Potential Capabilities Boost Investment Decision

Estimated Corporate Value Around 700 Billion Won

Plans to Propose Improvements in Business Structure

"Additional Stake Acquisition? Current Holdings Are Sufficient"

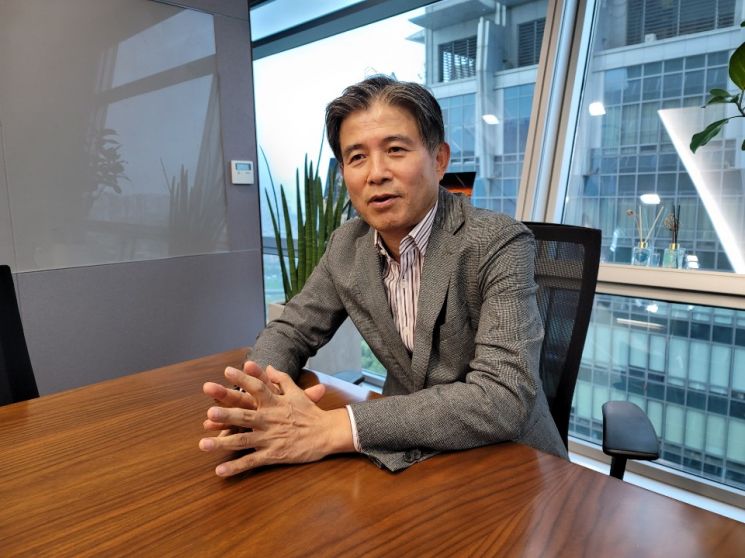

[Asia Economy Reporters Jeongsoo Lim, Hyowon Jang] "A hostile takeover (M&A) of KMH Group is neither possible nor something we intend to pursue. This is an investment to form a partnership with KMH, an undervalued blue-chip company, to enhance corporate value."

Hyun Sang-soon, CEO of Keystone Private Equity (PE), a private equity fund (PEF) operator that became the second-largest shareholder of KMH, stated this in an interview with Asia Economy on the 7th. Previously, on the 31st of last month, Keystone PE acquired a 25.06% stake in KMH for about 50 billion KRW. Keystone PE, which operates a management-participation type PEF, emphasized that the reason for investing in KMH is their high regard for KMH's potential.

CEO Hyun asserted, "Even conservatively estimating KMH's corporate value, it should be around 700 billion KRW." Based on the first half's trend, KMH's EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is expected to be around 90 billion KRW this year, and applying an EV/EBITDA multiple of 10 times results in a corporate value estimated at 900 billion KRW. He also estimated, "The net asset value is 500 billion KRW, and considering the investment status and other corporate details, even a conservative estimate would be 700 billion KRW."

Regarding the reason for KMH's undervaluation in the stock market despite its high intrinsic corporate value, he analyzed it as due to a complex business structure and governance. CEO Hyun said, "Although KMH's corporate value has grown sharply over the past five years, the average market capitalization in the stock market is around 150 billion KRW," diagnosing that "a lack of supplementary measures for structural improvements to enhance value has led to a long-term undervaluation phenomenon becoming entrenched and chronic." He explained that because of the significant potential for stock price appreciation, KMH was evaluated as a hidden blue-chip value stock, leading to their investment.

He said, "Going forward, we plan to propose two major initiatives to increase KMH's value." The first is improving or reorganizing the business and governance structure. Keystone PE argued that KMH needs thematic divisions by business. As part of this, they proposed dividing KMH's approximately 30 subsidiaries into three sectors: Media Group, IT Group, and Real Estate Group. They also proposed playing the role of a financial investor (FI) necessary during the business structure efficiency process. Additionally, they pointed out the need to resolve some circular shareholdings.

Regarding suspicions of a hostile M&A raised by some quarters, he categorically denied both the possibility and any such plans. CEO Hyun said, "KMH's largest shareholder and friendly shareholders hold about 40%, so a hostile M&A with a 25% stake is practically impossible," adding, "If there had been an intention for M&A, they would not have consolidated 25% of shares into one fund but rather held less than 5% shares separately without disclosure and then used an aggressive strategy."

He also drew a line on additional share acquisition. CEO Hyun said, "Since this is a project fund, an increase is possible, but with our 25% stake, including the major shareholder's shares, the total reaches 60%, so we believe we have secured sufficient shares." He reiterated that Keystone PE wants to act as a white knight for KMH's largest shareholder.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}