Prospects for Managing Non-Living Expense Credit Loans for High-Income Earners

Bank Sector Moves to Reduce Preferential Interest Rates

Concerns Over Potential Disruptions in Financial Supply to Small Business Owners

[Asia Economy Reporter Kim Hyo-jin] As the management of rapidly increasing unsecured loans has become a hot topic in the financial sector, financial authorities are expected to introduce a 'pinpoint regulation' plan as early as next week to curb non-living expense loans for high-income earners. This aims to block high-income and high-credit individuals from raising large sums through unsecured loans for investments in real estate and the stock market following tightened regulations on mortgage loans.

The problem is that if unsecured loans are tightened too much, it could lead to side effects such as drying up the funding sources for small business owners and SMEs hit hard by COVID-19. Banks are also increasingly concerned. While discussing measures such as reducing preferential interest rate margins or lowering unsecured loan limits in response to regulatory pressure, they are burdened by the possibility that stable profit generation could be hindered.

◆Managing loans starting with high-income, high-credit borrowers = Currently, unsecured loans at commercial banks are generally made within 100-150% of annual income. However, special professions including doctors and lawyers can obtain loans exceeding 200% of their annual income without much difficulty. For example, if the annual salary is 150 million KRW, one can raise more than 300 million KRW through unsecured loans for stock investments.

At one commercial bank (A Bank), the scale of medical staff loans has exceeded 100 billion KRW consecutively for the past three months. Compared to the same period last year, it increased by about 20%. Accordingly, there is a strong expectation that loan limits for these groups will be lowered and various preferential interest rate benefits will be reduced. Some even mention specific criteria such as 'unsecured loan regulations for earners with annual income over 200 million KRW.'

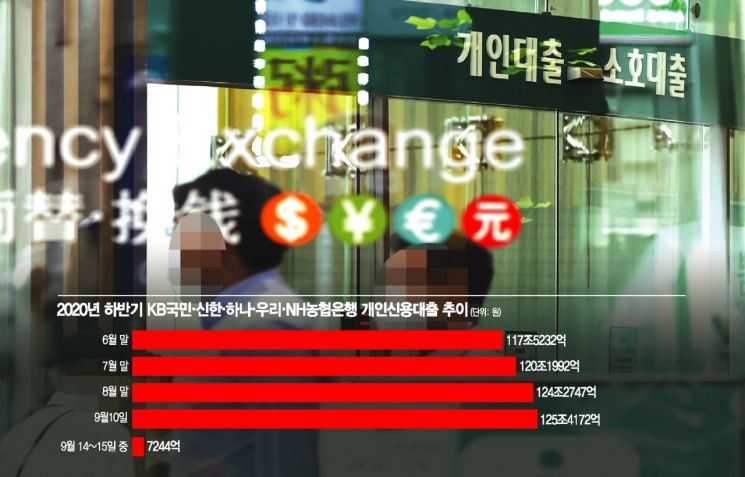

What financial authorities are watching is the fact that bank unsecured loans are supporting real estate panic buying?where people 'pull together every last bit' to buy homes?and 'debt investing' where people borrow to invest in stocks. At the end of last month, the balance of unsecured loans at the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?increased by 4.0705 trillion KRW (3.38%) from the previous month to 124.2747 trillion KRW, marking the largest monthly increase ever recorded.

Even this month, unsecured loans increased by 1.1425 trillion KRW in just ten days until the 10th. As loan regulation movements began, many rushed to secure loans before it was too late, resulting in a 724.4 billion KRW increase in unsecured loans at the five banks over just two days, the 14th and 15th.

A financial authority official said, "It is impossible to perfectly quantify how much of the total loans were used for 'pulling together every last bit' and 'debt investing,'" but added, "We judge that the increase in total loans is driven by high-income earners taking out non-living expense loans worth billions of KRW." He also emphasized, "We must not shrink the role of providing funds to small business owners and SMEs in response to COVID-19."

Concerns over weakening virtuous cycle structure through profitability enhancement

◆Banks sighing cautiously = In response to these movements, banks are reorganizing their systems by strengthening overall unsecured loan screening standards and preferential interest rate conditions. B Bank lowered the preferential interest rate margin on unsecured loans by 0.2 percentage points earlier this month. C Bank plans to manage by deleting some items of interest rate benefits.

A C Bank official said, "If all conditions are met, preferential interest rates can be applied up to around 1%," and predicted, "The larger the loan amount, the greater the suppressive effect from adjusting preferential interest rates." Banks are preparing unsecured loan total volume management plans until the end of this year as requested by financial authorities. There are also expectations that 1%-level unsecured loan products currently available may disappear once bank management intensifies.

While banks empathize with the problem of the recent surge in unsecured loans, they are also concerned about side effects that artificial regulations might cause. A credit executive at D Bank said, "Loans to high-income earners can be considered high-quality transactions from the bank's perspective," and pointed out, "A kind of virtuous cycle is needed where increased profitability through these loans is used for living expense loans."

A bank official lamented, "Although no official regulation from financial authorities has been announced, verbal interventions regarding loan regulations have already been made, so banks have no choice but to manage unsecured loans cautiously." He also predicted, "If financial authorities push too hard, banks might strictly manage even living expense loans for the lower and middle classes to produce results in total loan volume management."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}