Individual Retirement Pension Subscribers Surge from 750,000 in 2015 to 20.18 Million in 2019

45.3% Have Subscription Periods of 1-3 Years, Only 7.9% Subscribed for Over 5 Years

30% of Applicants Earn Over 100 Million Won Annually, 1% Earn Under 30 Million Won

Half of Early Withdrawals Due to 'Housing Costs'...Return Rate Low at 1.56% for Guaranteed Plans

[Asia Economy Reporter Wondara] It has been analyzed that more than half of individual retirement pension (IRP) subscribers cancel their accounts within 1 to 3 years. A 'polarization' phenomenon according to income brackets has also emerged.

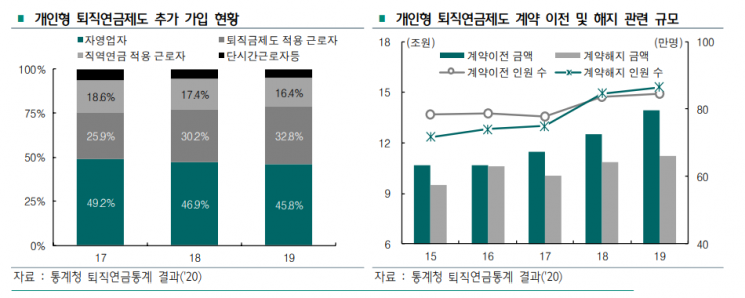

According to Hana Financial Management Research Institute's Hana Financial Focus published on the 17th, due to the influence of the Employee Retirement Benefit Security Act, the average annual growth rate of the individual retirement pension market over the past four years reached 24%. The number of individual retirement pension subscribers surged from 750,000 in 2015 to 2.08 million in 2019, and the balance of accumulated funds more than doubled from 10.8 trillion won to 25.4 trillion won.

However, it was confirmed that most subscribers cancel their individual retirement pensions within a short period. Among all subscribers, 45.3% had an IRP subscription period of 1 to 3 years. The proportion of those subscribed for more than 5 years was only 7.9%. The number of contract cancellations reached 865,000, and the cancellation amount was 11.2 trillion won. Since 2018, the number of cancellations has surpassed new subscriptions.

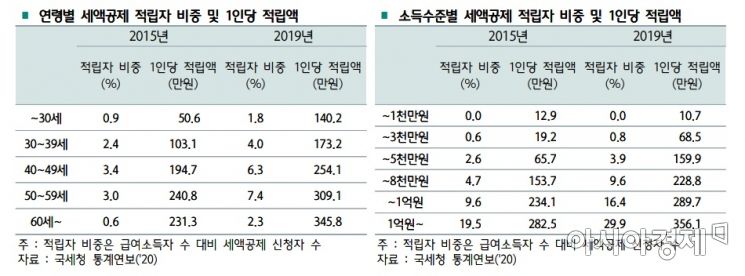

Although individual retirement pensions are considered a social safety net to supplement public pensions, the number of high-income subscribers has increased. The proportion of subscribers with an annual income of 30 million won or less is less than 1%, whereas the proportion in the income bracket of 80 million won or more exceeded 10%. The proportion of applicants with over 100 million won also increased significantly from 19.5% in 2015 to 30% in 2019. Over the past four years, the accumulated amount per person under 10 million won decreased, while other income brackets increased by up to about 3.5 times.

"Who maintains an individual retirement pension with low returns when they don't even have money to pay rent?"

The causes of this short-term trend and polarization are pointed out to be the burden of having to lock funds until age 55 while returns are low, and the tax deduction benefits, which were incentives, are designed to favor only high-income earners. In the case of early cancellation of an individual retirement pension, a 16.5% tax must be paid on the sum of the tax-advantaged contributions and investment returns. Unlike general retirement pensions, early cancellation is not recognized for reasons such as home purchase or securing jeonse (key money deposit) or rental deposits. Although the tax credit limit was expanded from the existing 4 million won to a maximum of 7 million won annually in 2015, the average annual accumulated amount per tax credit applicant was only 2.52 million won as of 2019.

Increased 'home acquisition costs' are also a major reason for early withdrawal from individual retirement pensions. According to the reasons for early withdrawal from retirement pensions compiled by Statistics Korea in 2019, home purchase (30.2%) and housing rent (22.3%) accounted for more than half. Other reasons included long-term care (37.7%) and rehabilitation procedures (9.3%). By age group, those in their 30s accounted for the largest share at 38.8%, followed by 40s at 34.3%, 50s at 19.4%, and 20s at 5.5%. Among those in their 30s, 18,522 subscribers cited home purchase and housing rent as reasons, the highest number.

Tax benefits should be applied differentially by age and income level... Measures to increase investment returns are urgently needed

Another limitation is the reduced capacity of individuals to pay into long-term products like retirement pensions due to the recent increase in household debt. The average household income growth rate was 1.7% as of 2019, but the ratio of financial debt to savings was 73.1% as of March 2019. Returns are also low. The average return on individual retirement pensions at the end of last year from 14 securities firms, 12 banks, and 17 insurance companies was only 1.56% annually for the principal-guaranteed type, which accounts for 73% of all subscribers. While individual retirement pensions are praised for allowing investment in various financial products such as funds and bonds, only up to 40% of the investment can be allocated to stocks even during a 'stock boom.'

Experts advise that the government should establish measures to make tax credit benefits more effective and to increase returns. Hee-Soo Jung, a research fellow at Hana Financial Management Research Institute, said, "Currently, the tax credit benefits do not provide a strong incentive for individuals to subscribe to retirement pensions," adding, "It is necessary to apply tax benefits differentially by age or income level." He continued, "Consideration should be given to providing additional economic benefits to long-term subscribers of 5 or 10 years or more," emphasizing, "Measures to increase investment returns, such as introducing a pre-designated management system, should also be prepared."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}