US Concerns Over China Regulations Weigh on Korean Semiconductor Weakness

Front-End Set Demand Expected to Slow

Uncertainty Likely Resolved Only After Trump Takes Office

The sluggishness of the K-semiconductor sector continues. The reexamination of U.S. semiconductor law subsidies, export restrictions to China, and concerns over memory oversupply are worsening investor sentiment. Securities firms predict that the stock price recovery of major semiconductor companies will be difficult this year.

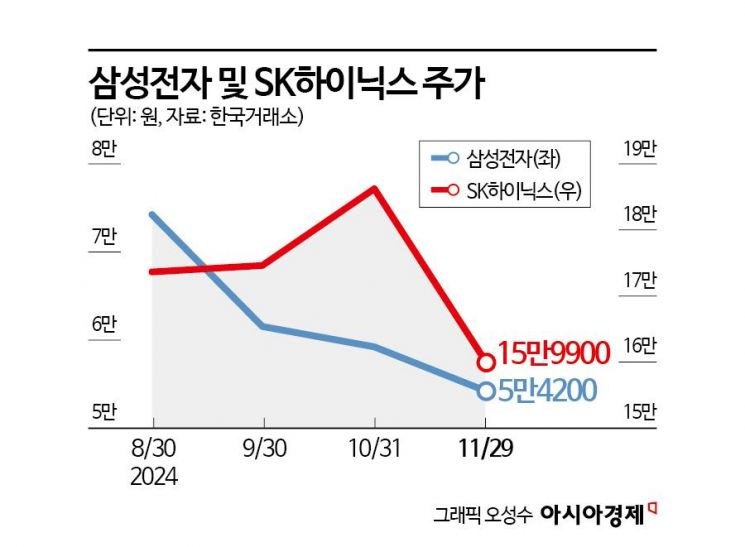

According to the Korea Exchange on the 2nd, Samsung Electronics closed at 54,200 KRW as of the previous trading day, down 7.03% over the past three trading days. During the same period, SK Hynix also fell 9.71%, showing a simultaneous weakness in the 'semiconductor top two.' On the 27th of last month (local time), major foreign media reported that the Biden administration in the U.S. is considering strengthening sanctions against China, and in this process, Changxin Memory Technologies (CXMT) is expected to be removed from the export restriction Entity List, raising concerns about memory oversupply. Additionally, the inclusion of restrictions on High Bandwidth Memory (HBM) also acted as a negative factor for domestic semiconductor stock prices.

In the securities industry, there is an analysis that a conservative approach to the semiconductor sector is necessary until the next administration of Donald Trump officially takes office. Chaemin-sook, a researcher at Korea Investment & Securities, said, "After Trump's election, semiconductor stocks have reflected exogenous variables more than corporate fundamentals, resulting in a downward trend," adding, "Specific policies need to be announced after the start of Trump's second term to help resolve uncertainties. Until then, stock prices may fluctuate whenever certain events occur."

Along with the negative factors from the U.S., the red light on demand in the upstream industries is also worsening investment sentiment. Until early this year, the semiconductor industry expected a recovery in the extremely sluggish PC and smartphone demand until last year, driven by AI laptops, but the absence of a 'killer product' that the general public would open their wallets for has led to an accumulation of semiconductor inventory. Lee Seung-woo, head of the research center at Eugene Investment & Securities, said, "The sell-out of on-device AI is sluggish, leading to inventory adjustments of key components related to PCs and smartphones, which is problematic," adding, "This impact is likely to continue until the first half of next year." He further diagnosed, "The World Semiconductor Trade Statistics (WSTS) DRAM sales value appears to have passed its peak and entered a downward trend. Concerns about the downturn transition of the DRAM cycle are increasing."

Researcher Song Myung-seop of iM Securities also pointed out the inventory accumulation issue. Song said, "Next year will be a period when semiconductor companies' inventories increase, contrary to the trend of the previous two years," explaining, "The current oversupply is caused by speculative buying based on the expectation that legacy (general-purpose) DRAM and NAND production will stagnate and prices will rise long-term due to strong AI investment expansion and increased HBM production share." He added, "However, in reality, demand in the IT sector excluding AI continues to be sluggish, and the production volume of AI servers by big tech companies exceeds actual needs. Due to economic slowdown, AI investment may also slow down in the second half of next year or the year after, which cannot be ruled out."

Due to U.S. policy uncertainties and a bleak industry outlook, the stock price recovery of major semiconductor companies is expected to be seen after the second quarter of next year. Park Yoo-ak, a researcher at Kiwoom Securities, said about Samsung Electronics, "As we approach the second quarter of next year, expectations such as Nvidia's entry into HBM3E will be reflected, strengthening the momentum for stock price increases." Regarding SK Hynix, he predicted, "The DRAM segment is expected to see a performance turnaround due to supply shortages in the second half of next year, but NAND is entering a down cycle, which may lead to an operating loss. The stock price is expected to show a box range movement."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}