Auto Insurance Loss Ratios Remain Elevated

Premium Hikes and the "8-Week Rule" Expected to Help

Insurers Seek Their Own Solutions via Channel Strategy and AI

The loss ratio for auto insurance has continued to exceed the break-even point. While the insurance industry is hoping to normalize profits through premium hikes and improvements to the system for minor-injury patients, companies are also reorganizing their sales channel strategies and introducing artificial intelligence (AI) to defend profitability.

According to the insurance industry on February 26, Lotte Non-Life Insurance plans to raise auto insurance premiums by 1.4% starting March 1. Earlier, Samsung Fire & Marine Insurance, which holds the No. 1 market share in auto insurance, raised its premiums by 1.4% on February 11. This was followed by DB Insurance, Hyundai Marine & Fire Insurance, KB Insurance, and Meritz Fire & Marine Insurance, which each implemented increases in the 1.3% to 1.4% range.

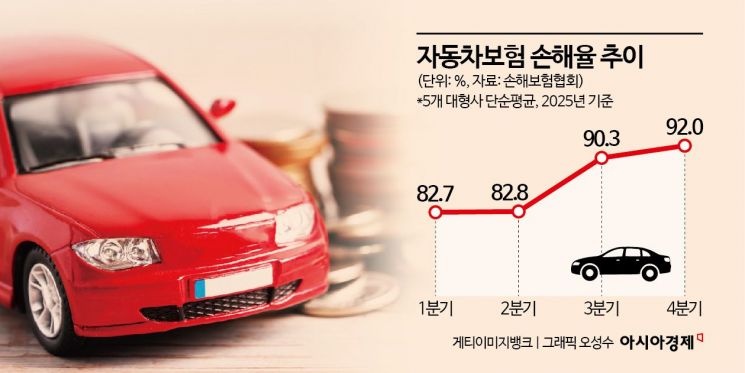

Industry observers say that these premium hikes by non-life insurers are an unavoidable step in response to a structurally worsening loss ratio. Last month, the auto insurance loss ratio of the top five non-life insurers averaged 88.5% (simple average), up 6.7 percentage points from a year earlier. In July, September, November, and December last year, the figure even exceeded 90%. The break-even point for the auto insurance loss ratio is generally considered to be 80%. Under the government’s policy stance of price stability and inclusive finance, premiums had been lowered for four consecutive years. During this period, higher repair costs, overtreatment of minor-injury patients, an increase in insurance fraud, and a rise in the number of accidents combined to drive a continued deterioration in the loss ratio.

Will Auto Insurance Enter a Profit Improvement Cycle This Year?

The industry expects that, alongside premium hikes, the so-called “8-week rule,” which strengthens medical review for minor-injury traffic accident patients as a measure to prevent insurance payout leakage, will help correct overtreatment practices and contribute to stabilizing the loss ratio. The “8-week rule” is scheduled to take effect in April. Ahead of full implementation, the Korea Insurance Development Institute is developing a system that analyzes typical hospitalization and outpatient days by gender, age group, and injury severity, and provides objective treatment guidelines. The aim is to make data on minor-injury patient treatment easier to search and utilize, thereby enhancing consistency in claims standards. In connection with this, Hyundai Marine & Fire Insurance said during a conference call on February 23, “Along with this month’s premium increase, we plan to focus our capabilities so that, through future improvements to the system for minor-injury treatment costs and efforts to curb increases in claims costs, we can enter an auto insurance profit improvement cycle starting this year.”

Hanwha General Insurance, which recently merged Carrot General Insurance, a digital insurer centered on auto insurance, has stated that it intends to reduce volatility in auto insurance profits not by relying on premium hikes, but by improving its channel strategy and achieving economies of scale. The company plans to advance a digital hybrid business model by combining Hanwha General Insurance’s face-to-face and telemarketing (TM) channels with Carrot General Insurance’s cyber marketing (CM) channel, and, based on this, expand Carrot General Insurance’s customers into long-term insurance products to diversify its revenue structure.

Samsung Fire & Marine Insurance is also working to improve the precision of claims cost management by expanding the scope of AI application across the entire auto insurance claims process. A Samsung Fire & Marine Insurance representative said, “The main direction is to expand the use of AI to support work that people have been performing in auto insurance,” adding, “This is expected to improve operational efficiency and have a positive impact on loss ratio management as well.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}