Shinhan Bank Relaunches Group Account After Three Years

Securing Low-Cost Deposits and Attracting New Customers

A group bank account is an account where multiple people collect money together for a specific activity, and it is gaining popularity because members can verify the process of pooling money together. Getty Images

A group bank account is an account where multiple people collect money together for a specific activity, and it is gaining popularity because members can verify the process of pooling money together. Getty Images

"Join the group account and receive a 10 million KRW group support fund."

Shinhan Bank, which recently launched the 'SOL Group Account Service,' is aggressively marketing the group account with its new model Cha Eun-woo at the forefront. It is unusual that the first advertisement after the model change is a product advertisement rather than a brand advertisement. Industry insiders see this as a sign that Shinhan Bank is focusing heavily on the group account. Previously, Shinhan Bank launched an application called 'Kim Chongmu' in 2011, similar to the current group account service, but discontinued it in June 2022 due to low usage. After three years, they reintroduced the service, belatedly entering the group account market.

Woori Bank also introduced a group account feature within its new banking app 'New One Banking' launched last November. iM Bank renewed its group account service starting January this year. KB Kookmin Bank and Hana Bank also currently offer group account services.

A group account is a bank account where multiple people pool money together for a specific activity, and members can verify the process of collecting funds, making it popular. KakaoBank was the first to introduce the group account, launching it in December 2018 as the industry's first. Starting with KakaoBank, the group account spread to internet-only banks and became a flagship product for them. As of the end of last year, KakaoBank's group account balance alone was 8.4 trillion KRW, accounting for about 26% of its demand deposit balance (31.7521 trillion KRW). During the same period, KakaoBank had 11.3 million group account customers.

A KakaoBank representative said, "At the initial launch, 70% of group account users were in their 20s and 30s, but as of the end of last year, users were evenly distributed across all age groups," adding, "The convenience of the group account has spread by word of mouth, especially increasing new customers in their 40s and 50s."

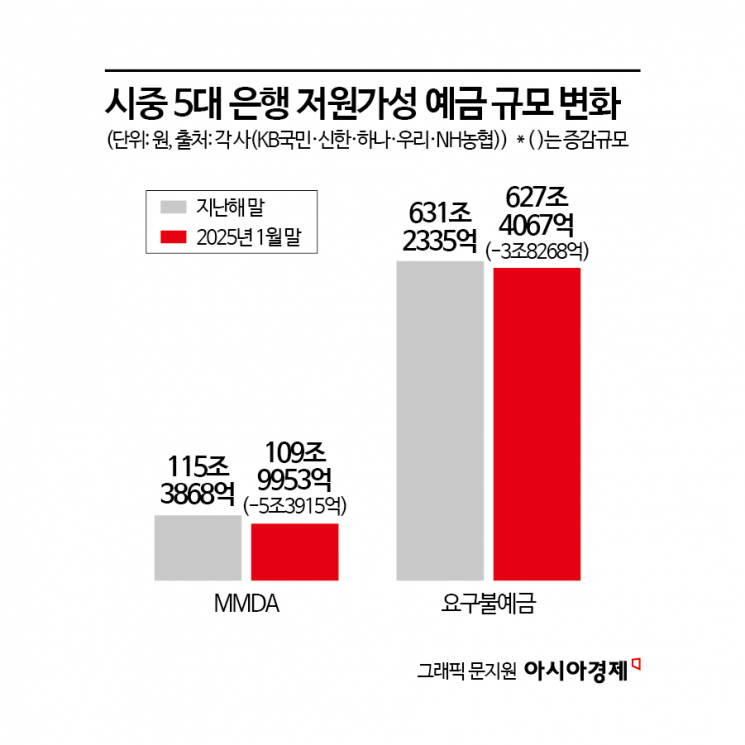

The reason commercial banks have entered the group account market, where internet banks have a stronghold, is to secure low-cost deposits. Recently, due to the Bank of Korea's base rate cuts and the low-interest-rate environment, low-cost deposits have significantly decreased. Group accounts operate as demand deposit accounts with a basic interest rate of only 0.1%, allowing banks to raise funds at rates lower than the 2% range deposit interest rates. As of the end of January, the demand deposits of the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup) totaled 627.4067 trillion KRW, down 3.8268 trillion KRW from the end of last year. The balance of money market deposit accounts (MMDA) also decreased by 5.3915 trillion KRW to 109.9953 trillion KRW during the same period.

The effect of attracting new customers through group accounts is also significant. A Shinhan Bank official said, "It is still early to judge the performance since the 'SOL Group Account' was recently launched, but some customers who are not main account holders are switching from other banks through the group account."

It is also known that savings banks are preparing to launch group account services.

An official from a commercial bank said, "It is a triple benefit for banks as they can raise deposits cheaply, attract new customers, and sometimes group account users open installment savings accounts afterward," adding, "In the current low-interest-rate environment, with significant capital outflows to coins and stocks, competition among banks for group accounts will intensify."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}