Five Major Banks' LCRs Below 100% Except Nonghyup

Burden of Separately Raising Funds in Banking Sector

Time Deposits with 0% Interest Rates Ignored Amid Surging Loans

[Asia Economy Reporter Park Sun-mi] While loans are surging, time deposits with interest rates in the 0% range are being shunned by consumers, putting the banking sector on high alert to maintain the Liquidity Coverage Ratio (LCR). The LCR is an indicator that shows a bank's ability to absorb shocks, and a lower figure implies increased vulnerability to liquidity crises.

According to the financial sector on the 4th, as of the end of the third quarter, the average LCR of the five major banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?stood at 94%. All five banks saw their LCR decline compared to the previous quarter, ranging from a decrease of 2.49 percentage points to as much as 8.08 percentage points. Notably, except for Nonghyup (100.21%), Kookmin (91.5%), Shinhan (92.6%), Woori (93.5%), and Hana (95.6%) all fell below the minimum mandatory holding ratio of 100% set by financial authorities.

The LCR represents the ratio of high-quality liquid assets to the expected net cash outflows over the next 30 days, serving as a key indicator of a bank's soundness. To prepare for situations where large sums might temporarily flow out during financial crises, regulators have set the minimum LCR at 100%. Currently, due to the COVID-19 pandemic, financial authorities have lowered the minimum LCR to 85% until March next year to encourage active lending by banks. However, after March, banks will face the burden of having to raise funds separately.

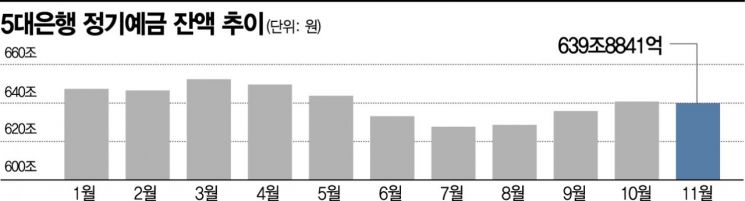

The decline in LCR is attributed to a decrease in time deposits. As of the end of November, the balance of time deposits at the five major banks was KRW 639.8841 trillion, down KRW 841.5 billion from KRW 640.7256 trillion at the end of October. Compared to KRW 647.3449 trillion in January this year, it decreased by KRW 7.4607 trillion, indicating that customers are losing interest in time deposit products offered by banks.

Decrease in Bank Time Deposit Balances Due to Paltry Interest

The decrease in bank time deposit balances is largely influenced by the 'paltry' interest rates.

The time deposit interest rates applied by the five major banks, as disclosed by the Korea Federation of Banks, range from 0.45% to 0.90% for a 12-month term, not even reaching 1%. Depositing KRW 10 million for one year yields an average interest of about KRW 60,000 to 70,000, which after a 15.4% tax deduction, amounts to roughly KRW 50,000 annually. While preferential interest rates can raise this to 0.90%?1.20%, these require meeting stringent conditions set by each bank, such as fulfilling credit card usage requirements or setting up automatic payments for utilities and management fees, making it difficult to qualify. Just a year ago, bank deposit interest rates were around 1.5%, but with the ongoing low-interest-rate environment, banks have competitively lowered deposit rates, leading customers to avoid bank time deposits.

The demand deposit balances of the five major banks reached KRW 566.1113 trillion as of the end of November, an increase of KRW 16.383 trillion from October and KRW 111.8347 trillion compared to the beginning of the year. This shows that customers prefer demand deposits, which allow them to withdraw funds freely at any time for high-yield investments, even if it means foregoing interest, rather than locking money in time deposits for over a year to earn 'meager' interest. The surge in 'Yeongkkeul' (borrowing to the max) and 'Bittou' (investing with borrowed money) trends has led many to take out unsecured loans and temporarily park funds in demand deposit accounts before investing in stocks or real estate, contributing to the decline in time deposits and the rise in demand deposits.

Accordingly, the banking sector is putting all efforts into managing the LCR amid stagnant or declining time deposits, in contrast to the rapidly increasing loans, but the burden is growing. A bank official said, "When liquidity is insufficient, banks sometimes sell time deposits in special promotional formats, but in the current situation, to increase liquidity, banks have no choice but to raise funds by issuing bank bonds and operate funds in highly marketable assets such as government bonds or monetary stabilization bonds."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}