Display and home appliances profitability down

Mobile division also seems to have contracted

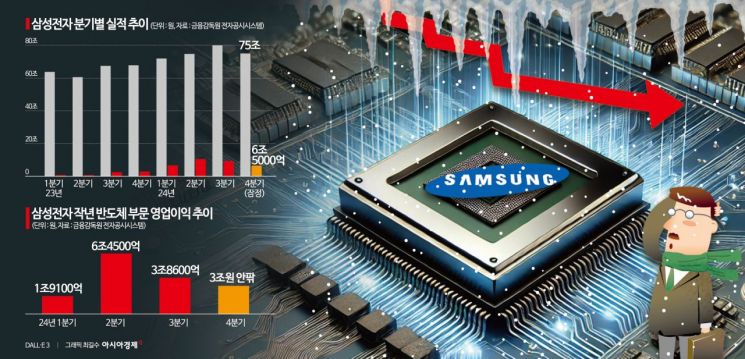

DS operating profit estimated around 3 trillion won

Less than half of Hynix

Decline in commodity DRAM prices causes sluggishness

Non-memory losses likely to widen as well

Samsung Electronics' lower-than-expected operating profit is largely due to the downturn in its core 'memory semiconductor' business. Additionally, the display and home appliance sectors saw profitability worsen compared to the previous quarter due to intensified competition, and the mobile division is also expected to have experienced negative growth.

Although Samsung Electronics did not disclose business segment results on the 8th, securities firms estimate the DS Division, which handles the semiconductor business, posted operating profit around 3 trillion KRW, slightly down from 3.86 trillion KRW in the previous quarter. This figure is less than half of SK Hynix's estimated operating profit of 8.0114 trillion KRW for the same period.

The semiconductor slump is attributed to delayed entry of HBM3E into North American customers and falling prices of legacy (general-purpose) DRAM. Samsung Electronics stated during its Q3 earnings conference call last year that "significant progress was made in completing a critical stage of the quality test (qual test) process for major customers of HBM3E, and sales expansion is expected in Q4," but no new updates have been reported.

In contrast, SK Hynix is thriving by effectively monopolizing HBM supply to Nvidia, which controls 90% of the AI accelerator market. HBM is a high-priced product costing 3 to 5 times more than general DRAM, and even small sales volumes bring substantial profitability.

Along with the slump in smartphone and PC demand, aggressive low-price supply from Chinese memory companies such as Changxin Memory Technologies (CXMT) is intensifying. The combination of shrinking demand and oversupply is further driving down memory prices. Chaemin Sook, a researcher at Korea Investment & Securities, said, "Considering Samsung Electronics' business structure with a relatively high proportion of general-purpose memory, profitability-focused management through supply adjustment is more important than anything else this year."

The DS Division's non-memory (foundry and system LSI) business is estimated to have an operating loss in the 2 trillion KRW range. Market evaluations indicate that the deficit has widened compared to the previous quarter.

Samsung Electronics explained regarding the DS Division's performance, "Despite weak demand for conventional products centered on PC and mobile, the memory business unit achieved its highest quarterly sales by expanding sales of high-capacity products in Q4." However, "performance declined due to increased R&D expenses for securing future technology leadership and initial ramp-up costs for expanding advanced process production capacity." It added, "The non-memory business saw reduced performance due to lower utilization rates and increased R&D expenses amid weak demand from major applications such as mobile."

Samsung Electronics' semiconductor performance slump is also compared with Taiwan's TSMC, the largest competitor in foundry. TSMC is expected to exceed market expectations in Q4 last year. Local media, citing sources, reported, "Demand for advanced 3nm and 5nm process products is strong," and "Q4 sales last year exceeded 860 billion TWD (approximately 38.1 trillion KRW), with January this year expected to record the highest sales ever."

Samsung Electronics has been out of sync with the semiconductor cycle since Q3 last year. The memory business unit turned profitable in Q1 last year, recording about 3 trillion KRW in operating profit, and increased to the 6 trillion KRW range in Q2, earning about 1 trillion KRW more per quarter than SK Hynix. However, the situation changed from Q3. While SK Hynix posted a record-high operating profit of about 7 trillion KRW due to increased HBM demand, Samsung Electronics' profit decreased to the 5 trillion KRW range.

There are also projections that SK Hynix will surpass Samsung Electronics' semiconductor business in annual operating profit for the first time, following Q3 last year. Securities firms' operating profit forecasts are in the 15 trillion KRW range for Samsung Electronics' DS Division and 23 trillion KRW range for SK Hynix. If this forecast materializes, SK Hynix will have an operating profit gap of over 8 trillion KRW compared to Samsung Electronics' DS Division. This is quite an unusual situation considering Samsung Electronics' long-standing technological expertise and production capacity in the memory semiconductor market.

Additionally, the MX Division, responsible for the mobile phone business, is also estimated to have seen operating profit decrease by about 200 billion KRW compared to Q3 last year.

Samsung Electronics' outlook for this year is also not favorable at present. This is because DRAM price weakness is expected to continue into Q1 this year. Market research firm TrendForce estimates that overall DRAM prices will fall by 8-13% during this period. Even including high value-added products like HBM, the decline is expected to narrow to 0-5%, making a price increase unlikely. Securities firms have also been lowering earnings forecasts and target stock prices one after another.

Kim Hyung-tae, a researcher at Shinhan Investment Corp., said, "Proving HBM performance and recovering foundry utilization rates to enhance technological capabilities are most important, but it is expected to be difficult in the short term." Park Yoo-ak, a researcher at Kiwoom Securities, predicted, "With normalization of DRAM distribution inventory and full-scale entry into the HBM3E business, earnings are expected to rebound from Q2 this year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}