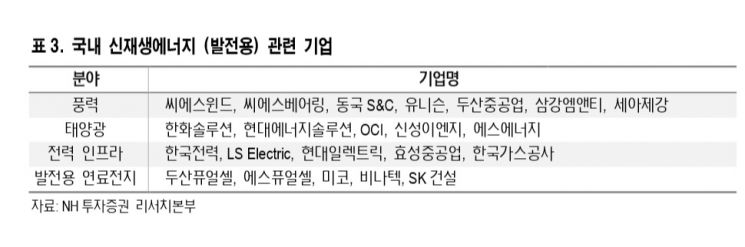

[Asia Economy Reporter Oh Ju-yeon] In 2020, domestic and international renewable energy-related policies were announced, leading to strong stock performance of related companies. In 2021, renewable energy policies are expected to become more concrete, making the mid- to long-term performance growth of these companies more visible. Accordingly, there is growing interest in whether the stocks that rose last year due to the Green New Deal policy and future expectations can continue to rise this year.

On the 1st, NH Investment & Securities evaluated the 5th Basic Plan for Renewable Energy announced by the Ministry of Trade, Industry and Energy as meaningful in that the policy was concretized to achieve carbon neutrality by 2050, and the mid-term deployment plan was also revised upward until 2025.

This policy includes raising the share of renewable energy in total power generation from 21.6% in 2030 to 25.8% in 2034, an increase of 4.2 percentage points, and newly deploying 65.1GW of renewable energy facilities by 2034. NH Investment & Securities focused on the fact that the renewable energy deployment target by 2025 was raised from 29.9GW to 42.7GW. Furthermore, to achieve carbon neutrality by 2050, improvements in renewable energy efficiency, expansion of potential capacity, power grid transition, and the spread of hydrogen energy to complement the shortcomings of renewable energy are necessary. From a mid- to long-term perspective, policy strengthening to address these tasks is inevitable. This is expected to support the mid- to long-term valuation increase of domestic renewable energy-related companies.

Researcher Jeong Yeon-seung analyzed, "This policy covers five areas: deployment, demand, market, industry (competitiveness), and power infrastructure."

Researcher Jeong predicted, "From the deployment policy perspective, the introduction of large-scale power plants utilizing state-owned land is expected to be possible, and from the demand perspective, the demand sources for renewable energy will diversify from existing power companies." Additionally, from the industry perspective, supporting the localization of core technologies is expected to be followed by facility investments for the advancement of power infrastructure.

He anticipated that this year, rather than presenting policies from a macro perspective, announcements will continue focusing on the concretization of detailed policies. Looking at the domestic market, subsequent policies are expected to include the introduction of the HPS (Hydrogen Power Obligation) system to build and strengthen the hydrogen ecosystem, enabling direct power trading contracts between renewable energy operators and power consumers through amendments to the Electricity Business Act, raising the RPS (Renewable Portfolio Standard) ratio, and expanding the obligated suppliers.

Researcher Jeong particularly forecasted that hydrogen and offshore wind power will show the most remarkable growth among detailed power sources. Regarding hydrogen, he explained that it is distinguished as an independent system from the existing renewable energy competition, reflecting the intention to expand the hydrogen ecosystem, and that hydrogen-related policy announcements will continue in 2021. He also noted that offshore wind power is a power source whose generation share is rapidly increasing among renewable energies, with installations set to begin in earnest domestically and internationally from 2023, maintaining a positive view on the offshore wind power value chain.

Researcher Jeong said, "There are concerns about whether there is room for further stock price increases given the rapid expansion of valuations from the perspective of renewable energy investment. However, as detailed policies are being concretized and new projects are expected to increase through full-scale capital investment, there are no clear factors that would cause a decline in the valuations of renewable energy companies."

He added, "At this point, it is judged that a positive view should be maintained continuously for companies where detailed policy concretization can be linked to actual performance," and "a mid- to long-term holding strategy is valid, focusing on companies with high export ratios, those that have concretized mid- to long-term growth plans, and those that can lead the global market."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}