Undervaluation Persists Compared to Global Competitors

"Must Prove Sustainable Shareholder Returns, Not One-Time"

Market attention is focused on whether Hyundai Motor Company can continue its additional rise by strengthening its shareholder return policy. This is because the improvement in the shareholder return rate could normalize the situation where it is severely undervalued compared to global competitors.

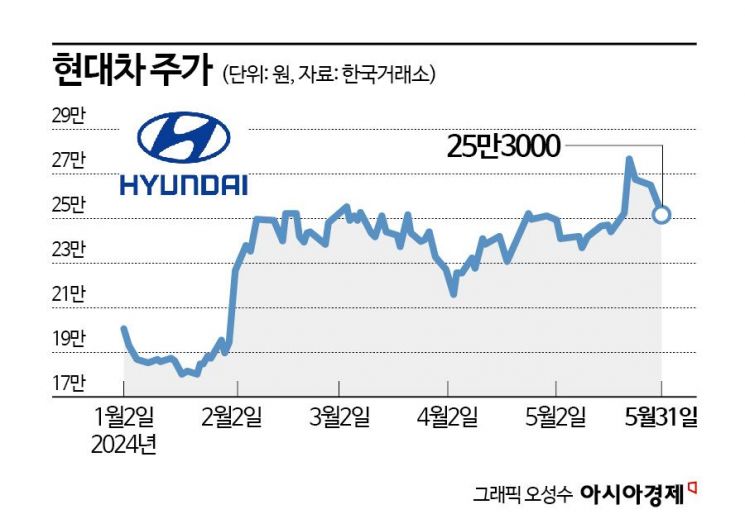

According to the Korea Exchange on the 3rd, Hyundai Motor recorded 253,000 KRW, rising 40.72% from the low point since the beginning of the year as of the end of last month. On the 22nd of last month, it reached an intraday high of 277,500 KRW, marking a 52-week high, but recently it has been declining day by day, appearing to take a breather. Since the government announced the corporate value-up program in January, Hyundai Motor has shown a steep stock price increase and has established itself as a 'value-up beneficiary stock' by supporting a solid bottom despite intermittent market fluctuations.

In the securities industry, there is a consensus that further stock price increases for Hyundai Motor are possible, and the prerequisite is to strengthen the shareholder return policy. Cho Hee-seung, a researcher at Hi Investment & Securities, said, "Recently, stock price volatility has been high due to expectations for shareholder returns," adding, "With the upcoming CEO Investor Day (CID) in August, investors' curiosity about the scale of expanded share buybacks is growing." He also explained, "Furthermore, expectations have increased that the shareholder return policy could be expanded through additional cash secured by the IPO of the Indian subsidiary."

The consensus in the securities industry is that improving the shareholder return rate is urgent to escape the current severe undervaluation. Yoon Hyuk-jin, a researcher at SK Securities, said, "Hyundai Motor recently strengthened its dividend payout ratio, raising last year's shareholder return rate to 25%, but compared to global competitors, the difference is huge," noting, "The average shareholder return rates over the past 10 years for Toyota and Honda are 49% and 41%, respectively, while the shareholder return rates last year for U.S. companies Ford and General Motors (GM), where shareholder capitalism is maximized, reached 116% and 123%, respectively." He analyzed, "Expanding share buybacks and raising the medium- to long-term shareholder return rate to 40% is the most effective way to normalize the undervaluation situation."

Furthermore, there is an evaluation that if Hyundai Motor proves that new business investments and shareholder return policies are sustainable, it could emerge as a new leading stock. Lim Eun-young, a researcher at Samsung Securities, said, "As Hyundai Motor's annual operating profit enters the 15 trillion KRW range, more than 2 trillion KRW in cash is being accumulated annually," emphasizing, "Investors should focus on the sustainability of shareholder returns rather than the one-time increase in the scale of share buybacks and cancellations." He continued, "Considering the need for investment in Hyundai Motor's new businesses such as robots and hydrogen vehicles, excessive return scale could be a burden, but if trust in the shareholder return policy builds, the valuation gap with Japanese companies like Toyota and Honda will narrow," adding, "The trigger for stock price increase is expected to be the approximately 1 trillion KRW level of share buybacks and cancellations anticipated this year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}