[Asia Economy Reporter Minji Lee] The Central Bank of Brazil kept the benchmark interest rate steady at 2% during its October monetary policy meeting. It maintained a dovish stance to alleviate concerns in the financial market, but given the expanding inflationary pressures, discussions on raising the benchmark rate are expected to be brought forward sooner than anticipated.

According to the financial investment industry and Korea Investment & Securities on the 1st, the Central Bank of Brazil held the benchmark interest rate at 2% in the October monetary policy meeting. With social distancing measures still in place, the recovery has been asymmetric, leading to the continuation of an accommodative monetary policy. The central bank appears to have maintained forward guidance not to raise the benchmark rate at least until 2021. Although the room is limited, it is analyzed that the possibility of additional rate cuts remains open.

Yeoh Hyun-tae, a researcher at Korea Investment & Securities, said, “Uncertainty about the growth trajectory remains high, but the room for further rate cuts is limited,” adding, “The central bank’s assessment of the economy has not changed significantly, and with fiscal support ending, downward pressure on the economy is expected to increase from the end of the year.” He continued, “As inflation rises sharply, it seems the central bank is calming the financial market, which was concerned about an early end to monetary easing,” and said, “In the short term, the central bank will maintain an accommodative stance and keep the benchmark interest rate at the current level.”

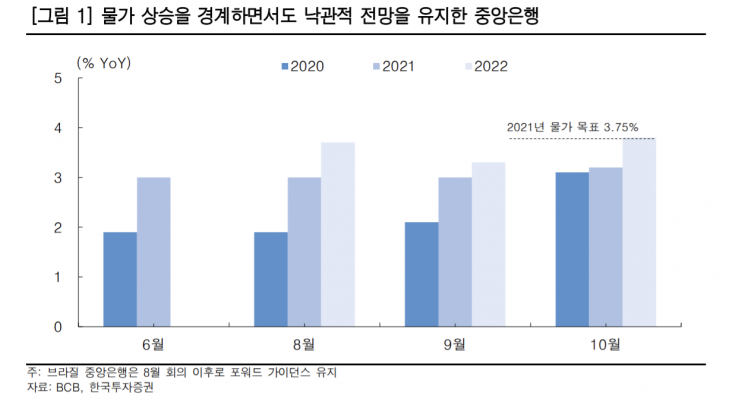

The Central Bank of Brazil acknowledged that inflationary pressures are emerging rapidly but viewed them as temporary. It identified the depreciation of the Real, rising food prices, and disaster relief payments as disruptive factors to inflation. Accordingly, it forecasted annual inflation rates of 3.1%, 3.2%, and 3.8% through 2022.

However, the timing of the benchmark rate hike is likely to be brought forward. These forecasts carry significant upside risks. Due to concerns over fiscal deficits and government debt, a rebound in the Real’s value is unlikely. Food and raw material prices are expected to remain high for an extended period. If real wages rise along with the recovery of the service sector, consumer prices could increase sharply.

In the short term, the central bank is responding to potential depreciation of the Real by intervening in the foreign exchange market. On the 28th, it sold about $1.04 billion, marking the largest intervention of the year. Researcher Yeoh Hyun-tae explained, “If concerns about inflation and fiscal matters are not dispelled, such policies are merely stopgap measures,” and added, “There is room for discussions on rate hikes to be brought forward sooner than expected.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}