Operating Profit Surprise-Shock Gap at 527%

Record High... Surpassing Even Financial Crisis Levels

Corporate Polarization Issue Ultimately Linked to Household Polarization

Urgent Need for Zombie Company Structural Reform, Yet No One Dares to Speak Up

[Asia Economy Reporter Kim Eunbyeol] Amid the impact of the novel coronavirus infection (COVID-19), which has led to declines in sales and operating profits for companies, the polarization among domestic listed companies has widened to an all-time high. While large domestic conglomerates entering the global market have posted better-than-expected results, continuing a 'surprise' streak, companies with weak financial structures have increasingly suffered severe 'earnings shocks,' resulting in this outcome.

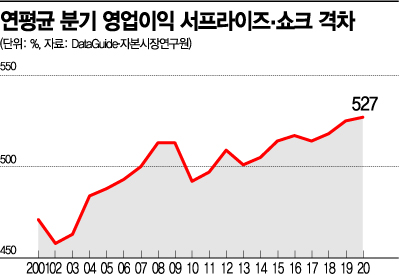

According to an analysis conducted on over 1,100 listed companies by Lee Sangho, a research fellow at the Korea Capital Market Institute, on the 18th, the gap between operating profit surprises and shocks among domestic listed companies this year (annualized basis for Q2) reached 527%. This represents a significant widening of the gap between the average surprise magnitude (269%) and shock magnitude (-258%) compared to market expectations. Generally, a performance exceeding expectations by more than 20% is referred to as an 'earnings surprise.'

The profitability gap among listed companies is the largest since quarterly earnings disclosures began in 2000, even surpassing the financial crisis periods of 2008 and 2009, which recorded gaps of 513% each. After the financial crisis, polarization among companies decreased, dropping to 492% in 2010, but recently, the gap has been steadily widening again.

The research fellow stated, "Well-performing companies are doing even better, while poorly performing companies are in a dire situation. There are various causes, but recently, the ultra-low interest rate environment has made it difficult to exit struggling companies, which seems to be widening the gap further."

Until now, government policies have focused primarily on household polarization, but corporate polarization can also act as an obstacle to economic growth. Corporate polarization affects the productivity and wages of employees within those companies, which can ultimately negatively impact the efficiency of income distribution.

This issue was also confirmed in the Bank of Korea's Q2 Corporate Business Survey. According to the Bank of Korea's announcement on the 15th, among listed manufacturing companies, the sales growth rate of the top 25% declined by 5 percentage points from 16.6% in Q1 to 11.6% in Q2. During the same period, the sales growth rate of the bottom 25% dropped sharply by 13.4 percentage points from -14.3% to -27.7%. The operating profit margin of the top 25% increased from 8.4% to 9.7%, while that of the bottom 25% decreased from -3.9% to -4.6%. The impact of COVID-19 has thus widened the gap between top and bottom companies.

The 'rich get richer, poor get poorer' phenomenon is also evident across industries. According to the Korea Capital Market Institute, among the top 100 companies with operating profit surprises, the medical (27%) and IT (23%) sectors accounted for half. In Q2, the medical industry ranked first for the first time ever, buoyed by sales of masks and diagnostic kits.

A common feature of these industries is active research and development (R&D) investment relative to sales. Over the past five years, the R&D investment ratio relative to sales was 5.9% for IT and 4.9% for medical sectors. In contrast, companies excluding Samsung Electronics and SK Hynix have maintained an R&D ratio of only about 1%. The research fellow pointed out, "R&D investment is meaningful when it leads to profitability," adding, "Since the 2000s, companies with low profitability have fallen into a vicious cycle of low growth, low returns, and low activity." The Bank of Korea's announcement that the total asset turnover ratio of externally audited companies in Q2 hit a record low of 0.73 times supports the notion that companies are not utilizing their assets effectively.

Ultimately, companies that have failed to cover even interest expenses with operating profits for more than three years?so-called zombie companies?should be filtered out of the market through a selection process, and promising companies should be chosen for support. The problem is that no one finds it easy to advocate structural reform. A Bank of Korea official said, "There is consensus on the need for restructuring zombie companies," but added, "Since the COVID-19 shock is considered 'temporary,' the biggest challenge is establishing criteria to distinguish between normal companies and those to be exited."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}