KB Financial Surpasses Competitors by 270 Billion Won in Net Profit

Recognizes 274 Billion Won in Hong Kong ELS Compensation Costs

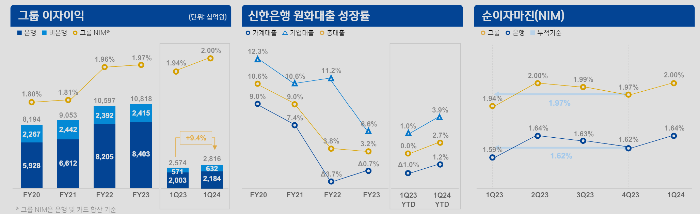

Expands Won Loans and Increases Fee Income

Quarterly Dividend of 540 Won per Share

Plans to Cancel 300 Billion Won in Treasury Stock

In the first quarter of this year, Shinhan Financial Group reclaimed its position as the 'leading bank,' surpassing KB Financial Group. This was due to relatively lower compensation for losses on Hong Kong H-Share Index (Hang Seng China Enterprises Index·HSCEI)-based equity-linked securities (ELS), improvements in net interest margin (NIM), expansion of won-denominated loans, and increased fee income, all of which positively impacted overall earnings.

Shinhan Financial announced on the 26th that its net profit for the first quarter was 1.3215 trillion won, a 4.8% decrease compared to the previous year. KB Financial, which recognized 862 billion won in compensation for losses related to Hong Kong H-Share Index (HSCEI)-based ELS, recorded 1.0491 trillion won, a 30.5% decrease from the previous year, ceding the leading bank position to Shinhan Financial.

Shinhan Financial also set aside 274 billion won in provisions related to the Hong Kong H-Share Index ELS loss incident in the first quarter but partially offset this through the expansion of won-denominated loans and increased fee income from major group companies. Interest income rose 9.4% year-on-year to 2.8159 trillion won. This was influenced by a won loan growth rate of 2.7% (1.2% for households, 3.9% for corporations) and the group's quarterly net interest margin (NIM) improving by 6 basis points (1bp=0.01%) to 2.00% compared to the same period last year.

Shinhan Financial's non-interest income increased by 0.3% to 1.0025 trillion won. Although gains related to securities decreased, fee income rose. Fee income increased by 28.4% for credit cards, 25.8% for securities custody, and 21.4% for insurance. The provision for loan losses decreased by 18.0% to 377.9 billion won. The loan loss expense ratio for the first quarter remained stable at 0.38%. Non-operating losses amounted to 277.7 billion won, influenced by Shinhan Bank's provision of 274 billion won related to the Hong Kong H-Share Index ELS.

The contribution from the global division expanded. The global division's net profit for the first quarter increased by 35.4% to 215 billion won. Shinhan Financial is expanding its overseas business, recently investing in Credila, India's leading student loan company. By subsidiary, Shinhan Bank posted a net profit of 928.6 billion won, down 0.3%. Shinhan Investment Corp. recorded 75.7 billion won, a 36.6% decrease but turned profitable compared to the previous quarter. Shinhan Card (185.1 billion won), Shinhan Life (154.2 billion won), and Shinhan Capital (64.3 billion won) also posted net profits.

A Shinhan Financial official stated, "Despite the challenging market environment, we demonstrated solid fundamentals and a diversified business portfolio, resulting in favorable performance. In particular, the increase in interest income due to asset growth centered on corporate loans at the bank and margin improvement, along with increased non-interest income based on fee income growth from credit cards, securities custody, and insurance profits at major group companies such as card, securities, and life insurance, led to an improvement in the group's operating profit."

On the same day, Shinhan Financial's board resolved a first-quarter dividend of 540 won per share and approved the acquisition and cancellation of treasury shares worth 300 billion won during the second and third quarters. The treasury share acquisition and cancellation will be conducted through a trust contract method over six months, with all acquired shares planned to be canceled after completion. Shinhan Financial's Basel III (BIS) capital adequacy ratio stood at 15.8%, and the common equity tier 1 (CET1) ratio was 13.09%, maintaining stable capital ratios through efficient risk-weighted asset (RWA) management.

Meanwhile, regarding the sale of shares by BNP Paribas and some private equity funds, which had participated in management through shareholding in Shinhan Financial, the overhang issue is expected to gradually ease. A Shinhan Financial official said, "With the significant completion of share sales by major investors such as private equity funds during the first quarter, the supply-demand instability caused by the previously concerning overhang (potential sell-off volume) is expected to improve gradually. The cooperative relationship as business partners, such as the recent joint investment between Shinhan Bank and India's Credila, will continue."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}