks may be advantageous. If our interest is to effectively approach neglected stocks, a strategy of buying less-risen stocks within industries or groups with large return standard deviations can be effective. This can also be examined by dividing stocks into three return groups based on market capitalization within an industry: large-cap, mid-cap, and small-cap. By understanding the average return and its standard deviation for large, mid, and small-cap groups within an industry, one can strategize whether to approach leading stocks or neglected stocks in each size group.

Researcher Byun said, "Based on returns and standard deviations calculated from prices compared to the end of 2019 (distinguishing industries where neglected stocks or leading stocks should be bought and effective neglected stock buying strategies within them), attention is needed for chemical large-cap neglected stocks, construction small-cap neglected stocks, machinery mid-cap neglected stocks, transportation large and small-cap neglected stocks, automobile small-cap neglected stocks, semiconductor small-cap neglected stocks, media education small-cap neglected stocks, IT home appliances mid and small-cap neglected stocks, and healthcare large and mid-cap neglected stocks."

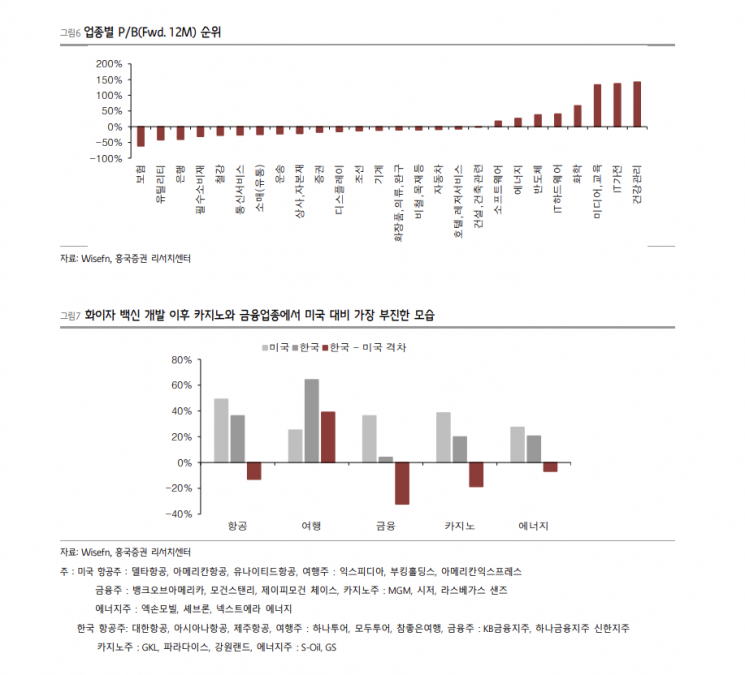

Next is the utilization of the large-cap stock price-to-book ratio (P/B) coefficient of variation decline cycle. Since last summer, the coefficient of variation of large-cap P/B ratios has been on a downward trend. This means that the P/B gap among large-cap stocks is narrowing. The significant rise in low P/B large-cap stocks is causing the P/B gap within large caps to shrink. The rise and fall of the large-cap P/B coefficient of variation are mainly determined by pharmaceutical and bio stocks. When growth stocks and pharmaceutical bio stocks outperform the market, the P/B coefficient of variation rises; conversely, when pharmaceutical bio stocks underperform relatively and value stocks strengthen, the P/B coefficient of variation falls. The decline in the P/B coefficient of variation since last summer is also a result of the relatively weak relative price performance of pharmaceutical bio stocks. As economic recovery is materializing in indicators, interest in cyclical stocks, which are relatively economically sensitive, is expected to continue rather than pharmaceutical bio stocks, which have a defensive nature, and with the resumption of short selling approaching, sentiment toward pharmaceutical bio stocks is likely to be weak.

Researcher Byun said, "Attention should still be paid to low P/B industry groups that have not risen much," adding, "Interest will increase in industry groups that are still significantly below the average P/B since 2010, including financial industries centered on insurance, and materials and industrials centered on transportation and steel."

Lastly, the approach is to buy inflation and leisure-related stocks that have risen less compared to overseas. This involves finding industries such as airlines, travel, casinos, energy, and finance that have risen less compared to overseas trends. The price strength of inflation and leisure-related stocks began in earnest after Pfizer's vaccine development news in November last year. Comparing the price increase rates from that point to the present, if domestic industry groups have risen relatively less, this can be a justification for price increases. Looking at the rise rates since early November after Pfizer's vaccine development, except for travel, the casino, finance, energy, and airline sectors showed relative underperformance compared to the U.S. Among COVID-19 affected stocks, there is a high possibility of opportunities in casino, finance, and energy sectors. Among these, finance and casino stocks are judged to have the greatest potential for price increases.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}