Household credit up 2.9% year-on-year at end-2025

Pace of increase has slowed since the third quarter

Mortgage loan growth down from 12.4 trillion won to 7.3 trillion won

Increase in other loans and sales credit by specialized credit

Household credit (debt) in Korea last year surged to nearly 1,979 trillion won, hitting a new all-time high. This was the largest increase since 2021, when it jumped by 133.4 trillion won (7.7%) during the period of the COVID-19 pandemic and soaring real estate prices. Although the government’s strong real estate measures have slowed the growth in mortgage loans since the third quarter, the pace of deceleration in overall household credit has weakened as securities firms’ margin loans and sales credit have expanded.

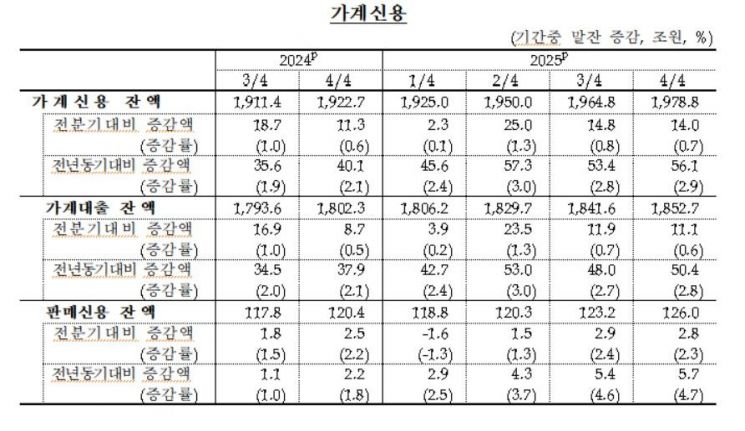

According to the provisional data on household credit for the fourth quarter of 2025 released by the Bank of Korea on the 20th, the balance of household credit at the end of the fourth quarter stood at 1,978.8 trillion won, up 14 trillion won from the previous quarter. Household credit refers to comprehensive household debt, which includes loans taken out by households from banks, insurance companies, savings and loan companies, and public financial institutions, plus pre-settlement card spending (sales credit).

Compared with the end-2024 household credit balance of 1,922.7 trillion won, this represents an increase of 2.9% (56.1 trillion won. However, the quarterly increase continued to narrow, following a decline to 14.8 trillion won in the third quarter of last year, marking two consecutive quarters of smaller gains.

Mortgage growth slows, shrinking household loan increase for two straight quarters...Unsecured loans turn to growth

Household credit in Korea turned back to growth in the second quarter of 2024 with an increase of 13.3 trillion won, and has since risen for seven consecutive quarters. Excluding card payments (sales credit), the balance of household loans in the fourth quarter of last year was 1,852.7 trillion won, up 11.1 trillion won from the previous quarter. The increase was smaller than in the second quarter of last year (23.5 trillion won) and the third quarter (11.9 trillion won).

