Mortgage Loan Rates Near 4% Again in July

Unsecured Loan Rates See Largest Increase in 8 Months

Deposit Rates Continue to Decline for Tenth Consecutive Month

The interest rates on mortgage loans handled by banks have risen for two consecutive months, approaching the 4% annual mark. This increase reflects the additional interest margins raised by some banks in May and June. According to industry explanations, the additional interest margins raised by banks after the household loan regulations implemented on June 27 will affect the average mortgage loan rates with a lag of one to three months.

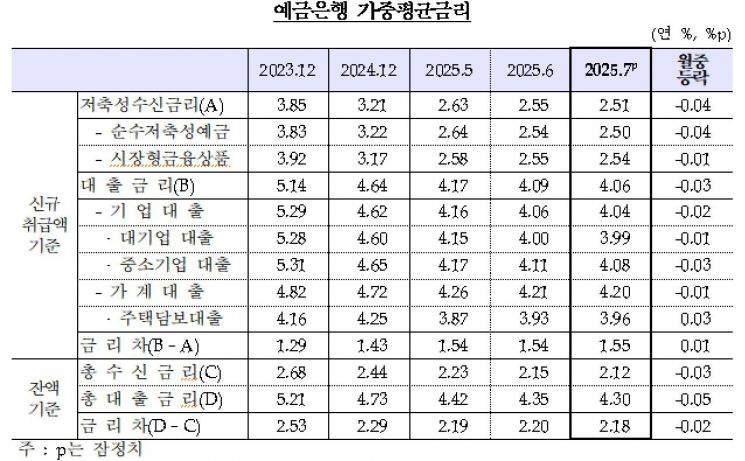

According to the Bank of Korea's announcement on July's weighted average interest rates at financial institutions released on the 27th, the mortgage loan rate at deposit banks (based on new loans) stood at 3.99% per annum last month, up 0.03 percentage points from the previous month.

The mortgage loan rate, which climbed to 4.27% in January this year, had declined for four consecutive months starting in February, but began rising again in June. Breaking it down, the fixed-rate mortgage loan rose by 0.03 percentage points to 3.95%, while the variable-rate mortgage loan fell by 0.06 percentage points to 4.05%. Kim Minsoo, head of the Financial Statistics Team 1 at the Economic Statistics Department, explained, "Although the benchmark five-year bank bond rate remained steady in July, the additional interest margins raised by some banks in May and June have affected the rates with a time lag."

The interest rate on jeonse (lump-sum deposit) loans rose by 0.04 percentage points from the previous month to 3.75% per annum, as some banks reduced their preferential rates in June. The general unsecured loan rate increased by 0.31 percentage points over the same period to 5.34% per annum. This is the largest increase in eight months since November 2014, when it also rose by 0.31 percentage points. However, Kim explained, "Rather than an actual increase in the rates borrowers pay, the rise is due to the June 27 measures that limited the maximum amount of unsecured loans to within annual income, which reduced the proportion of new loans taken out by high-credit borrowers who could have obtained loans at relatively lower rates."

Including these, the overall household loan rate fell by 0.01 percentage points from the previous month to 4.20% per annum, marking an eighth consecutive monthly decline. Although the rates for mortgage loans, jeonse loans, and general unsecured loans all increased, the rate for other guaranteed loans fell by 0.12 percentage points to 4.12% per annum, and the proportion of general unsecured loans, which tend to have higher rates, also decreased.

Corporate loan rates dropped by 0.02 percentage points to 4.04% per annum, continuing a two-month decline. As short-term market rates, such as 91-day certificates of deposit and short-term bank bonds, fell, rates for both large corporations and small and medium-sized enterprises (SMEs) declined. The rate for large corporations fell by 0.01 percentage points from the previous month to 3.99% per annum, while the rate for SMEs dropped by 0.03 percentage points to 4.08% per annum.

The interest rate on time and savings deposits (based on new deposits) declined by 0.04 percentage points from the previous month to 2.51% as time deposits and similar products fell. This marks a tenth consecutive monthly decline since October last year (3.37%). Specifically, the pure savings deposit rate, centered on time deposits, fell by 0.04 percentage points to 2.50% per annum. The rate for market-type financial products, mainly certificates of deposit, dropped by 0.01 percentage points to 2.54%.

The loan-deposit interest rate spread (based on new transactions) rose by 0.01 percentage points to 1.55 percentage points from the previous month. On a balance basis, the spread narrowed by 0.02 percentage points to 2.18 percentage points.

It is believed that the changes in bank interest rates following the June 27 measures were not yet reflected in July. Kim explained, "Although some banks slightly raised their additional interest margins after the measures, considering that it takes about one to three months for such changes to affect mortgage and jeonse loan rates, the impact of the June 27 measures on July rates was likely limited."

Regarding the future direction of mortgage loan rates, he said, "The benchmark five-year bank bond rate has fallen by 0.04 percentage points compared to last month's average, which is likely to exert downward pressure on mortgage loan rates in August." However, he added, "Since the additional interest margin increases before and after the measures may affect rates with a lag, we need to monitor the situation further." He also noted, "Based on our monitoring, only a few banks are raising their additional interest margins, and the scale of the increases is not as significant as in the second half of last year."

Meanwhile, the proportion of fixed-rate household loans rose by 2.9 percentage points from the previous month to 64.8%. In contrast, the proportion of fixed-rate mortgage loans fell by 1.8 percentage points to 88.8%. Kim explained, "A few months ago, some banks offered two-year jeonse loans classified as fixed-rate, which increased their scale and affected the proportion of household loans. The decline in the proportion of fixed-rate mortgage loans may be due to some borrowers choosing variable rates in anticipation of a base rate cut." However, he added, "With the implementation of the stress DSR and fixed rates being more advantageous in terms of loan limits, the proportion of variable rates is unlikely to rise rapidly."

Among non-bank financial institutions, the deposit interest rate for one-year time deposits fell across the board except for mutual savings banks. The lending rate (based on general loans) rose across the board except for mutual savings banks.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}