Up to 220 Companies Affected as Authorities Move to Weed Out Zombie Firms

Experts Weigh In on FSC's "Delisting Reform Plan"

"The direction is right. If anything, it is late rather than early."

"Zombie companies need to be cleaned up. But a 'price of 1,000 won' cannot be the criterion for insolvency."

After the financial authorities announced a "delisting reform plan" centered on eliminating penny stocks (low-priced stocks under 1,000 won), capital market experts agreed with the broad direction of "weeding out insolvent companies," but also voiced caution. They pointed out that whether this measure, which was modeled on the Nasdaq's penny stock system, will serve as an opportunity to restore market confidence, or whether it will merely increase the burden on growth companies by putting forward a "price yardstick" without structural remedies, will depend on how the detailed rules are designed. Some further argue that the real key is to fix the entry structure so that not just any company can go public in the first place.

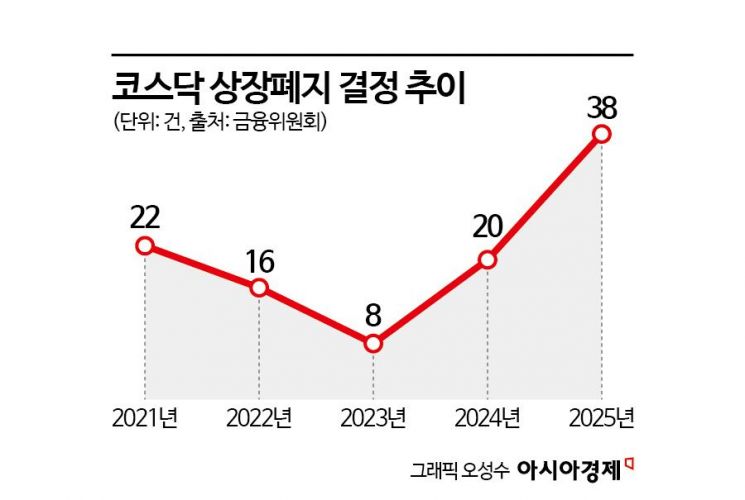

According to the financial investment industry on the 13th, experts generally gave a positive assessment to the reform plan on the grounds that, to restore confidence in the Korean stock market, especially the KOSDAQ market, it is inevitable to clean up marginal firms. Lee Namwoo, Chairman of the Korea Corporate Governance Forum, said, "Although it feels belated, strengthening delisting requirements is the right direction." Lee Sangho, Research Fellow at the Korea Capital Market Institute, likewise assessed, "There have been many KOSDAQ zombie companies and marginal firms vulnerable to stock price manipulation, so the intention to proactively clean them up is very desirable." The reform plan focuses on: operating a concentrated management period for KOSDAQ delistings to facilitate swift removal of insolvent companies; strengthening four major delisting requirements, including earlier application of the market capitalization standard, introduction of a penny stock requirement, tougher criteria for complete capital impairment, and stricter rules on disclosure violations; and streamlining procedures for abolishing KOSDAQ listing reviews. Once implemented, it is estimated that 100 to 220 companies in the KOSDAQ market alone will become subject to delisting this year.

Counterargument: "Price does not equal insolvency"... Structural differences from Nasdaq also cited

The most eye-catching element is the elimination of penny stocks. Due to their high price volatility, penny stocks have repeatedly become targets of speculative and manipulative forces, thereby exacerbating losses for retail investors. This is the backdrop to Vice Chairman Kwon Daeyoung of the Financial Services Commission remarking at a briefing the previous day that "we should have done (the removal of penny stocks) much earlier, but we are only now introducing international standards."

However, concerns are being raised over whether the 1,000 won price threshold is appropriate. Critics argue that one cannot simply equate "penny stocks = insolvent companies." Some warn that it could inadvertently shrink funding channels for undervalued companies, or deepen polarization in the market by reinforcing a large-cap-centric environment. A senior official in the securities industry said, "You have to look at it in combination with market capitalization, capital impairment, operating cash flow, and so on. Not all stocks under 1,000 won are the same kind of penny stock."

In particular, some question whether it is appropriate to apply a Nasdaq-style system directly to the KOSPI and KOSDAQ. On Nasdaq, institutional investors account for a high share and the over-the-counter market is well developed, so channels for trading and re-listing remain relatively open even after delisting. In contrast, on KOSDAQ, where penny stocks account for a relatively high proportion, retail investors make up around 80%, and alternative markets are not sufficiently active. At the listing stage as well, unlike Nasdaq, Korea has relatively low entry barriers due to mechanisms such as technology-special listing. This is why critics argue that if only a price-based standard is introduced without considering these structural differences, the intended effects will be difficult to achieve.

Chairman Lee said, "What is disappointing about this delisting plan is that corporate governance requirements and free-float share conditions are missing," adding, "Nasdaq requires, at the time of listing, a board of directors centered on independent directors, an audit committee, and high ethical standards. The 1,000 won requirement is subjective, and corporate governance and free-float conditions are far more important." Professor Lee Junseo of the Department of Business Administration at Dongguk University expressed agreement with the policy design that blocks delisting avoidance through stock splits in the process of eliminating penny stocks, but also said, "There is a clear difference between a company with a par value of 500 won and a share price of 1,000 won, and a company with a par value of 5,000 won and a share price of 1,000 won. It would be better to set standards by subdividing the ratio of share price to par value," he suggested.

Professor Ahn Donghyun of the Department of Economics at Seoul National University said, "Because there may be growth stocks that are sidelined in the process of eliminating penny stocks, it is also necessary, during substantive reviews, to grant a grace period," and recommended, "Rather than immediate delisting, companies should be given at least one chance." Nasdaq, which served as the model for KOSDAQ, also grants a grace period before delisting.

"Entry structure must also be fixed" Concerns over damage to retail investors

Some point to the listing entry structure as a more fundamental problem. Professor Ahn asked, "Isn't the core issue that we need to curb 'mass production' of listings? Because venture capital (VC) firms can take companies public on KOSDAQ too easily, problems inevitably arise." He criticized, "The problem is that companies are being listed indiscriminately, without distinguishing between good and bad." He went on, "Eighty percent of KOSDAQ investors are individuals, so ultimately it is retail investors who suffer," adding, "Urging faster and faster delistings ultimately amounts to shifting delisting costs onto individuals."

Regarding the raising of the market capitalization standard included in the delisting criteria, some experts noted the need for more granularity. Professor Ahn said, "I agree with the direction, but the (standard) is uniform," and continued, "For example, in the case of holding companies, their market capitalization can be relatively low. For such cases, it would be better to subdivide tiers and create mechanisms that first allow them to operate within a given tier, rather than immediately pushing them out." Kim Suyeon, Research Fellow at Gwangjang, voiced concern about potential side effects during implementation, saying, "The market requirements have suddenly become too stringent. I am not sure how feasible they are," and "For companies, the pressure will inevitably be intense."

On the separate issue of the stock exchange restructuring plan signaled by the financial authorities, expert opinions are somewhat divided. Professor Lee said, "It is right to separate the KOSDAQ market," explaining, "Under the current structure, it can only remain as a second division of KOSPI. Government initiatives such as national growth funds or venture capital ultimately relate to KOSDAQ, and if we want to grow our capital market, we should be revitalizing KOSDAQ." In contrast, Professor Ahn argued, "Rather than separating KOSDAQ, KOSPI and KOSDAQ should be merged," saying, "All companies should be subject to the same standards, and within KOSPI they should be classified into tiers such as Tier 1, Tier 2, Tier 3, and operated in a way that allows promotion between tiers."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}