Commercial Banks' Total Volume Control 'Speed'

Suspension of Handling and Limit Restrictions

[Asia Economy Reporter Kim Hyo-jin] Major commercial banks are accelerating their efforts to manage total loan volumes as the year-end approaches. This includes temporarily suspending loan product offerings or limiting loan amounts. This is interpreted as a result of a combination of active government intervention and increased need for risk management.

The annual loan growth target, which was raised early in consideration of the impact of the novel coronavirus disease (COVID-19), has been exceeded in the second half of the year due to factors such as 'Youngkkeul (borrowing to the limit)' and 'Debt Investment (debt-financed investment)', further accelerating tightening measures. As banks tighten the reins, it is expected that it will become even more difficult for real demand borrowers who need funds by the end of the year to obtain loans.

According to the banking sector on the 11th, NH Nonghyup Bank temporarily strengthened the Debt Service Ratio (DSR) standards applied when handling housing-related loans starting from the 9th. DSR is a measure that calculates the borrower's principal and interest repayment burden by dividing the annual repayment amount of all household loans by annual income. Until now, NH Nonghyup Bank allowed housing-related loans up to a DSR of 100%, but from the 9th, loans are rejected if the DSR exceeds 80%.

NH Nonghyup Bank also decided to reduce preferential interest rates on major loan products until the end of the year. The maximum preferential interest rate for major mortgage loans will be reduced by 0.4 percentage points, and preferential rates for high-quality credit loans such as 'Exciting Employee Loan' and 'NH Strong Employee Loan' will be reduced by 0.2 percentage points. Lowering preferential rates effectively raises the final interest rate, increasing the loan threshold.

Hana Bank will temporarily suspend new applications for 'Mortgage Credit Insurance (MCI)' and 'Mortgage Credit Guarantee (MCG)' loans starting from the 16th. Using MCI or MCG loans allows homeowners to borrow additional amounts equivalent to small rental deposits. If these loans are not available, the loan limit effectively decreases. Woori Bank also suspended MCI and MCG loans until the end of the year.

Woori Bank has also stopped issuing jeonse loans since the 30th of last month in cases where ▲ ownership of the lessor is transferred ▲ jeonse loans are sought under conditions of cancellation or reduction of senior mortgage rights ▲ customers who have already taken jeonse loans from other banks want to switch to Woori Bank.

KB Kookmin Bank adjusted the DSR standard for KB Mugunghwa Credit Loans (in cooperation with the National Police Agency) and group credit loans from the previous 70% to within 40% as of the 16th of last month. Shinhan Bank, which had applied a DSR of 100% for new customers and 120% for existing customers when setting personal credit loan limits, standardized this to 100% for all customers starting from September.

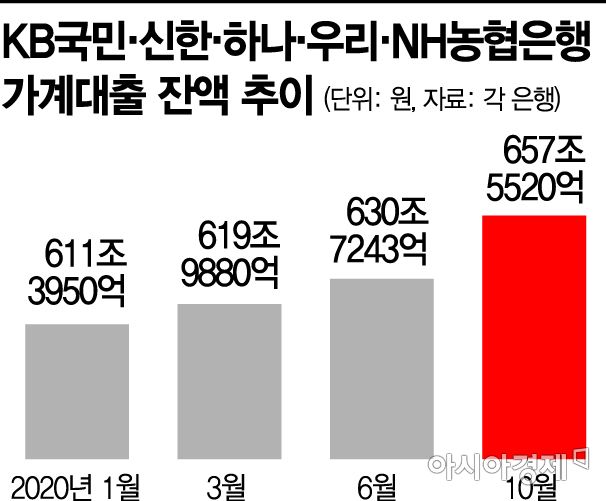

The outstanding household loans of the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?stood at 657.552 trillion KRW at the end of last month, an increase of 7.6611 trillion KRW compared to 649.8909 trillion KRW in September. The increase, which was 8.4098 trillion KRW in August, slightly decreased in September but rose again last month. Meanwhile, the outstanding balance of jeonse loans surpassed 100 trillion KRW for the first time at 101.6828 trillion KRW at the end of last month, continuing the monthly upward trend in total loan volume this year.

Major banks initially set the annual loan growth target at around 4%, but due to increased loan demand from small business owners and SMEs amid the spread of COVID-19, the target was raised to around 6-7%. However, with the surge in 'Youngkkeul' and 'Debt Investment' trends and skyrocketing jeonse prices in the second half of the year, most banks are expected to exceed the raised targets.

Accelerated Management Amid Concerns Over 'COVID-19 Defaults'

Total Household Loans in Financial Sector Increased by 13.2 Trillion KRW in October

The potential accumulation of latent defaults due to extensions of loan maturities for small business owners in response to COVID-19 (until March next year) is also cited as a factor making banks more anxious. A commercial bank official said, "While strict management by the government and financial authorities has had an impact, banks themselves are increasingly concerned about soundness due to COVID-19."

Meanwhile, the government is considering implementing separate measures to curb loans depending on future trends. On the 9th, Hong Nam-ki, Deputy Prime Minister and Minister of Economy and Finance, stated at the National Assembly Budget and Accounts Committee, "The government is actively responding while preparing management plans with caution." Financial authorities have also indicated that they may consider strengthening DSR regulations depending on circumstances.

Meanwhile, total household loans in the financial sector increased by 13.2 trillion KRW compared to the end of September. The increase expanded by 2.2 trillion KRW compared to the previous month (11 trillion KRW) and by 4.9 trillion KRW compared to the same month last year (8.3 trillion KRW).

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}