7 Card Companies, Multiple Debtors' Delinquency Rates Rise Simultaneously in First Half of Year

Delinquency Rates Higher Among Borrowers with Lower Credit Ratings

Concerns Over Household Debt Defaults

Due to the resurgence of the novel coronavirus infection (COVID-19), difficulties for small business owners are increasing, and a banner announcing business closures is hung in the Goyang Furniture Complex in Gyeonggi Province. Photo by Mun Ho-nam munonam@

Due to the resurgence of the novel coronavirus infection (COVID-19), difficulties for small business owners are increasing, and a banner announcing business closures is hung in the Goyang Furniture Complex in Gyeonggi Province. Photo by Mun Ho-nam munonam@

[Asia Economy Reporter Ki Ha-young] Lee Min-jung (55, pseudonym), who runs a pub, saw customers disappear abruptly this year due to the novel coronavirus infection (COVID-19), making it difficult to even pay the electricity bill, let alone the rent. Although he received a small business policy loan supported by the government, he ultimately could not endure for several months and had no choice but to borrow from multiple financial institutions. Having been rejected by first-tier financial institutions due to a low credit rating, he took out a total of three loans from relatively high-interest savings banks and credit card companies. While he managed to put out the immediate fire, business is still not going well, and repaying the loans seems bleak. Lee said, "With the government's additional support, I don't have to pay interest or principal immediately, but if the economy doesn't improve by next year, I worry about how I will repay this money and can't even sleep."

Concerns are growing that multiple borrowers who have taken out three or more loans from financial institutions could become a ticking time bomb for household debt defaults. This is because the delinquency rates of credit card companies for multiple borrowers with low credit scores have all risen compared to the previous year in the first half of this year. Experts point out that as the proportion of multiple borrowers increases and the repayment ability of low-credit borrowers declines, the credit risk of credit card loan assets inevitably rises.

According to the report titled "Analysis of Potential Asset Deterioration Factors Focusing on Credit Card Multiple Borrowers' Asset Exposure" released by NICE Credit Rating on the 24th, as of the first half of this year, when classifying the total card assets of seven specialized credit card companies (Shinhan, Samsung, KB Kookmin, Hyundai, Lotte, Woori, Hana) by the number of loans per borrower, 38.6% were assets of multiple borrowers holding three or more loans in total. In particular, for loan-type card assets such as cash services (short-term loans) and card loans (long-term loans), the proportion of multiple borrower assets accounted for as much as 62.6% of total card assets during the same period.

Multiple Borrowers Have Lower Credit Ratings and Higher Delinquency Rates

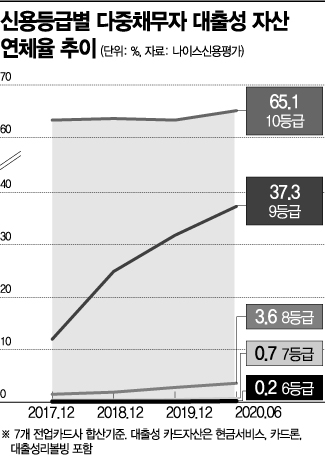

The problem is that multiple borrowers also have very low credit ratings. The more loans they have, the more their credit rating is downgraded, and the lower the credit rating, the higher the delinquency rate. Based on the combined data of the seven specialized credit card companies, the average delinquency rate of multiple borrower assets fell slightly from 2.6% last year to 2.5% in the first half of this year. On the other hand, the delinquency rates of low-credit multiple borrowers (grades 7 to 10) all increased from the end of the previous year to the first half of this year, ranging from 0.1 percentage points to as much as 5.5 percentage points. The delinquency rate for grade 9 in the first half of this year was 37.3%, up 5.5 percentage points from the end of last year, and grade 10 also recorded 65.1%, up 1.8 percentage points from the end of last year.

Furthermore, the recovery rate (cash recovery amount compared to the principal of delinquent loans) has declined due to the expansion of multiple borrowing, which is likely to become a burden during future periods of rising delinquency rates. Since the 2008 financial crisis, the proportion of loans moving from normal to delinquent has decreased due to improved risk management by credit card companies and better repayment ability of borrowers, but loans classified as delinquent are more likely to remain long-term delinquent loans. In fact, when comparing recovery rates during the first half of this year with those during the financial crisis, the total card asset recovery rate dropped by about 50%, from 40.6% at the end of 2008 to 21.4% at the end of June 2020. For loan-type card assets, cash services fell from 35.4% at the end of 2008 to 17.8% at the end of June 2020, and card loans dropped from 26.6% to 11.8% during the same period, both decreasing by more than 50%.

Kim Seo-yeon, lead researcher at NICE Credit Rating's Financial Evaluation Division, said, "Despite conservative risk management by credit card companies, the proportion of multiple borrowers has increased compared to the past, raising the possibility of delinquency transmission. The likelihood of recognizing losses due to failure to recover loans after delinquency has also greatly expanded compared to the past." She added, "Assuming the same delinquency rate increase shock, the loss magnitude for credit card companies is likely to be greater than during the 2008-2009 financial crisis."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}