Samjong KPMG Publishes Report on 'Key Issues and Future Outlook of Real Estate PF'

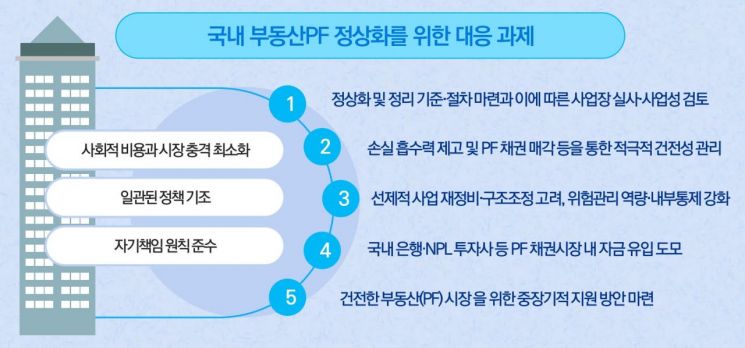

Proposes Stakeholder-Specific Checkpoints for Normalizing Domestic Real Estate PF

Calls for Savings Banks and Securities Firms to Strengthen Proactive Provisioning and Internal Controls

Following the maturity of bridge loans in the first half of this year, a large-scale maturity of main project financing (PF) is expected by next year. In this context, there is advice that financial institutions and construction companies with high risk exposure should evaluate project feasibility through due diligence and estimate the recoverability of PF under conservative assumptions, thereby establishing concrete measures.

Samjong KPMG presented the current status of real estate PF and inspection points for stakeholders in its report titled ‘Key Issues and Future Outlook Related to Real Estate PF,’ published on the 30th.

As the financial sector aggressively increased PF loans to diversify business and improve profitability, the outstanding balance of real estate PF loans, which was 92.5 trillion KRW in 2020, rose by 46.6% over three years to 135.6 trillion KRW last year. When combining the credit exposure of developers and securities firms, the real estate PF risk exposure of market participants is estimated to approach 200 trillion KRW.

The main cause of recent real estate PF problems is the contraction of the real estate market due to high interest rates and high inflation. In particular, the possibility of recovery in regional real estate markets is limited. The initial pre-sale rate in regional areas was 70% in the fourth quarter of last year, indicating continued weak demand. Developers, construction companies, secondary financial institutions, and trust companies are intricately intertwined through the real and financial markets, and risks in the domestic real estate PF market could spread like a domino effect.

Due to unsold inventory in regional areas, savings banks and securities firms face uncertainty in recovering principal on senior real estate PF loans. Construction companies are experiencing reduced project feasibility due to financing burdens along with increased raw material prices and labor costs. The occurrence of unsold units or project failures raises the possibility of contingent liabilities materializing for construction companies, securities firms, and trust companies.

The report pointed out that to improve the domestic real estate PF market, developers, contractors, and trust companies should closely understand the number of real estate PF projects, business types, financial structures, and creditor rights relationships, and conduct project feasibility reviews and valuations at the corporate and group-wide level considering internal and external environmental changes. Construction companies need to proactively consider restructuring directions linked to the disposal of PF projects and various mid- to long-term business plans to improve financial structure and secure cash flow.

The report stated, “For bridge loans that are difficult to convert to main PF, savings banks and securities firms should fully reserve 100% of expected losses as provisions and promptly sell them. For PFs with construction delays or low pre-sale rates, provisions should be increased stepwise assuming the worst-case scenario.” It added, “Financial institutions should focus on improving soundness by managing delinquency rates and non-performing loans, and promote the sale of collateral other than PF bonds, sale of business rights, and restructuring.”

Furthermore, “It is especially necessary to objectively diagnose and review project feasibility, and establish loan execution and monitoring systems based on risk management standards of the screening department and project feasibility,” and advised, “while enhancing the professional capabilities of employees for project feasibility evaluation, internal controls should also be strengthened.”

To absorb unsold inventory, effective incentives are also needed to activate private joint unsold inventory funds and CR (Corporate Restructuring) REITs. In the mid- to long-term, measures to strengthen developers’ capital, diversify risk structures with various investors beyond construction companies, and establish real estate PF monitoring systems should also be considered.

Kim Jeong-hwan, partner at Samjong KPMG’s Corporate Real Estate Advisory Division, said, “A long-term perspective is necessary to seek solutions to the current real estate PF crisis.” He added, “In particular, financial institutions and construction companies with high real estate PF risk exposure should evaluate project feasibility through due diligence and estimate PF recoverability under conservative assumptions to establish concrete measures.” He further emphasized, “Liquidity management, provision reserves, and business restructuring should be considered to continuously find business opportunities in the real estate market that experiences cycles of recession and boom.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}