Applications at bank branches from the 1st of next month

Support without damage proof for annual sales under 100 million KRW

1.5% ultra-low interest rate loans also offered by commercial banks

[Asia Economy Reporter Kim Hyo-jin] Small and medium-sized enterprises (SMEs) and small business owners who have suffered direct or indirect damage from the novel coronavirus infection (COVID-19) can apply for loan principal repayment maturity extension and interest repayment deferral starting from the 1st of next month. This applies to all financial sectors including banks, insurance companies, credit finance companies, savings banks, credit unions, NongHyup, Suhyup, forestry cooperatives, and Saemaeul Geumgo. Household loans such as mortgage loans are excluded. At the same time, ultra-low interest loans at 1.5% through commercial banks will also be supplied.

The Financial Services Commission announced on the 31st a financial support plan for SMEs and small business owners related to COVID-19 containing these details.

Businesses with annual sales of 100 million KRW or less will be considered as affected businesses and can receive support without separate proof. If annual sales exceed 100 million KRW, documents proving sales decline must be submitted. The financial authorities plan to broadly accept proof documents such as POS data, VAN company sales data, credit card company sales data, electronic tax invoices, and bankbook copies. If it is difficult to submit sales proof documents due to circumstances such as less than one year of business operation, a management difficulty confirmation letter prepared jointly by the financial sector can be submitted according to the prescribed form.

There must be no insolvency such as principal and interest arrears, capital erosion, or business closure to receive support. However, even if arrears occurred between January and March, if all arrears with financial companies are resolved as of the application date, the business is eligible for support. Businesses temporarily closed since January are also eligible unless due to other insolvencies such as capital erosion. Loans to SMEs, including individual business owners, received before March 31 of this year and with repayment deadlines by September 30 are eligible. Guaranteed loans and foreign currency loans are also included. For guaranteed loans, consent from the guarantee institution is required.

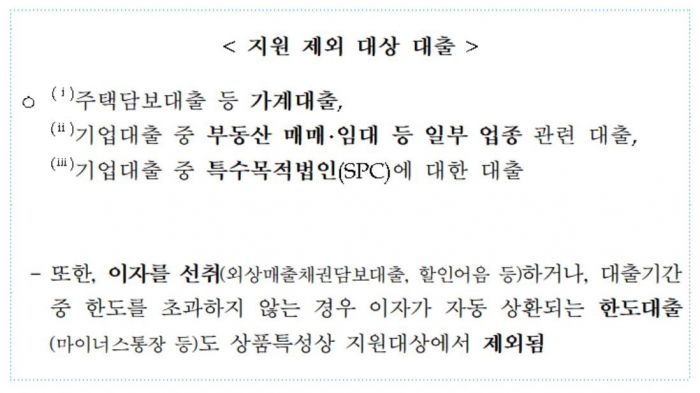

Household loans such as mortgage loans, loans related to certain industries like real estate sales and leasing among corporate loans, and loans to special purpose companies (SPCs) among corporate loans are not eligible for support. Loans where interest is collected in advance (such as accounts receivable secured loans, discounted bills) or revolving credit loans (such as overdraft accounts) where interest is automatically repaid without exceeding the limit during the loan period are also excluded from support.

Support will be provided by extending the maturity by at least six months from the application date and deferring interest repayment regardless of the repayment method, whether lump-sum or installment. Extension of the grace period for grace-type loan products is also included. For principal and interest installment loans, principal repayment deferral is included. Applications can be made by visiting the branch of the financial company with which the business has a transaction, and in some cases, applications can be made non-face-to-face via phone or fax.

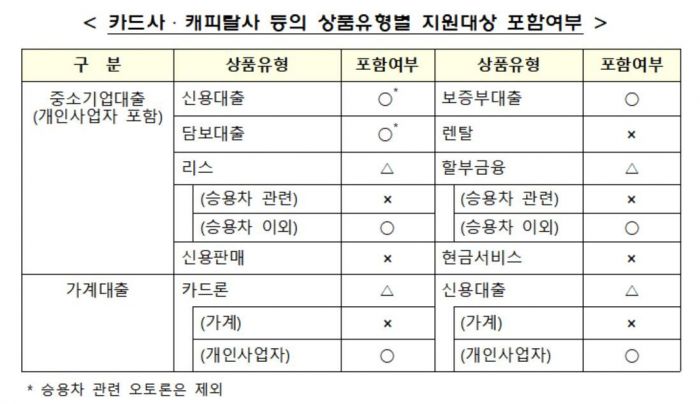

Among insurance policy loans, if the contract holder is an SME or individual business owner affected by COVID-19, they are included in the interest repayment deferral target. Card loans (including card loans from banks with multiple business lines), credit, secured, installment finance, and leases are also included in the deferral target, but credit sales, cash services, rental, and loans/leases/installment finance related to passenger cars are excluded.

Industries excluded from support include gambling and unhealthy amusement device manufacturing, general and dance entertainment bars, online game item brokerage, finance, real estate, golf course operation, and other gambling facility management and operation businesses, as designated by the Small Enterprise and Market Service's 'Small Business Policy Fund Loan Exclusion Industries.'

Meanwhile, small business owners affected by COVID-19 can also receive existing guaranteed loans with ultra-low interest rates (1.5%) from commercial banks starting from the 1st of next month. This is an interest subsidy loan where the government supports up to 80% of the difference from market interest rates. The remaining 20% is borne by the bank. The scale is 3.5 trillion KRW, and the target is highly creditworthy small business owners with annual sales of 500 million KRW or less. The criterion for 'high creditworthiness' corresponds to an internal credit rating by each bank equivalent to personal credit bureau (CB) grades 1 to 3. It is not possible to receive multiple supports such as the commercial banks' interest subsidy loans, IBK Industrial Bank of Korea's ultra-low interest loans, and the Small Enterprise and Market Service's management stabilization funds simultaneously.

Loans can be used up to 30 million KRW for a maximum of one year. Applications can be made at branches of 14 commercial banks, and KB Kookmin Bank and Shinhan Bank also accept applications through non-face-to-face channels. KB Kookmin Bank supports applications via internet banking, and Shinhan Bank via mobile banking. A financial authority official stated, "We expect loan execution to be possible within 3 to 5 business days after application." Applications can be submitted until the end of this year.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}