Expectations for Stock Market Recovery This Year Boost Equity Funds

Private Equity Fund Contraction Filled

Need to Resolve Rigidity in Sales Market

[Asia Economy Reporters O Ju-yeon, Gu Eun-mo] Last year, public funds lost popularity due to sluggish stock markets and the relative rise of private equity funds, but this year they are benefiting significantly from expectations of stock market recovery and the January New Year effect. The suspension of redemptions in Lime Asset Management funds and the maturity extension of German Heritage Derivative-Linked Securities (DLS) have dampened investor sentiment toward private equity funds, which is one reason why public funds are gaining more attention. In particular, since the end of last year, after the US-China Phase One agreement, global risk asset preference has strengthened, and domestically, expectations for semiconductor industry improvement and earnings rebound have grown, leading to increased demand for equity-type public funds.

◆Shrinking Private Equity Fund Investor Sentiment= "Will we be able to get our money back? If we could just confirm a principal loss, we could plan future measures, but with only maturity extensions, we are stuck and frustrated." An investor who was notified of a maturity extension after investing in last year's German Heritage DLS expressed this sentiment, saying, "I will no longer invest in private equity funds upon solicitation." Since the second half of last year, as incidents related to private equity funds have occurred one after another, investors' concerns about losses have increased, causing the previously surged private equity fund scale to shrink.

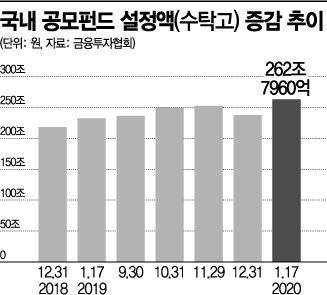

According to the Korea Securities Depository, the number of newly established public funds last year was 2,267, a 20.8% decrease from the previous year (2,863), while the number of private equity funds increased by 5.5% to 7,907 from 7,498 the previous year. The amount of new subscriptions also showed a 9.4% increase for public funds, whereas private equity funds rose by 23.5% to 128.6838 trillion KRW.

Recently, the atmosphere has changed considerably. According to the Korea Financial Investment Association, as of the 20th of this month, the number of private equity funds was 10,908, down by 232 from 11,140 on December 2 last year. The number reached an all-time high of 11,479 at the end of July last year but has since declined steadily: 11,458 at the end of August, 11,336 at the end of September, 11,177 at the end of October, and 11,140 at the end of November. Meanwhile, the number of public funds increased to 4,187 as of the 20th, up by 29 from 4,158 at the end of July last year.

◆Funds Flowing into Equity-Type Public Funds= Among public funds, the movement of funds toward equity-type funds rather than bond-type funds is noticeable. The net asset value of public bond-type funds decreased by 2.0632 trillion KRW (5.52%) from 37.4088 trillion KRW on December 2 last year to 35.3456 trillion KRW on the 20th of this month. In contrast, the net asset value of public equity-type funds increased by 9.6165 trillion KRW (14.66%) from 65.6033 trillion KRW to 75.2197 trillion KRW during the same period.

Within domestic equity funds, money is flowing into index funds linked to the KOSPI index. According to data compiled by financial information provider FnGuide, active equity funds saw an outflow of 30.76 billion KRW over the past month, while index equity funds experienced a net inflow of 6.17 billion KRW. Particularly, funds linked to the KOSPI 200 index attracted 45.84 billion KRW in net inflows.

By theme, funds with a high weighting in Samsung Electronics, which has repeatedly hit new highs amid expectations for the semiconductor industry, are popular. Since the beginning of the year, 24.02 billion KRW has flowed into Samsung Group funds, 3.01 billion KRW into IT funds, and 470 million KRW into healthcare funds.

◆"Public Fund Investors' Costs Must Be Reduced"= To sustain growth through their own capabilities rather than as a reflection of private equity fund weakness, it is pointed out that the rigidity of the sales market must be resolved. Currently, general public fund distributors must charge the same sales commission for the same fund and class. This structure prevents price competition among distributors and favors large distributors who have already secured a customer base.

Researcher Kwon Min-kyung of the Korea Capital Market Institute explained, "From the perspective of large financial companies with an established position, there is a strong incentive to strategically promote funds with high sales commissions, so asset management companies must set high sales commissions to expect their funds to be sold more by large financial companies." The rigidity of the sales market leads to high sales commissions, which in turn causes customers to turn away.

The cost of equity-type public funds sold domestically is high compared to major countries. According to global fund rating agency Morningstar, the total expense ratio of domestic equity-type public funds last year was 1.89%, higher than the US (0.59%), Australia (1.23%), Japan (1.31%), and the UK (1.57%).

To revitalize the public fund market, it is ultimately necessary to reduce investors' cost burdens to expand investment incentives. For this, an environment must be created where small and medium-sized financial companies can compete on equal footing with large financial companies in sales. Researcher Kwon emphasized, "It is necessary to encourage the entry of new businesses that provide simple sales services without separate advice or solicitation, or to activate sales channels that offer low-cost automated advice." She added, "In the long term, it is worth considering allowing sales commissions to be autonomously adjusted by sales companies by fund and class rather than being standardized, thereby inducing price competition among distributors."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}