3Q NIM Expected to Drop Up to 5bp

Actual Decline Likely Limited to 2-3bp

Soaring Loan Growth Rate Slows

COVID Loan Maturity Extensions, etc.

Downside Risks Remain for 2H

[Asia Economy Reporter Kangwook Cho] As the novel coronavirus disease (COVID-19) prolongs, concerns are growing over the decline in earnings and deterioration in asset quality of commercial banks in the second half of the year due to worsening profitability and increasing non-performing loans. On the other hand, some predict that the third quarter may mark the bottom, and recovery could begin in the fourth quarter. This is based on the analysis that the sharply rising loan growth rate curve in the first half of the year is flattening and low-cost deposits are increasing, which could lead to a recovery in the core profit source, net interest margin (NIM), after the third quarter.

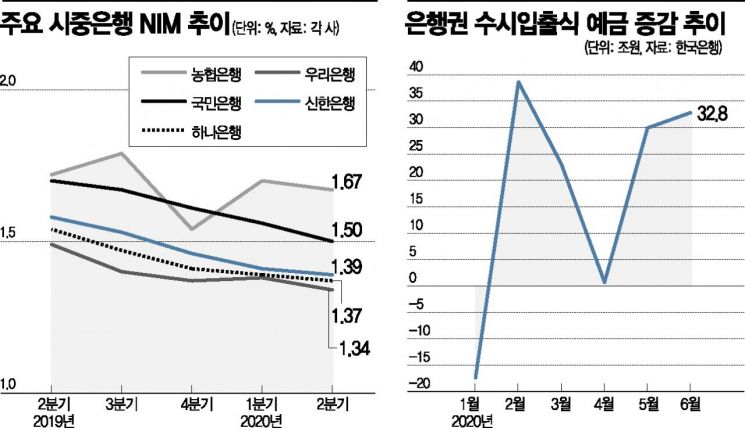

According to the financial sector on the 10th, the NIM of commercial banks in July is estimated to have declined by only about 1 basis point compared to the previous month, maintaining a fairly favorable level. Initially, the financial sector expected the most significant negative impact of the Bank of Korea’s 50 basis point rate cut in March and 25 basis point cut in May to occur in the third quarter. Most forecasts predicted that the third quarter NIM would fall by up to 5 basis points. However, the current consensus leans toward a decline of only 2 to 3 basis points.

Choi Jungwook, a researcher at Hana Financial Investment, said, "The previous expectation was that NIM would further decline by 1 to 2 basis points in the fourth quarter and bottom out during that period. However, if the current trend continues and there are no additional rate cuts, NIM is likely to form a bottom in the third quarter."

This analysis is based on the fact that loan growth is slowing while the surge in low-cost deposits continues. Commercial banks have already met most of their annual loan growth targets in the first half of the year. KB Kookmin Bank, which projected a 5-6% annual loan growth rate in its first-quarter earnings announcement, saw a 6.77% increase in the first half. Shinhan Bank recorded 8.17% (targeting 5%), KEB Hana Bank 4.30% (3-4%), Woori Bank 4.61% (5%), and NH Nonghyup Bank 6.11% (5.2%). Accordingly, banks have begun selecting management sectors at the start of the second half and are sorting out corporate loans, while also raising thresholds for household loans by adjusting limits to manage risks from rapidly rising unsecured loans in the first half.

Strategies to reduce funding costs by expanding low-cost deposits such as demand deposits and short-term savings deposits are also ongoing. These deposits require relatively lower interest payments to customers compared to time deposits and other savings products. According to the Bank of Korea, the increase in demand deposits was 29.9 trillion won in May and 32.8 trillion won in June, showing a significant rise mainly from corporate and individual funds. In contrast, time deposits decreased by 3.3 trillion won in May and the decline widened to 9.8 trillion won in June.

Additionally, expectations that the burden of loan loss provisions will decrease in the second half contribute to the third-quarter bottom theory. The five major financial holding companies set aside a total of 2.6554 trillion won in provisions in the first half of this year, double the 1.3903 trillion won in the first half of last year. Notably, 1.8425 trillion won was provisioned in the second quarter alone, surpassing last year’s first-half total in just one quarter. This was a preemptive measure in response to the COVID-19 impact. As a result of these efforts, the international credit rating agency Moody’s recently decided not to downgrade the credit ratings of domestic banks. Moody’s analyzed that concerns over the banking sector have been largely offset by Korea’s fiscal and financial policies.

Moody’s forecasted, "As loan growth at Industrial Bank of Korea and regional banks normalizes from the second half of this year, economic capital adequacy will temporarily weaken but is expected to recover over the next two to three years."

However, despite this optimism, concerns about deterioration in the second half remain high. Recently, the government has leaned toward extending the maturity and interest repayment deferral measures related to so-called 'COVID loans,' raising fears that these could become future non-performing loan triggers. In fact, economic agents including corporations and self-employed individuals borrowed over 100 trillion won from banks during the five months from February to June this year. Consequently, there are warnings that without proper screening, a 'hot potato' situation could lead to a non-performing loan crisis similar to the 2003 'card crisis.'

A financial sector official said, "Currently, banks classify all loans with extended maturities and deferred interest repayments under government policy as normal loans without problems," adding, "The current improvement in indicators is likely an 'optical illusion,' and the real COVID-related debt crisis will begin in earnest from next year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}