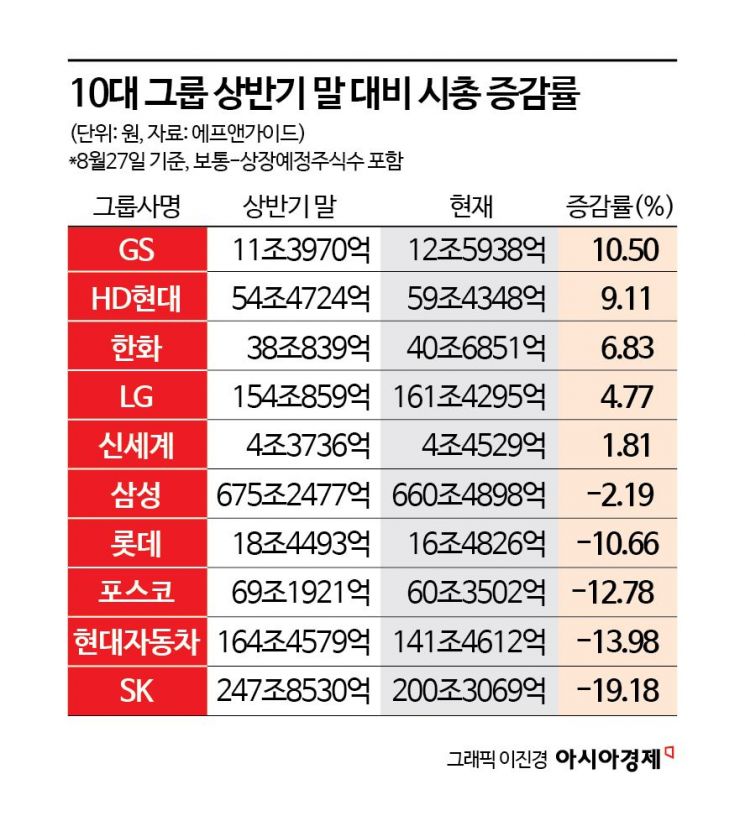

Market Cap of Top 10 Groups Down About 80 Trillion Won Compared to H1

GS Group Shows Largest Increase... Up 10.5%

SK Group Shows Largest Decrease... Down 19.18%

Recovery in Construction Stocks and Sluggish Semiconductor Divide Fortunes

As construction stocks have recently rebounded, GS Group's market capitalization among the top 10 conglomerates showed the largest increase compared to the first half of the year. On the other hand, semiconductor stocks have shown sluggish performance in the second half, leading to the largest decrease in SK Group's market capitalization, with Samsung Group's market cap also declining compared to the first half.

According to financial information provider FnGuide on the 29th, as of the 27th of this month, GS Group's market capitalization was 12.5938 trillion KRW, marking a 10.5% increase compared to the end of the first half. This was the largest growth among the top 10 conglomerates. HD Hyundai (9.11%), Hanwha (6.83%), LG (4.77%), and Shinsegae (1.81%) followed.

The increase in GS Group's market capitalization was led by GS Construction. GS Construction's market cap rose by 43.38% compared to the first half, ranking first in growth rate among the top 10 conglomerates.

GS Construction's stock price has continuously risen in the second half, climbing from the 15,000 KRW range at the end of the first half to the 20,000 KRW range. Recently, it has repeatedly hit 52-week highs, showing a strong upward trend. Since the second half, expectations of interest rate cuts and a recovery in housing prices have positively influenced construction stocks. Song Yurim, a researcher at Hanwha Investment & Securities, said, "The construction sector was one of the sectors most affected by interest rate hikes, and the recovery of the housing market is very important both fundamentally for construction companies and in terms of stock prices." She added, "Recently, there have been clear signs of recovery in sales prices and transaction volumes centered on Seoul, along with market changes such as declining market interest rates, rebounding housing sales sentiment, and the spread of warmth to regions outside Seoul, which sustain market expectations. It is time to increase interest in housing stocks overall." In particular, GS Construction is expected to see a turnaround in performance this year. Kim Giryong, a researcher at Mirae Asset Securities, said, "GS Construction's consolidated performance this year is expected to be 13 trillion KRW in sales and 388.8 billion KRW in operating profit," adding, "Operating profit will turn positive compared to the previous year, marking a performance turnaround." He further noted, "Investment points such as the rebound in housing stocks due to sector investment sentiment recovery, performance turnaround, and expectations for financial structure improvement through subsidiary sales will remain valid."

On the other hand, SK Group's market capitalization was 200.3069 trillion KRW, down 19.18% compared to the end of the first half, marking the largest decline among the top 10 conglomerates. Along with this, Hyundai Motor (-13.98%), POSCO (-12.78%), Lotte (-10.66%), and Samsung (-2.19%) also saw their market caps decrease compared to the first half.

The semiconductor sector, which led the market in the first half, slowed down in the second half, resulting in decreases in SK and Samsung's market capitalizations. SK Hynix's market cap dropped by 26% in the second half, and Samsung Electronics' decreased by 6.99%. Besides SK Hynix, SK Group's SKC (-23.90%), SK IE Technology (-22.34%), SK D&D (-19.91%), and SK Square (-19.20%) also showed double-digit declines, eroding the overall group's market capitalization.

Earlier this month, as the market experienced an unprecedented crash, the combined market capitalization of the top 10 conglomerates fell to 1,357.6869 trillion KRW, down about 80 trillion KRW from 1,437.6129 trillion KRW at the end of the first half.

There is a forecast that the semiconductor sector, which significantly influences the market capitalization of the top 10 conglomerates, may see a turnaround in sentiment after mid-September. Chaemin-sook, a researcher at Korea Investment & Securities, explained, "The recent price adjustments of the three major DRAM companies, including Samsung Electronics and SK Hynix, began due to concerns over declining DRAM average selling prices (ASP) caused by increased mobile inventory." She added, "While the performance related to artificial intelligence (AI), such as high-bandwidth memory (HBM), has already been reflected in estimates, the biggest issue is the renewed increase in general DRAM inventory, especially mobile. For a sentiment turnaround, confidence that DRAM ASP will continue to rise through the fourth quarter is necessary, and the time to confirm this will be after mid-September."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}