Local Government-Owned State Enterprises' Debt No Longer Supported

Defaults in Bond Market Surge Over 10 Times Since 2015

[Asia Economy Reporter Hyunwoo Lee] The Chinese government recently announced a zero-tolerance policy, stating it will no longer support large state-owned enterprises (SOEs) amid a series of defaults. This move aims to curb the previous practice of borrowing to repay debts, leading to expectations that the default crisis will continue for some time. Particularly, if SOEs undergo a chain of bankruptcies, not only the connected local governments but also small local financial firms face a high risk of insolvency, lending credibility to the view that the Chinese government is embarking on a full-scale restructuring of troubled SOEs.

According to the state-run Global Times on the 23rd, the Financial Stability and Development Committee under the State Council held a special meeting chaired by Vice Premier Liu He the day before, deciding to strictly punish financial-related illegal activities by SOEs. The committee analyzed that recent corporate bond defaults among SOEs were caused by various illegal acts, including corporate fraud, improper information disclosure, malicious transfers, and misappropriation of funds.

Previously, SOEs declared defaults one after another. Starting with state-owned Yongcheng Coal Power failing to repay corporate bonds worth 1 billion yuan (approximately 170 billion KRW) on the 10th, semiconductor company Tsinghua Unigroup defaulted on the 16th, followed by Huachen Group on the 20th, all unable to meet bond maturity payments. Yongcheng Coal Power is also scheduled to mature corporate bonds worth 26.5 billion yuan (4 billion USD) this week, raising concerns about additional defaults. Financial authorities are investigating whether there were any irregularities in financial transactions between securities firms, banks, and Yongcheng Coal Power.

Locally, the cause of the chain defaults among SOEs is attributed to the exhaustion of local governments' fiscal capacity, which had been supporting SOEs. Local governments had guaranteed corporate bond issuances but are now unable to provide further support. A major foreign media outlet noted, "SOEs have enjoyed implicit guarantees from local governments regardless of their financial status," adding, "This incident is breaking the trust of Chinese bond investors in SOEs." In this context, the Henan provincial government dispatched a crisis management team to Yongcheng Coal Power, but their scope of action remains very limited due to financial pressures on local governments.

The Chinese government's non-response to this series of defaults has drawn attention. In the past, the central government would have prepared financial support measures before defaults were declared, but this time, no additional support announcements were made even after defaults were declared. This has led to interpretations that the central government intends to expose the weaknesses of SOEs through this opportunity. The Hong Kong South China Morning Post (SCMP), citing sources from the National Development and Reform Commission, reported, "The central government will no longer bail out SOE defaults caused by local governments and will urge them to resolve issues independently and systematically prevent risks."

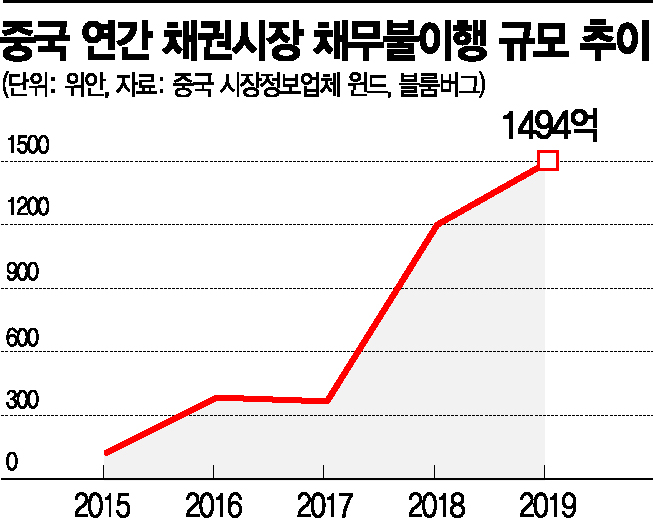

The source added, "Local governments have undertaken too many projects through debt, and these projects have not generated proper returns." Given that China's corporate bond market has grown to the world's second largest, continued support for insolvent companies could significantly damage China's credibility in international financial markets. In fact, the scale of bond market defaults surged from 36.7 billion yuan in 2017 to 120 billion yuan in 2018 and 149.4 billion yuan in 2019, undermining confidence in Chinese bonds.

Since early this year, Chinese financial authorities have begun restructuring small local financial institutions to reduce the risk of chain bankruptcies caused by indiscriminate investment in SOE corporate bonds. According to Xinhua News Agency, the number of local financial firms investing in local corporate bonds, which had proliferated to over 9,000 nationwide since 2015, decreased to 7,333 by the end of the second quarter this year. The China Banking and Insurance Regulatory Commission added regulations in September, mandating that financial firms maintain bond market fundraising at no more than four times their net assets.

Tan Minlan, Chief Investment Officer for Asia Pacific at UBS Global Wealth Management, told CNBC, "The Chinese government has declared it will no longer bail out some companies with very weak credit." He added, "Differentiated support based on companies' credit status can enhance trust in Chinese financial authorities in the long term and help local governments, which are under fiscal pressure due to COVID-19, reduce indiscriminate investments."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}