[Asia Economy Reporter Oh Hyung-gil] Although liquidity in the capital market has increased due to the COVID-19 pandemic, the sales of variable life insurance, a representative investment product of life insurance companies, have not escaped sluggishness.

It is pointed out that life insurance companies need to inform that variable life insurance does not belong to high-risk assets and respond to strengthened regulations related to variable life insurance sales.

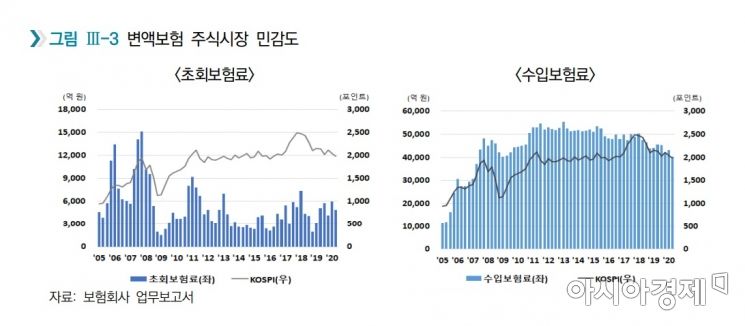

On the 18th, Kim Se-jung, a research fellow at the Korea Insurance Research Institute, stated in the report "COVID-19 and Variable Life Insurance Market Trends" that "In a low-interest-rate environment, the variable life insurance market is emerging as an alternative market to traditional insurance products."

According to the report, since the spread of COVID-19, market liquidity has shown a sharp increase and is flowing into the capital market.

Customer deposits at securities companies were at the level of 20 to 30 trillion won per month last year, but they surpassed 40 trillion won in March 2020, when the stock market hit its lowest point, and approached 50 trillion won in July.

Also, the credit balance, which refers to the size of loans for stock purchases, sharply declined in March 2020 but has been continuously increasing since then.

Researcher Kim diagnosed, "Despite the stock market recovery, variable life insurance sales show sluggish performance," adding, "The first half premium income of variable life insurance decreased by 6.9%, and the monthly initial premiums of variable life insurance actually decreased compared to the same period last year after the stock market sharply rebounded in March."

He also analyzed that the sales of variable life insurance through bancassurance channels, the main sales channel for variable life insurance, were sluggish, acting as a factor weakening the growth of variable life insurance.

He suggested, "Life insurance companies need to develop consumer-friendly products that increase the stock market sensitivity of variable life insurance and respond to the trend of strengthening regulations related to variable life insurance sales by considering channel suitability," adding, "They should strive to develop consumer-friendly fee and product structures and emphasize the advantages of variable life insurance products."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}