Q1 Net Income of 5 Companies Up 3.7%

Installment Finance Assets Also on the Rise

[Asia Economy Reporter Ki Ha-young] Card companies are gearing up for fierce territorial competition in the auto installment finance market in the second half of this year. As profits have declined due to reductions in merchant fees, many are planning to expand their auto installment finance businesses, which have emerged as new growth opportunities.

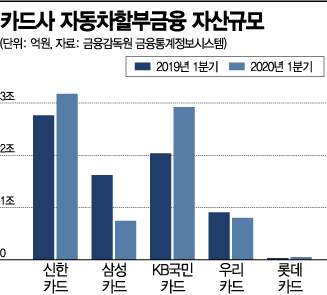

According to the Financial Supervisory Service's Financial Statistics Information System on the 7th, the net income from auto installment finance of five card companies (Shinhan, Samsung, KB Kookmin, Woori, and Lotte) operating in the first quarter of this year reached 64.9 billion KRW, a 3.7% increase compared to the previous year. Shinhan Card recorded 31 billion KRW, up 12.6% year-on-year, and KB Kookmin Card increased by 45.3% to 22.1 billion KRW.

Auto installment finance assets are also steadily increasing. During the same period, auto installment finance assets totaled 7.6997 trillion KRW, up 4.6% from the previous year. In particular, Lotte Card saw the largest asset growth, recording 51.4 billion KRW, a 55.8% increase year-on-year. The company explained that this was due to the leverage ratio improvement effect from issuing new capital securities in June last year and continuously enhancing product competitiveness such as 'Direct Auto.' KB Kookmin Card also recorded 2.9202 trillion KRW during this period, a sharp 43.5% increase compared to the same period last year. Shinhan Card, which holds the largest auto installment finance asset size, also achieved 3.1771 trillion KRW, a 15% increase from the previous year.

Card companies plan to expand their auto installment finance businesses in the second half of the year to compensate for deteriorating profitability caused by reduced merchant fees. In fact, in the first quarter, merchant fee income of seven specialized card companies (Shinhan, Samsung, KB Kookmin, Hyundai, Lotte, Woori, and Hana) was 990.4 billion KRW, down 13.1% year-on-year.

The easing of the leverage limit for card companies from 6 times to 8 times, under the Credit Specialized Financial Business Supervisory Regulations, which will take effect in October, is also expected to have an impact. With an increased leverage limit, card companies can expand their assets, allowing them to grow their auto installment finance assets and strengthen operations.

Shinhan Card and KB Kookmin Card are targeting the used car installment finance market. In March, Shinhan Card acquired long-term rental car assets worth 500 billion KRW from Hyundai Capital. In April, it signed an agreement to provide installment finance with 'Auto Meca Incheon An,' the largest used car sales complex in the Chungnam region. This marked the first partnership by a card company in the used car sales complex finance market, which has been dominated by large capital companies.

KB Kookmin Card is pursuing various projects related to used car installment finance. In January, KB Kookmin Card opened the 'Auto Finance Center,' a specialized used car installment finance branch in Gangseo-gu, Seoul, and is considering establishing Auto Finance Centers in other regions in the second half of the year. In the fourth quarter, it will also launch the 'Peer-to-Peer Used Car Transaction Card Safe Payment Service,' selected as an innovative financial service by the Financial Services Commission. This service provides credit card payment and vehicle information inquiry through a payment platform during peer-to-peer used car transactions. KB Kookmin Card will also strengthen its linkage with KB Capital to expand its auto installment business.

Lotte Card and Woori Card also plan to strengthen their operations in the second half of the year, focusing on their auto installment finance products such as 'Direct Auto' and 'Kajeongseok Auto.' Hana Card is preparing to enter the auto installment finance business, targeting the fourth quarter. An industry insider said, "The used car transaction market is about 3.7 million units, twice the size of the new car market, but the related financial market is still underdeveloped. As merchant fee income continues to decline, the auto installment finance market inevitably becomes a new growth opportunity for card companies."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}