There is a forecast that the semiconductor market upswing will continue at least until the first half of next year. It is analyzed that the improvement in semiconductor exports will continue to play a role in driving the growth trend of our economy.

Additionally, amid intensifying competition between the U.S. and China over advanced industries, it is expected that the economies of the U.S. and China will continue to grow supported by government stimulus measures, positively affecting South Korea's exports. However, there are concerns that in the long term, the segmentation between the two countries may have a negative impact on exports.

"Semiconductor Market to Rise Until First Half of Next Year, Driving South Korea's Economic Growth"

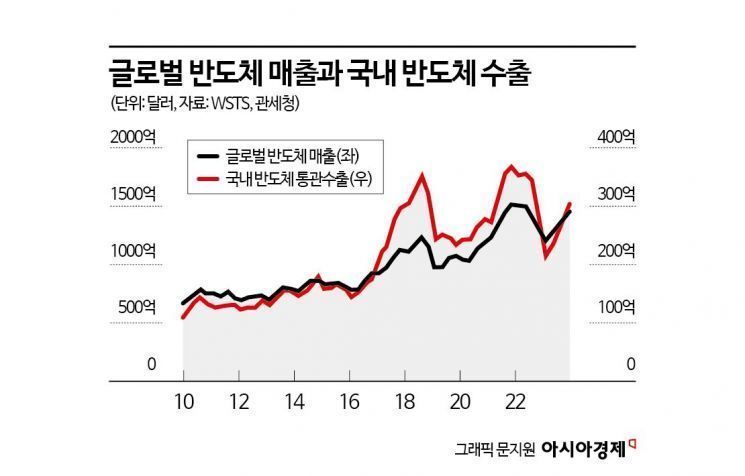

According to the ‘Recent Semiconductor Market Situation Review’ report released by the Bank of Korea on the 24th, the current global semiconductor market upswing driven by the AI boom shows a pattern similar to the semiconductor upswing that began in 2016 with the expansion of cloud servers.

Since 2010, there have been three major semiconductor market upswings: in 2013 triggered by the expansion of smartphone demand, in 2016 with the start of cloud server expansion, and in 2020 due to increased non-face-to-face activities during COVID-19.

In all three cases, semiconductor demand expanded widely, leading to significant increases in corporate investment and supply, followed by a shift to a downturn phase caused by oversupply due to weakening additional demand. Each of the three upswings lasted about two years, but the magnitude of the increase was greater when demand spread across various sectors.

Looking at the increase in semiconductor sales, 2016, which saw the spread of cloud servers and virtual assets, and 2020, when non-face-to-face activities increased demand for mobile and PC information and communication products due to COVID-19, showed larger growth than 2013, which was limited to smartphone demand expansion.

The report evaluated that the semiconductor boom triggered by AI is expected to spread not only to AI servers but also to general servers, mobile, PCs, and other sectors, making the current upswing similar to that of 2016.

Choi Young-woo, head of the Economic Trend Team at the Bank of Korea’s Research Department and author of the report, emphasized, "Semiconductor demand is highly likely to expand from AI servers to other sectors in the future, and supply expansion is also constrained. We judge that the semiconductor market will continue its upward trend until the first half of next year, with the possibility of lasting longer."

Choi added, "During the global semiconductor market upswing, domestic semiconductor exports are showing favorable performance, which is expected to drive the growth trend of our economy. Investments in facilities and construction for domestic semiconductor production, as well as data center construction investments, will also play a positive role in the domestic economy."

"G2 to Continue Domestic Demand-Led Growth... Positive for South Korea's Exports"

On the same day, the Bank of Korea also released a report titled ‘Evaluation and Implications of Recent G2 Economic Situations,’ forecasting that "the U.S. and Chinese economies will continue a domestic demand-led growth trend supported by government fiscal and industrial policies."

The U.S. and Chinese economies maintained growth in the first quarter of this year. Despite high interest rates last year, the U.S. showed strong growth, with first-quarter GDP recording an annualized rate of 1.6% compared to the previous quarter, showing a slower growth rate than the 3.4% in the fourth quarter of last year. However, favorable employment conditions, steady consumption, and a shift to increased facility investment suggest continued domestic demand-led growth. China’s economy saw a surprise 5.3% GDP growth in the first quarter, offsetting sluggish real estate and consumption by increased exports along with manufacturing and social overhead capital (SOC) investments.

Recent growth in both countries heavily relies on government fiscal stimulus measures. The U.S. has strengthened private consumption support through student loan forgiveness and expanded transfer payments to households. In China, the central government is expanding SOC investments on behalf of local governments with limited fiscal capacity. Recently, the ‘Igu Hwanxin’ policy, which provides subsidies for replacing old facilities, is promoting recovery in consumption and investment.

Investment driven by industrial policies amid U.S.-China conflicts and intensified competition in advanced industries is also propelling growth. The U.S. provides subsidies to strategic industries through the Inflation Reduction Act (IRA) and the CHIPS and Science Act (CSA). China has long provided implicit subsidies and financial support to domestic export companies.

While the U.S. is growing centered on domestic demand, China is offsetting domestic sluggishness through export expansion, further escalating tensions between the two countries. China’s large trade surpluses have caused trade frictions with the U.S., which led the Trump administration to impose tariffs and visa restrictions, intensifying trade disputes. As China increased export volumes through overproduction and low-price strategies and indirect exports, trade regulations were further tightened.

Choi Byung-jae, deputy head of the International Comprehensive Team at the Bank of Korea’s Research Department and author of the report, said, "The expansion of investment by the U.S. and China is expected to affect South Korea’s capital goods exports. The U.S. export restrictions on China will benefit exports of South Korea’s key products such as semiconductors and automobiles."

He added, "In the short term, their growth is positive for South Korea’s exports, but in the long term, segmentation between the two countries, which increases domestic production dependence in each country, will have a negative impact on South Korea’s exports."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}