Doosan Heavy Industries and Ssangyong Motor Face Liquidity Crisis Due to COVID-19

Increase in Non-Performing Loans Worsens Soundness...Concerns Over Paralysis of Policy Finance Functions

[Asia Economy Reporter Jo Gang-wook] As Ssangyong Motor faces a liquidity crisis following Doosan Heavy Industries due to the novel coronavirus disease (COVID-19) crisis, the concerns of policy banks such as the Korea Development Bank (KDB), Export-Import Bank of Korea (KEXIM), and Industrial Bank of Korea (IBK), which act as 'breakwaters,' are also growing. This is because, under government policy, the financial sector is already bearing nearly half of the total 100 trillion won in support, and additional sacrifices are inevitable to fulfill their role in corporate rehabilitation. While policy banks are committed to fully supporting corporate normalization, there are concerns that if large corporate insolvencies become widespread, it could worsen soundness and weaken restructuring capabilities.

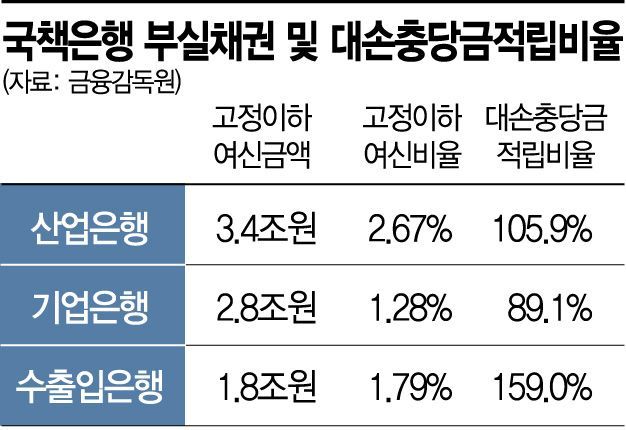

According to the Financial Supervisory Service and the financial sector on the 7th, as of the end of last year, the non-performing loan (NPL) ratio of KDB was 2.67%, ranking first among 19 domestic banks. Following that, another policy bank, KEXIM, had 1.79%, ranking second, and IBK had 1.28%, ranking fourth. Excluding K Bank (1.41%), which is virtually inactive, policy banks occupy the top three positions among the 19 domestic banks. The NPL ratio is a representative soundness indicator showing the proportion of non-performing loans (bad debts) in the total loan portfolio. Typically, policy banks handle corporate restructuring, which increases the likelihood of non-performing loans. Nevertheless, the average NPL ratio of the three policy banks reaches 1.91%, nearly five times higher than the average of commercial banks (0.41%).

Currently, policy banks serve as emergency rooms for companies. On the 27th of last month, KDB and KEXIM decided to provide 1 trillion won in emergency funds to Doosan Heavy Industries. Additionally, KDB plans to support Air Busan with up to 28 billion won through Asiana Airlines this month and will provide additional support to T'way Air. They also plan to jointly support 150 billion to 200 billion won this month for Jeju Air's acquisition of Eastar Jet.

The acquisition of Asiana Airlines by HDC Hyundai Development Company remains pending. It is reported that HDC Hyundai Development recently requested support from KDB and others regarding Asiana Airlines' borrowings. Last year, KDB acquired 500 billion won in perpetual bonds issued by KEXIM and Asiana Airlines and provided 800 billion won in credit lines and 300 billion won in standby letters of credit, totaling 1.6 trillion won in support.

Moreover, Ssangyong Motor is also reaching out for help due to the refusal of financial support from its major shareholder, India's Mahindra Group. Ssangyong Motor's borrowings exceed 400 billion won, including 190 billion won in loans from KDB. Notably, 70 billion won of KDB loans will mature in July this year.

The problem is that the capital capacity of policy banks like KDB is insufficient not only to absorb government measures but also to actively engage in corporate resuscitation. As of the end of last year, the common equity tier 1 capital ratios of KDB and IBK based on the Basel Committee on Banking Supervision (BIS) standards were 12.3% and 10.3%, respectively. Seo Young-soo, a researcher at Kiwoom Securities, pointed out, "Assuming a tolerable capital ratio of 9%, the risk-weighted assets that can be acquired are only 5 trillion won for KDB and 2.3 trillion won for IBK," adding, "If excessive policy support causes loss of market trust, the ability to raise funds and create credit could be significantly weakened."

Soundness management is also in an emergency. As of the end of last year, the total capital ratios of KDB, KEXIM, and IBK based on BIS standards were 13.97%, 14.48%, and 14.45%, respectively, lower than the domestic bank average of 15.25%. The simple tier 1 capital ratios were 11.28% for KDB, 10.37% for KEXIM, and 6.14% for IBK, decreasing by 0.27, 0.36, and 0.05 percentage points from the previous year, respectively. The loan loss reserve ratios increased for KDB and KEXIM but slightly decreased for IBK. Moody's, an international credit rating agency, recently began reviewing a downgrade of IBK's credit rating.

Concerns about future insolvencies are also growing within policy banks. An official from a policy bank said, "There is simultaneous pressure to prevent the collapse of the entire market and concerns about deteriorating soundness," adding, "As the scale of financial support to companies increases immediately, concerns about funding methods are also deepening."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}