[Asia Economy Reporter Park Jihwan] Following Lime Asset Management's suspension of redemptions on funds worth about 1.6 trillion KRW, Alpenroute Asset Management is considering delaying redemptions on funds worth 180 billion KRW. Similarly, all 19 asset management companies operating funds through total return swap (TRS) contracts are exposed to the risk of redemption delays. Although financial authorities stated that this redemption delay differs from the Lime case, concerns have been raised that securities firms may rush to recover funds.

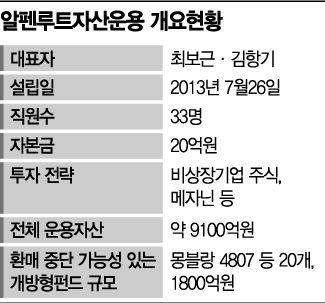

According to the financial investment industry on the 28th, Alpenroute Asset Management is reviewing the suspension of redemptions on 20 funds (total subscription amount 181.7 billion KRW) under TRS contracts with securities firms such as Montblanc4807. While the total redemption target is known to be 26 funds worth 230 billion KRW, considering 47.9 billion KRW invested by the company’s own funds and employees, the actual amount invested by individual investors and the securities firms’ loan scale is expected to be around 181.7 billion KRW.

Alpenroute Asset Management is a hedge fund manager investing in unlisted stocks. It has distinguished itself by investing mainly in promising domestic unlisted companies such as Big Hit Entertainment, the agency of BTS, open market Market Kurly, and smart farm startup Manna CEA.

An Alpenroute Asset Management official said, "We first decided to suspend redemptions on 1.95 billion KRW, for which the redemption date was confirmed today," adding, "The 179.7 billion KRW due for redemption in early February is not an immediate matter for suspension. We decided to monitor the situation until the end of this week."

The official explained, "We will provide a paper to beneficiaries explaining how asset recovery will be conducted and what the current investment portfolio is," adding, "However, since the fund invests in unlisted stocks, disclosure will be limited to investors only."

The reason Alpenroute is currently considering a large-scale suspension of redemptions is that securities firms with TRS contracts suddenly requested fund recovery, causing liquidity issues. It is known that Korea Investment & Securities and Mirae Asset Daewoo demanded termination of TRS contracts worth a total of 46 billion KRW over two days from the 22nd to the 23rd. This is interpreted as a risk management measure following liquidity problems in funds raised through TRS contracts concluded by Lime Asset Management with securities firms.

An Alpenroute official said, "We are continuously trying to postpone TRS contracts with securities firms, but it seems the securities firms have decided to exit this business," adding, "Although negotiations are ongoing, the situation is difficult."

This redemption suspension incident is reported to have been decisively influenced by TRS transactions with securities firms, similar to the Lime incident. Securities firms have been entering into TRS contracts with asset managers, which are stock-collateralized loans. TRS transactions are over-the-counter derivatives where the total return seller (securities firm) purchases underlying assets such as stocks and bonds, and all cash flows including profits and losses are transferred to the total return buyer (asset manager).

Securities firms provide loans secured by fund assets and receive fees from asset managers. On the other hand, asset managers can purchase assets worth about twice the investment amount by preparing only a certain level of margin. This is why asset managers could leverage funds and increase fund assets and returns or invest in illiquid assets while designing funds as open-ended structures through TRS contracts.

The problem lies ahead. If securities firms continue to terminate TRS contracts, the possibility of a repeat of Lime Asset Management’s fund redemption suspension cannot be ruled out. According to the securities industry, domestic securities firms currently have TRS contracts worth nearly 2 trillion KRW with 19 asset management companies. If securities firms continue to terminate TRS contracts, the possibility of additional redemption suspensions among hedge funds with similar structures cannot be excluded.

A financial investment industry official said, "Not only Lime Asset Management but also several asset managers have created mezzanine investments as open-ended funds," adding, "The current structure, where the scale of operations is greatly inflated through TRS contracts compared to actual assets held, causes the insolvency of the mother fund to significantly affect sub-funds."

A financial authority official said, "This redemption suspension is fundamentally different from Lime," adding, "The suspension appears to be a temporary occurrence in response to securities firms’ fund recovery rather than an internal company problem."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}