Partial Amendment to the Local Tax Special Cases Restriction Act

50% Acquisition Tax Reduction for Houses Under 300 Million KRW, 100% Exemption for Those Under 150 Million KRW

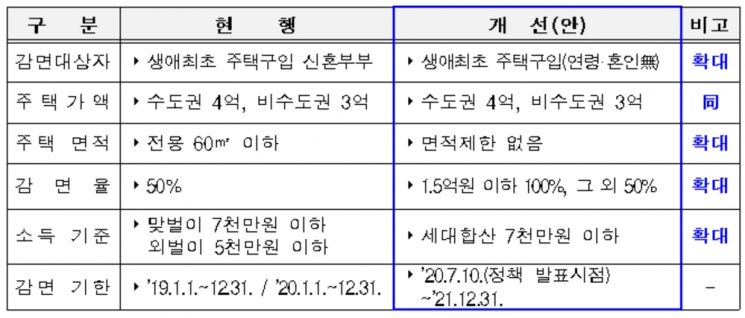

[Asia Economy Reporter Jo In-kyung] When purchasing a home for the first time in their life, not only newlyweds but also unmarried individuals or middle-aged and older couples can receive acquisition tax reduction benefits.

The Ministry of the Interior and Safety announced that the "Partial Amendment to the Local Tax Special Cases Act" containing this content passed the Cabinet meeting on the morning of the 11th.

Previously, only newlyweds who met certain income and other requirements and bought a home for the first time were exempted from 50% of the acquisition tax. Newlyweds were defined as couples within 5 years of marriage registration, so middle-aged and older couples with children or unmarried individuals were excluded from the benefits.

Following the "Housing Market Stabilization Supplementary Measures" announced on the 10th of last month, the government amended the law so that from the 12th, even those who are not newlyweds can receive acquisition tax reductions if they meet income requirements and other conditions.

Accordingly, for apartments and multi-family/row houses excluding officetels, applicants whose individual or combined annual income of the couple is 70 million KRW or less can receive the reduction benefit. Previously, if a single-income household earned more than 50 million KRW, they could not receive the reduction.

The housing area restriction, which was limited to 60㎡ or less, has also been removed. The purchase price of the home must still be 300 million KRW or less (400 million KRW or less in the metropolitan area), as before.

However, the amendment expanded the benefit by fully exempting acquisition tax for homes priced at 150 million KRW or less, instead of the previous uniform 50% reduction.

To receive the acquisition tax reduction, none of the household members registered in the resident registration must own a home. In the case of couples, even if the spouse is not registered as a household member on the resident registration, they are considered the same household.

The new criteria apply to homes acquired after the announcement of the Housing Market Stabilization Supplementary Measures on the 10th of last month. For those who purchased a home and paid acquisition tax between the 10th of last month and August 11th, a tax refund will be provided. The refund application period is within 60 days from the law’s enforcement date on the 12th.

Those who receive the acquisition tax reduction benefit must report their move-in within 90 days from the date of home acquisition and begin actual residence. If they purchase an additional home during this period or sell, gift, or lease the home before residing for at least 3 years, they may be subject to tax recovery.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}