83 Cases of Cooperative Sanctions This Year

More Than Last Year's Number of Sanctions

[Asia Economy Reporter Kim Min-young] While the National Credit Union Federation of Korea (NACUFOK) has achieved its long-cherished goal of expanding its business area, local credit unions are still being found to have operational shortcomings, such as incorrectly calculating loan amounts. As the scope of operations is expected to broaden as early as the end of this year, there are calls to further enhance expertise in internal credit screening and post-management.

According to the financial sector on the 10th, the number of disciplinary actions self-detected by credit unions from January to July this year was 83 cases, exceeding the total of 75 cases in 2018. At this rate, it is estimated that the number of disciplinary actions will surpass last year's 148 cases. During the same period, the number of sanctions imposed by the Financial Supervisory Service (FSS) was 5, the same as the total number of sanctions last year (5 cases).

Operational Shortcomings in Basic Tasks such as Loans and Deposits

Incidents that should not occur in mutual finance sectors, which perform banking-like tasks such as loans and deposits, have frequently happened. Recently, a credit union in Daegu was issued a 'formal warning' by the FSS after it was found to have exceeded the loan limit to a single borrower.

According to the FSS, mutual finance institutions like credit unions must lend to a single borrower within the larger of 20% of their own capital or 1% of total assets. However, this credit union lent KRW 17.01 billion (104 cases) to 8 borrowers over 14 years from 2005 to 2018, exceeding the single borrower loan limit (KRW 500 million) by up to KRW 2.219 billion.

This credit union also failed to strictly manage loans to its employees. According to the Credit Union Act, credit unions are prohibited from granting loans secured by real estate other than housing owned by their executives and employees. Nevertheless, in November last year and July 2018, two individuals including Executive Director A of this credit union were found to have taken out loans of KRW 50 million secured by land owned by their spouses and mothers. Executive Director A received an improvement order, and the employee was severely disciplined with a three-month suspension.

A financial sector official pointed out, “If credit unions have earned the right to expand their loan areas through effort, they must establish loan and deposit systems that match this right. Without thorough retraining of underperforming credit unions, financial accidents could occur at any time.”

Expansion of Loan-Eligible Areas

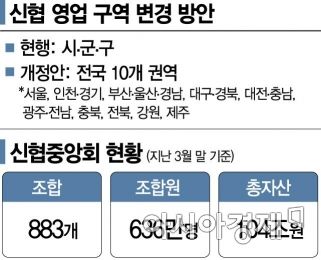

The Financial Services Commission has decided to divide the current 226 city, county, and district units where credit unions can lend into 10 regions: Seoul; Incheon-Gyeonggi; Busan-Ulsan-Gyeongnam; Daegu-Gyeongbuk; Daejeon-Sejong-Chungnam; Gwangju-Jeonnam, among others, through amendments to the Enforcement Decree of the Credit Union Act and the Mutual Finance Business Supervision Regulations. It also relaxed regulations by considering loans within these regions as member loans. This is expected to be implemented around the end of this year.

Additionally, the requirements for expanding joint bonds will be eased. Joint bonds refer to the business area units that determine the establishment of a credit union and its members. The requirement of “asset size of KRW 100 billion or more” has been abolished, allowing small and medium-sized credit unions with excellent financial soundness and performance in microfinance to expand joint bonds to adjacent single city, county, or district units. Furthermore, regardless of the location of the main office, credit unions can expand joint bonds to some towns and townships adjacent to the city, county, or district where the credit union belongs.

Credit unions have formed a Joint Bond Task Force (TF) to improve loan and deposit systems. A credit union official said, “Urban hollowing-out areas, rural credit unions, and small credit unions can expand their activities to broader regions, enabling continuous credit union services even in underserved areas.” As of the end of March, there are 883 credit unions with about 6.36 million members. Total assets have also reached KRW 104 trillion.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}