Money moving into equities and a weaker won sap bond demand

Japan’s general election landslide for the LDP points to expansionary fiscal policy

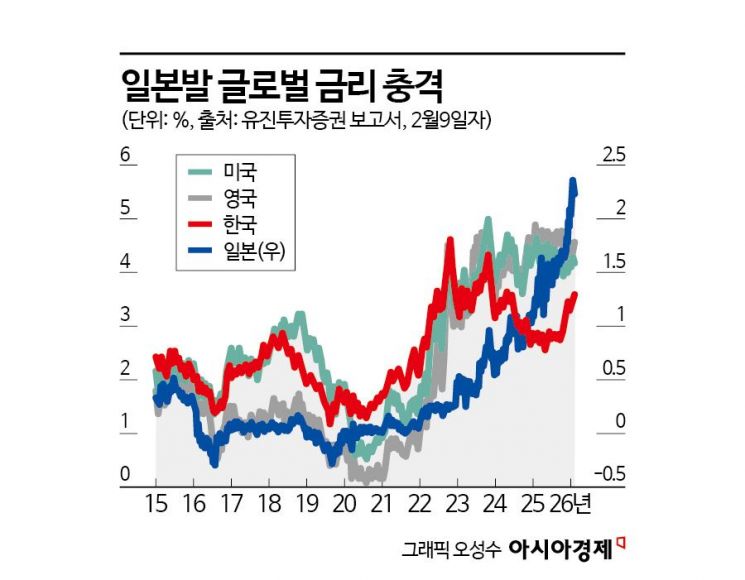

Rising Japanese government bond yields erode the appeal of Korean government bonds

Higher yield volati

As concerns grow that Japan's fiscal policy may shift toward an expansionary stance, risks in the Korean bond market are mounting further. Given the deadline for passing the budget bill, there is a view that related uncertainty could act as a destabilizing factor for the bond market through March. Moreover, the Korean bond market is already under significant pressure in terms of yield levels, with rates having risen the most among major countries so far this year, and conditions for supply-demand and the exchange rate have also deteriorated. Analysts warn that if rising Japanese government bond (JGB) yields push up Korean Treasury bond yields, it could also weigh on discussions over the so-called "cherry blossom supplementary budget."

Korean Bond Market Under Growing Pressure on Fears of Japan's Fiscal Shift

According to the financial investment industry on the 12th, the prevailing view in the market is that uncertainty surrounding Japan's fiscal policy is highly likely to remain a destabilizing factor for the bond market at least through March. Kim Jina, a researcher at Eugene Investment & Securities, said, "Yields have already priced in some of the risk during the general election, but instability could resurface when the budget bill is adjusted," adding, "The ultimate deadline for passing the budget bill is April 1. Until March, issues related to Japan's fiscal policy will remain a source of uncertainty in the bond market." Heoseongu, a researcher at Hana Securities, likewise assessed, "As fiscal concerns in Japan persist, the upward pressure on long-term yields remains in place."

Previously, on the 9th, Korean Treasury bond yields hit new highs due to the news of a landslide victory by Japan's Liberal Democratic Party and supply-demand pressures related to the auction schedule. Except for the one-year maturity, yields rose across the curve, marking new year-to-date highs. This means bond prices have fallen to new lows. The move reflects concerns that the stronger political footing of Japanese Prime Minister Sanae Takaichi, following the Liberal Democratic Party's landslide victory, will lead to more expansionary fiscal spending, pushing JGB yields higher and transmitting that impact directly to the Korean bond market.

Market participants are particularly focused on the fact that changes in Japan's fiscal policy now have a greater impact on the Korean bond market than in the past. Japan, one of the world's largest overseas bond investors, has long played the role of a lower bound for global interest rates through ultra-low rates and massive JGB purchases. If JGB yields rise, the reference point for the global yield structure as a whole shifts upward, and in this process, the relative appeal of Korean Treasuries, which already offer comparatively high yields, is bound to diminish rapidly.

