Moody's Downgrades Domestic Banks' Ratings to 'Negative'... Securities Firms Under 'Review for Downgrade'

[Asia Economy Reporter Park Jihwan] As the novel coronavirus disease (COVID-19) crisis prolongs, warning signs have been triggered for the credit ratings of domestic financial companies.

If credit ratings deteriorate, the bond issuance interest rates in the financial sector rise, which directly leads to increased financial burdens. In particular, if a large-scale credit rating downgrade becomes a reality, there is a possibility that some financial companies may be completely blocked from capital inflows.

According to the credit rating industry on the 8th, recently, domestic and international credit rating agencies have been consecutively downgrading the credit rating outlooks for the domestic financial industry. On the 2nd, the international credit rating agency Moody's lowered the credit rating outlook for the domestic banking sector from 'stable' to 'negative.'

Last month, Moody's announced that it would consider downgrading the credit ratings of four regional banks in Korea. NICE Credit Rating also changed the credit rating outlooks for the financial sector to predominantly 'negative' in a report released on the 31st of last month.

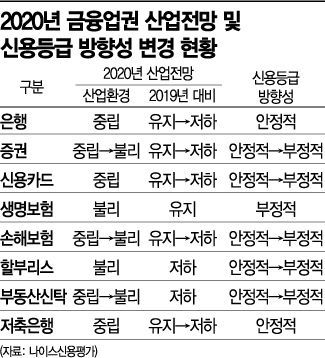

In last year's report, only life insurance among eight financial sectors was evaluated with a negative credit rating outlook, but this time six sectors were viewed negatively.

A downgrade in credit ratings for financial companies first raises their funding costs. During the 2008 global financial crisis, global credit rating agencies downgraded banks' credit rating outlooks, which led to an increase in bond issuance interest rates in the banking sector. The rise in funding costs reduces the net interest margin (NIM), which can directly hit banks' profitability.

Due to the impact of COVID-19, not only households but also corporate financial strength has weakened, raising concerns about the soundness of financial companies. This is because bank loans to industries directly affected by COVID-19, such as food service, lodging, transportation, and manufacturing, have significantly increased as part of government policies.

Seo Youngsoo, a researcher at Kiwoom Securities, said, "In 2008, banks' credit ratings were not actually downgraded, but the risk of loan defaults caused by the COVID-19 crisis started when banks' profit-generating capacity was already weakened, leading to additional concerns about deteriorating soundness."

The situation in the secondary financial sector is even more severe. In particular, credit card companies and capital companies are struggling to raise funds through specialized credit finance company bonds (여전채) as the capital market has frozen significantly due to the COVID-19 crisis. Although the government has announced that it will purchase some of these bonds through the Bond Market Stabilization Fund (채안펀드), the industry views the scale as far too insufficient.

The credit ratings of securities companies are also highly likely to decline. The day before, Moody's changed the credit rating outlooks of Mirae Asset Daewoo, NH Investment & Securities, Korea Investment & Securities, Samsung Securities, KB Securities, and Shinhan Investment Corp. from 'stable' to 'under review for downgrade.' Korea Ratings also adjusted the credit rating outlook for the securities industry from 'neutral' to 'negative' on the 26th of last month.

They commonly cited the increased volatility in the capital markets due to the spread of COVID-19 as the greatest risk factor. It is pointed out that the high volatility will simultaneously worsen securities companies' profitability, capital adequacy, funding, and liquidity management.

Anna Young, a researcher at Korea Ratings, evaluated, "As major stock indices plunge and the capital market contracts severely, the securities industry as a whole is facing liquidity burdens, increased volatility in asset values held, default risks, and profit declines due to reduced business activity."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}