September 5 Major Banks' Housing Loan Increase Halved from Previous Month

Holiday Impact Present... Concerns Over Early Year Supply Amount Reset

Recently, due to pressure from financial authorities to manage household loans, an autonomous restraint effect has appeared in the banking sector. However, concerns have been raised about whether this effect can continue even after the year-end, when the supply volume of household loans is 'reset.' Accordingly, attention is focused on the financial authorities' future measures.

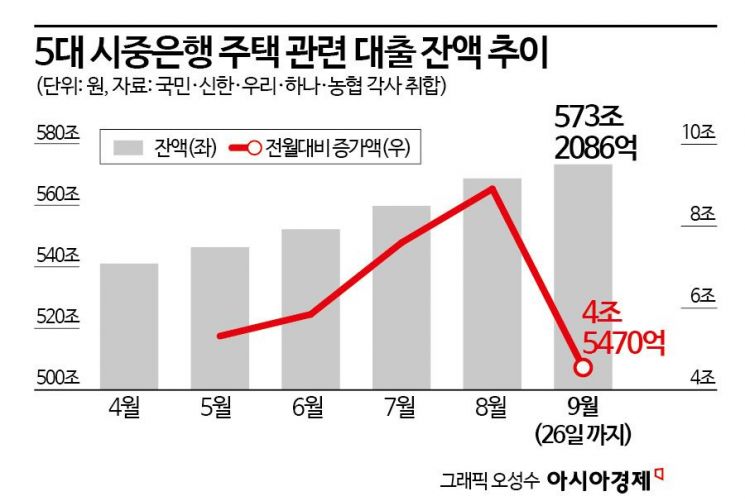

According to the banking sector on the 30th, as of the 26th, the outstanding balance of mortgage loans (including jeonse deposit loans) at the five major banks (Kookmin, Shinhan, Woori, Hana, and Nonghyup) increased by 4.547 trillion KRW this month. This figure is nearly half of the 8.9115 trillion KRW increase recorded in August alone. This declining trend is the result of banks strengthening their own lending standards in response to recent demands from financial authorities to curb household loans.

Banks have taken measures not only to raise interest rates but also to restrict eligibility for housing-related loans. In particular, Shinhan Bank, Woori Bank, and NH Nonghyup Bank have recently implemented stringent self-regulations, including suspending loans through loan solicitors. Loan solicitors refer to loan consultants and loan solicitation corporations that have signed outsourcing contracts with financial companies to perform loan solicitation tasks. Recently, as bank branches have decreased, loans through solicitors have increased as a means to enhance customer convenience, accounting for about half of the banking sector's mortgage loans.

However, it is unclear how long these effects will last. The decrease in loans this month was partly influenced by the Chuseok holiday. Since there are various public holidays in October as well, more time is needed to assess the actual loan reduction effect.

Moreover, since household debt management is currently left ostensibly to 'bank autonomy,' there is a possibility that loan doors may reopen next year if banks regain lending capacity. Professor Seok Byung-hoon of Ewha Womans University’s Department of Economics said, "Currently, the authorities have demanded comprehensive self-regulation, which has suppressed the increase in housing loans. However, suppressed demand still exists, so this can be seen as a kind of optical illusion."

Accordingly, attention is being paid to what regulations the financial authorities will establish while monitoring household debt and housing price trends. Before Chuseok, after a meeting with bank CEOs, Lee Bok-hyun, Governor of the Financial Supervisory Service, mentioned to reporters that it might be necessary to manage banks' funding schedules in detail, such as on a monthly basis. This suggests that the financial authorities may require a more detailed approach to banks' loan balance targets than the current annual plans to prevent a loan cliff near the year-end, as banks quickly exceed their annual targets like this time.

However, the Financial Supervisory Service currently confirms the annual household loan balance targets through management plans submitted by banks each year and intends to refrain from further intervention. A senior official at the Financial Supervisory Service stated, "There are no plans to receive monthly loan target amounts beyond the annual targets currently submitted through management plans," and regarding Governor Lee’s mention of 'monthly management,' clarified, "The intention is to receive plans on how to adjust since some banks have already exceeded this year's targets."

Additionally, interest is focused on whether the financial authorities will implement the early enforcement of the third stage of the stress Debt Service Ratio (DSR). The stress DSR is a system that adds an additional interest rate to the DSR regulation, which limits the principal and interest repayment amount to a certain percentage of annual income. Currently, the second stage is in effect. The higher the stage, the lower the maximum amount a borrower can borrow.

A financial sector official said, "More time is needed to determine whether the current decline in loans is a temporary phenomenon or the beginning of a long-term trend," adding, "It is expected that financial authorities will announce measures after observing the trend."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}