The influence of Japan-related funds is also cited as a key market variable. Japanese investors such as life insurers and pension funds are among the major buyers of Korean Treasuries, and when Japanese yields rise, the added burden of currency-hedging costs can further weaken the incentive to invest in Korean bonds. This structure can translate directly into supply-demand pressure for Korean Treasuries. Kim noted, "Recently, the correlation between Japanese long-term yields and global yields has been very high," and evaluated, "At a time when risk-on sentiment toward risky assets is undermining bond investment appetite overall, the unusual rise in Japanese yields is a primary factor pushing up yields in major countries such as the United States, Australia, and Korea."

Already-High Yields... Overlapping Risks from Supply-Demand and FX

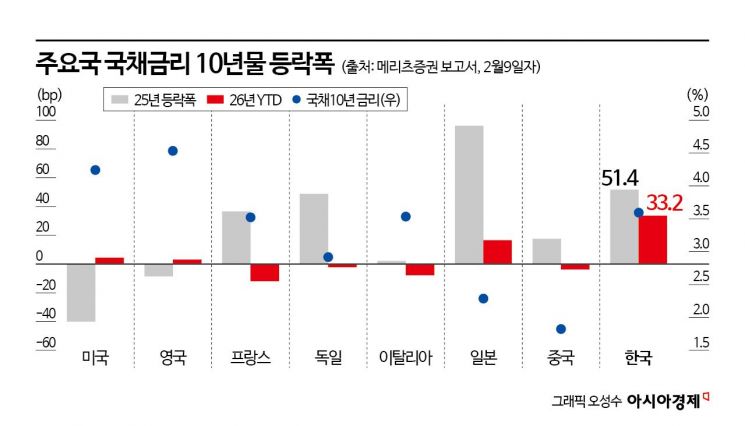

The problem is that the Korean bond market is already exposed to multiple risks at the same time. Since the beginning of the year, the 10-year Korean Treasury yield has surged more than 30bp (1bp = 0.01 percentage point) in less than 40 days, marking the steepest rise among major countries. This increase is larger than that of Japan or Australia, which have recently raised policy rates. Yoon Yeosam, a research fellow at Meritz Securities, diagnosed, "Current Korean market yields are at levels that already price in expectations for two rate hikes over the next year," and added, "If there are no actual hikes, roughly 50bp of the current yield level can be seen as a bubble."

With expectations for a policy rate cut already having faded and investor sentiment weakened, supply-demand and exchange-rate conditions are also cited as burdens. Cho Yonggu, a researcher at Shinyoung Securities, pointed out, "Korean Treasury yields have continued to rise while the stock index has been hitting record highs, yet they have not meaningfully retreated even when stocks have corrected," adding, "Risk-on sentiment in the financial market, combined with increased issuance, is acting as a negative factor for bond supply-demand."

There is still some expectation that foreign inflows will come in with Korea's inclusion in the World Government Bond Index (WGBI) in April, but the weak won is acting as a factor that constrains foreign investors' appetite for Korean Treasuries. Some in the securities industry even say that "for bonds to be attractive, it is important that the semiconductor cycle turns down," underscoring the lack of a clear buying catalyst. Cho predicted, "In the end, the market will likely continue to see pension funds, whose capacity to buy bonds has increased, playing a role in defending the upper bound of yields, while waiting for foreign WGBI-related inflows."

On top of this, external factors and domestic fiscal-policy variables are also adding to the pressure. There are concerns that if rising JGB yields push up the upper bound of Korean Treasury yields, discussions on formulating a supplementary budget could become more burdensome at a time when government borrowing costs are already elevated. Despite recent denials by the government, the possibility of a supplementary budget in the first half of the year continues to be raised. If the government's signal of fiscal expansion becomes clear while global yields are in an upward phase, there are fears that bond-market volatility could increase significantly. A bond-market participant said, "The recent market trend is difficult to view as just a short-term event," adding, "In particular, this is a time when we must closely watch how changes in Japanese policy affect Korean yield movements and the broader discussion on fiscal policy."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

!["The Woman Who Threw Herself into the Water Clutching a Stolen Dior Bag"...A Grotesque Success Story That Shakes the Korean Psyche [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}