Foreigners' Selling Pressure and BOK Growth Rate Downgrade

Stock Market Expects 15 to 20 Trillion Won

[Asia Economy Reporter Minji Lee] As fears that the novel coronavirus infection (COVID-19) could escalate into a global pandemic continue to strike the domestic stock market day after day, foreign selling pressure has persisted for the fifth consecutive day. Despite the Bank of Korea's Monetary Policy Committee (MPC) lowering its annual economic growth forecast to 2.1%, it kept the base interest rate unchanged, leading the market to focus on the government's fiscal policy.

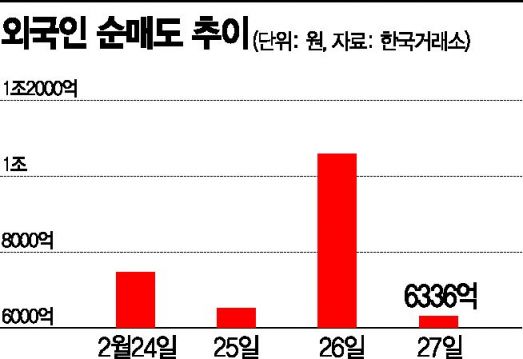

According to the Korea Exchange on the 28th, as of 10 a.m., foreigners net sold stocks worth 69.1 billion KRW in the KOSPI market. Individual investors sold stocks worth 80 billion KRW, while institutional investors alone purchased stocks worth 139 billion KRW. Foreigners continued their net selling streak for five consecutive trading days until that morning. During this period, foreigners net sold 2.8898 trillion KRW in the domestic stock market. The KOSPI 200 Volatility Index (V-KOSPI), which tends to rise when market volatility increases, surged about 40% this month.

As the COVID-19 situation prolongs, market attention is focused on the scale and timing of the government's supplementary budget (Chugyeong). This is based on the judgment that only the government's fiscal policy can quickly stabilize the financial market before the April MPC meeting, which will decide on interest rate cuts. Assuming that the effect of the supplementary budget can raise the economic growth rate by 0.2 percentage points per 10 trillion KRW, the market expects the supplementary budget size to be between 15 trillion and 20 trillion KRW. The supplementary budget proposal is expected to include expansion of COVID-19 response facilities such as the establishment of negative pressure rooms in local medical facilities, expansion of income deduction targets, and reductions in corporate taxes for the service industry.

Park Soyeon, a researcher at Korea Investment & Securities, explained, "The rationale for keeping the base interest rate unchanged is the judgment that policies selectively supporting vulnerable sectors are more effective than adjusting interest rates," adding, "Going forward, the stock market will be influenced by the size, funding, and timing of the supplementary budget."

If the supplementary budget is finalized, there is speculation that the KOSPI could rebound by the amount it previously fell. During the SARS (2003) and MERS (2015) outbreaks, the government allocated 3 trillion KRW and 11.6 trillion KRW respectively, which led to stock price increases. During the SARS outbreak, the KOSPI fell about 11% but rose 9% after the supplementary budget, and during MERS, it fell 9.8% and then rose 2.5%.

However, there are also opinions that the government's expected issuance of deficit bonds to enter the market could shock the financial market. Since the government announced plans to issue more than 60 trillion KRW in deficit bonds this year, the issuance scale could increase further with the addition of the supplementary budget.

Shin Dongsu, a researcher at Eugene Investment & Securities, pointed out, "During MERS, government tax revenues increased, so actual supplementary budget spending was about 8 trillion KRW less than planned, which reduced concerns about deficit bond issuance. However, this year, tax revenues have significantly decreased compared to 2018," adding, "If the issuance of 10-year government bonds increases, it could provide a factor for further widening spreads."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}