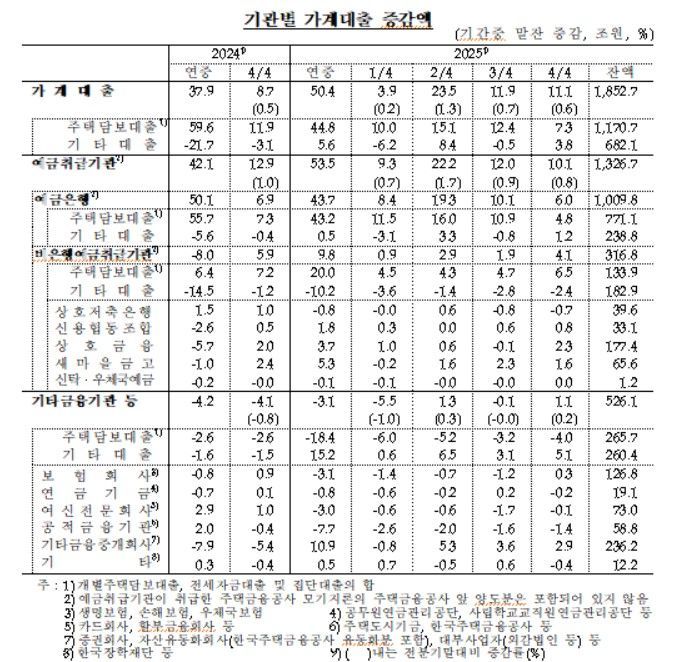

Within household loans, the balance of mortgage loans in the fourth quarter of last year was 1,170.7 trillion won, an increase of 7.3 trillion won from the previous quarter. This was a smaller rise than in the third quarter of last year, when mortgage loans grew by 12.4 trillion won. Lee Hyeyoung, head of the Financial Statistics Team in the Economic Statistics Department 1 at the Bank of Korea, explained that this was "due to measures to stabilize the housing market." On October 15 last year, the government announced a real estate package centered on designating additional speculative overheating zones and land transaction permit zones.

Other loans such as unsecured credit loans and overdraft accounts (minus accounts) turned to an increase, reaching 682.1 trillion won, up 3.8 trillion won from the third quarter of last year. Lee said, "Because the June 27 measures limited credit loan ceilings to within each borrower’s annual income, credit loans turned to a decline in the third quarter, and that base effect contributed to the turnaround to an increase in the fourth quarter."

By lending channel, the balance of household loans at deposit banks in the fourth quarter of last year was 1,009.8 trillion won, increasing by only 6 trillion won from the previous quarter. In contrast, household loans at non-bank depository institutions such as mutual finance cooperatives, mutual savings banks, and credit unions rose by 4.1 trillion won to 316.8 trillion won, with the pace of increase accelerating. While the growth of mortgage loans at deposit banks slowed in the fourth quarter of last year due to total loan volume controls, mortgage lending at non-bank depository institutions such as mutual finance cooperatives, mutual savings banks, and credit unions expanded.

Loans increase at other financial intermediaries...Hard to rule out possibility of money moving

The balance of household loans at other financial institutions such as securities firms, insurance companies, and asset-backed securities companies stood at 526.1 trillion won, up 1.1 trillion won from the third quarter of last year. Mortgage loans fell by 4 trillion won, but this was more than offset by a 5.1 trillion won increase in other loans at other financial intermediaries, including securities firms, asset-backed securities companies, and moneylenders.

The balance of sales credit (card payments) within household credit in the fourth quarter of last year was 126 trillion won, up 2.8 trillion won from the previous quarter. For sales companies such as department stores and automakers, the balance fell by 100 billion won to 1.2 trillion won, but at specialized credit finance companies such as capital companies, the balance of receivables expanded by 2.9 trillion won to 124.9 trillion won.

On the possibility that money may have moved from real estate to stocks, Lee said, "Since in the third quarter of last year credit loans, including card loans, were capped at within annual income, there is likely to be a base effect," but added, "Even though the increase in household loans at other intermediaries, which include securities companies, is slowing, they are still on an upward trend, so it is hard to rule out the possibility of money moving."

Bank of Korea: "Household debt ratio likely to fall this year...Uncertainty over household credit remains high"

The Bank of Korea pointed out that the ratio of household debt to nominal gross domestic product (GDP) at the end of last year may have declined. Lee said, "Household credit increased by 2.9%, and considering that the nominal GDP growth rate in the third quarter of last year appears to be in the high 3% range, the household debt ratio is also expected to have fallen last year compared with 2024."

Regarding the outlook for household credit this year, Lee said, "The government has been continuously strengthening its stance on managing household debt, for example by raising the lower bound of risk weights on bank mortgage loans earlier in the year, so household credit is unlikely to grow sharply," but added, "There are significant uncertainties, including increased housing transaction volumes, the resumption of financial institutions’ sales activities at the beginning of the year, and the expansion of securities firms’ margin lending."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}

{kind=link}